$Adyen: Simplifying payment

$Adyen: Simplifying payment

The most integrated payment ecosystem

Company: Adyen

Ticker: Adyen, listed in Amsterdam

Industry: Financial technology (Fintech)

Investment thesis

Adyen has been a stock market darling since the start of Covid-19 due to the exploding volume of online transactions. It has been able to grow both its top line and bottom line at an impressive rate for the past 5 years at around 40% as well as high profitability (60% EBITDA margin). As a result, it has been valued by Mr. Market highly at more than 35x P/s.

The problem with highly valued companies is that their future growth has been fully priced in and any missteps or slow down will be severely punished by the market. Adyen suffered the same fate when it missed the wall street estimates. Its stock tumbled by 50% YTD.

Source: Chamath X.com

On top of that, the issues of race to the bottom resurface again as argued by bear analysts which I have extracted as shown from the above. So, the research will be mainly focused on whether the statement is true and does Adyen possess an edge as compared to its peers.

Introduction

Payment industry is probably one of the most complex industries but there are many good resources to read up on the industry history and how payment works. Click here for further information. I will skip that part and focus mainly on the Adyen core business - acquirer.

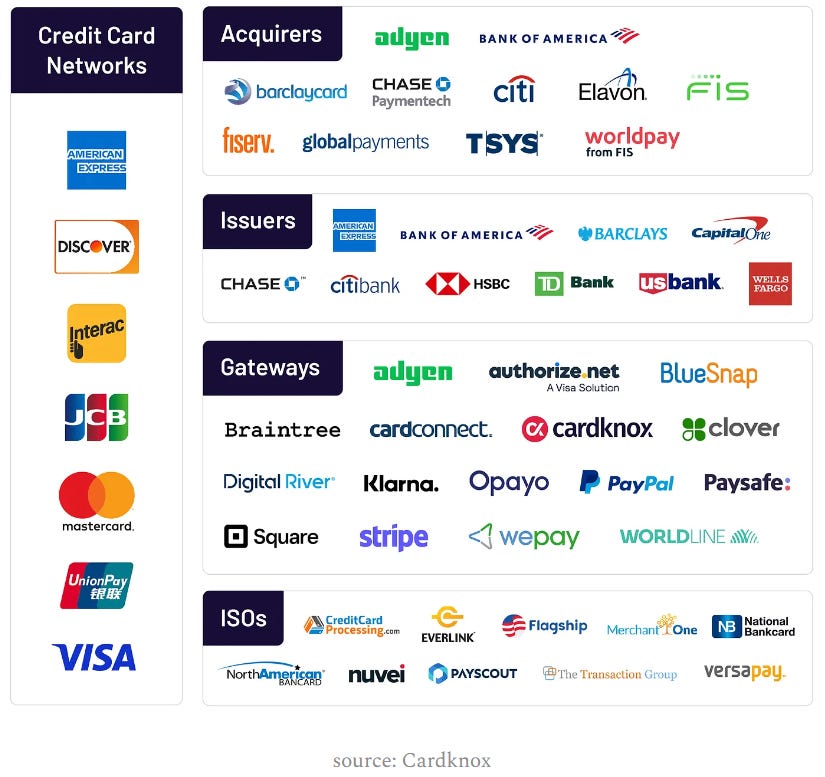

What is an acquirer? To keep it simple, It is essentially the “merchant” bank account and the main function is to enable merchants to receive/refund money both online and offline accurately from their customers all over the world.

However, there are a few moving parts for a merchant to receive/refund money. There are payment gateway(online)/payment terminal(offline), acquirer processor and acquiring bank which are usually operated by different players traditionally. Thus, a merchant will be liaising with many parties such as payment gateway with paypal, acquirer processor with Fiserv and acquiring bank with JP Morgan.

Worst if they have operations internationally and they have to liaise with multiple local players. Working with an incumbent such as Worldpay (mainly expanded through M&A) is like working with 10 different smaller companies in a trenchcoat (Quote directly from Jareau Wade). This means the service, API endpoints, and products vary dramatically by geography. It is going to be a pain in the ass for the enterprise.

This is where the disruption came in. Adyen founder, being one of the pioneers in the industry, saw the issues that a merchant was facing (especially for enterprise) and he created Adyen to solve this problem. Adyen is unique because it is an integrated platform that provides an end-to-end solution from checkout to settlement with scale.

Business model

How does an acquirer make money?

To understand that, I will use a real life example (excluding other valued added services such as fraud detection, analytics,etc). A customer pays $100 for a pair of Nike shoes using his credit card, the merchant will only receive $98.14. So, where does the $1.86 go? (assuming the lowest take rate)

1)Issuing bank (ie: DBS) will receive the most as they undertake default risk (it is called interchange fees and it can range from 1.5%-3% depending on the regulation and payment option)

2)The card networks (or schemes), e.g. Visa or Mastercard collect Scheme Fees range from 0.15%-0.2%

3)The acquirer, ie: Adyen collects Acquiring Fees range from 0.1%-1% for settlement

4)The processor, ie: Adyen collects a fixed amount of processing fees $0.11 (varies by countries and provider)

Adyen’s gross revenue is segmented in four categories: settlement fees (3), processing fees (4), sales of goods, and other services. Settlement fees ~52% of net revenue; while processing fees is ~29% net revenue. (2023: Adyen changed its revenue recognition from gross to net basis)

Adyen uses an interchange + model so that their pricing is transparent. Since the markup is inversely related to the volume, as a result, Adyen customers, usually a large enterprise, have greater negotiating power and this has resulted in Adyen usually price at the lower end of the spread spectrum.

As for its sales of goods (4% of net revenue), it is their POS terminal which they usually sell at cost so that they can earn from the transaction fees. (classic razor and blade model). Lastly, for “other services” (15% of net revenue), Adyen earns from forex fees, third party commission, issuing services, risk, and fraud analytics etc. These value-added services to merchants allow Adyen to expand its take rates.

Addressable market and Competitive landscape

These 2 topics are closely related and if the market is huge and growing, in theory, everyone gets a share of the pie and the intensity of the competition will be lower than most investors expected.

Let's look at the TAM first. As per research and markets, the global merchant acquiring market stood at $27.80 trillion in 2021 and is estimated to reach $41.75 trillion by 2026. Assuming an average take rate of 0.25%, there will be an opportunity of $100bil of revenue up for grab. The segment is also expected to grow healthily at a CAGR of 8% (2022-2026) due to tailwinds such as rapid digitisation, growth in e-commerce, omnichannel expansion, etc.

Adyen, being one of the disruptors, is taking share quickly from incumbents but it is still small relative to the global TPV. Based on current total payment volume (about $800bil), Adyen market share is around 2.5% (based on 2026 estimated TAM).

If Adyen was to grow 20% for the next 10 years, its market share would remain in the low double digit (around 10% assuming no future growth in estimated TAM). It does suggest that the market is huge enough to accommodate a few players.

Competitive landscape

Broadly speaking, there are 2 types of competitors: incumbents and disruptors. The discussion will be mainly looking at the US market as it is the largest market (excluding china as there are local champions like Alipay which is difficult to penetrate) by payment volume (around half of global TPV)

Legacy players- Based on the Nilson report, the top 3 incumbents are Chase Paymentech (owned by JPMorgan), Worldpay (owned by FIS), and First Data (owned by Fiserv). Each of these players processed more than a trillion dollars of payment volume in 2022 and collectively did ~$4 Tn. It is estimated that top 10 players manage 60% of the TPV in the US and the legacy players remain dominant (94%) vs the modern acquirers (6%).

Are they losing market share? The short answer is yes but it is at a much slower pace than expected (about 1% per year). As explained earlier, incumbents are burdened with an increasingly complex payment ecosystem and technical debt (multiple platforms and integration).

Besides, disruptors are lowering the switching cost by introducing an API that can be easily integrated with the merchants. Lastly, incumbents are suffering from an innovation dilemma and counterpositioning as it is still a lucrative market for them. “You do not want to kill your golden goose.” As a result, the pace of innovation is slowed and it gives the disruptors an opportunity to enter the market.

However, why are the customers switching slower than expected? It could be based on a few factors. Firstly, banks who are both issuers and acquirers tend to have higher authorisation rates for their own cards. Top 5 issuers are still the banks with 60% market share. Secondly, these banks usually could bundle other services to increase their stickiness, which explained slow transition.

Lastly, smaller merchants (especially existing businesses) have lower bargaining power and are likely to stay put as it might not worth the trouble to disrupt their daily operations. (This will not apply to new startups/SMB as they have more options)

Or larger legacy merchants like Kroger that have multiple physical POS embedded in each store will make it harder to switch. Unless these new acquirers have proven their ability to process large volumes (ie: Kroger revenue is around $110bil), the switch might take longer to happen.

Banks seem like a tougher candidate to go after but pure payment processors (FIS & Fiserv) are at much greater risk. It is likely to be the share donor going forward because of the issues mentioned above. (Note: these players are consolidating to boost their market share but it is not going to be sustainable in my view) Click here to read more about their M&A activities.

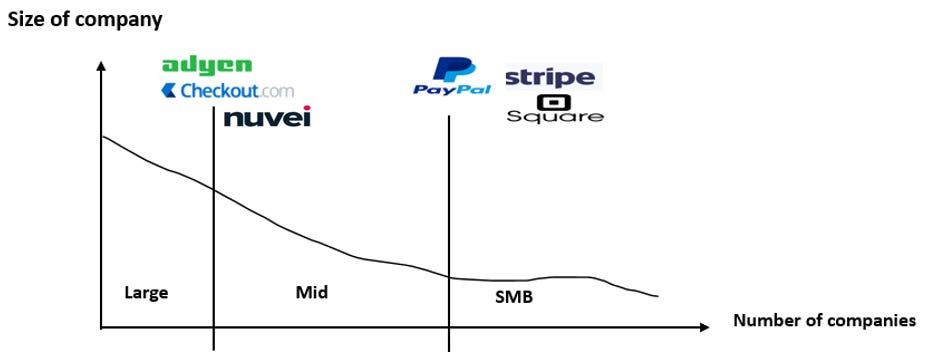

The disruptors- Incumbents are still their largest competitors for short to midterm but the disruptors will be a greater threat to Adyen in the long term as they do not face the similar issues as the incumbents.

The above diagram clearly shows the disruptor’s strength in respective markets but they are likely to move up or down the segment to increase their market share. There are some early signs that Adyen is moving down the market such as introducing Adyen for the marketplace, Adyen for Platforms, Adyen Checkout,etc to capture the right end of the spectrum. Same things apply to stripe and Paypal where they are looking to share a slice of pie towards the left end of the spectrum.

Payment facilitator

Let's discuss Stripe first as it is probably one of the most successful fintech companies in the space. To make it clear, Stripe is not a merchant acquirer but a payment facilitator or Payfac. So, what is a payment facilitator? The author of anatomy of swipe explained it best:

“Payfac is a layer on top of a Merchant Acquirer. Payments Facilitators can typically onboard Merchants very quickly and offer out-of-the-box hardware and software to enable a Merchant to start accepting card-based payments quickly.”

Stripe set themselves apart by taking a developer approach, making integration for online payment with single/no code (extremely quick), etc. It is essentially lowering the barrier to accept payment which traditionally needed a track record to open an account with legacy players. (ie:minimal payment vol)

Coupled with products like analytics, reporting, inventory management, billing etc, it is extracting a lot of complexity for a small merchant. Thus, Stripe is able to charge a more premium price (typical charge is around 2.6% + 10cents as the risk lies with Stripe. ie: chargebacks, fraud, KYC, or AML).

Nevertheless, it sounds great when their customer business is small but when they grow bigger, there is undoubtedly more bargaining power accrue to their customers. (Consequently, their take rate will shrink). A good example is probably Shopify, where Stripe is their main payment facilitator and the margin is likely to be very thin due to the huge payment volume (contributing an estimated 13% of 2022 Stripe TPV).

The dilemma is that Stripe would hope that the market is much more fragmented (more bargaining power against smaller merchants) as these e-commerce aggregators are eating into their margin. They are probably stuck in between scale (going after enterprise but lower margin) or margin (going after smaller merchants but smaller market). As a result, their cost structure blows up as they are trying to satisfy both sides of the markets. (lack of focus)

Nuvei and checkout are direct competitors to Adyen. Both of these companies claim to offer a similar value proposition to Adyen and higher authorisation rate. However they are much smaller (ie: Nuvei TPV is around $128bil), more aggressive in pricing and have less stellar clients profiles.

A quick overview suggests that both checkout (remain private) and Nuvei (listed in Canada) target more markets. (ie: Cryptocurrency, B2B payment, Saas,etc). They are also more acquisitive as compared to Adyen. Besides, they have more exposure in the middle east countries due to their connections. (ie: Checkout founders are located in Dubai). Lastly, their businesses are also less/not profitable and deploy higher leverage.

Bull vs bear

The race to the bottom

This is a difficult question to answer but I am leaning toward the argument that it is not a race to the bottom. Simon Taylor, a famous blogger on the fintech industry made a good argument on the point. To quote him:

“The value add isn't simply "the ability to get paid for the lowest cost." Depending on the buyer, it might be improving authorisation rate, conversion at checkout, helping reactivate customers after a purchase, expanding into new markets, managing fraud rates,etc. Payments are easy. Edge cases are hard.”

Adyen edge

That is exactly what Adyen is trying to achieve. Adyen has an edge to improve authorization rate especially for accepting global payment. This is because Adyen was originally created to solve the complexity of the payment ecosystem in Europe which includes lots of currencies, multiple licensing and regulatory compliance and many local payment methods. (their stronghold)

As a result, with an integrated platform (from gateway to settlement), it gives Adyen a better insight on why certain transactions are being rejected, reducing fraud through tokenisation and thereby increasing their authorisation rate. This itself created more value than their slightly premium pricing as compared to their competitors. (Note: There is no disclosure on its authorisation rate but it is estimated to be around 90%)

MBI, a blogger has illustrated this point beautifully by calculating the amount gain vs the take rate. For every dollar paid to Adyen (assuming 98% authorisation rate) , it will easily create $10 more revenue than a competitor with lower take rate but also lower authorisation rate (assuming 95%).

Besides, it makes no sense for enterprises to set up their own local payment processor in every country that they are operating as the back office costs are going to be more expensive. It is similar to the AWS value proposition where Amazon built out the expensive infrastructure and shared the cost with more users so that it will be cheaper to rent than to build their own.

As a result, Adyen possesses a geographical edge and they are actively securing local acquiring licenses to widen their moat. (Currently, they can accept up to 9 types of different payment methods from BNPL to digital wallet to mobile covering 100 countries) With one contract, their customers will be able to enjoy higher authorization, lower processing costs, faster merchant payouts, lower interchange costs and card network fees globally. (Note: Adyen had full acquiring licences for Europe, Australia, New Zealand, Singapore,Hong Kong, US,etc)

Bear argument

The US is generally a tough market especially for the large enterprise e-commerce/online only players such as Amazon, Shopify, Uber, etc. Bear argues that the US itself has a high authorisation rate to begin with due to one country, one currency, and there are no local payment methods.

Besides, the rise of the payment orchestrator platform (POP) will further remove the barrier to switch. Basically, a POP is a platform that integrates different payment providers and methods into a single infrastructure. It is programmed to route transactions based on cost, performance, etc.

As a result, volume can be easily shifted away (but restricted to online transactions) especially for large enterprises as they have their own team or prefer a specialized company to provide value added service like fraud, data analytics, reporting,etc. There is limited differentiation.(commoditised) From an interview by Ben Thompson with Lisa Ellis:

“You might have 80% (volumes) here, 20% there, or you might in the US even have three (providers). And you’re sort of turning, adjusting across those. So it can happen quickly, which is what Adyen has experienced, and it took them by surprise because it’s not like they lost the customer. It’s not like the customer renegotiated their contract. It wasn’t even necessarily visible to them until they started to see the impacts of it.”

In addition, local players are also turning up the heat. Take Braintree, a subsidiary of Paypal as an example, Braintree is becoming more aggressive in pricing (offered at cost to bundle its Paypal button) for unbranded processing as they are losing more market share for their branded checkout due to the rise of players like Apple pay, Google pay,etc.

As a consequence of the above, Adyen, who is unwilling to match the price dropped, has suffered from the decrease in sales. Ie: Adyen growth has slowed down considerably (from 40% to 20%) in the US recently (FY2023) and this has negatively affected Adyen's future growth and margin profile. (Bear predicts that Adyen margin is peak at 2022 at least for the US market)

However, In my view, it is not a doomsday scenario for Adyen. It is true that Adyen relies on large online enterprise customers but it is reducing its exposure on them. (from 31% to 18% in 2022 for its top 10 customers)

For context, large enterprise online players only account for 10% of the total payment volume in the US. Adyen has 20% of the 10% which implies only 2% market share. It is true that these players will grow but the rest of the market is so much larger (90%). Adyen is highly aware of these and they are deploying more resources to target traditional retailers (Mcdonald’s, Louis Vutton) who are not tech native by introducing “unified commerce”.

Omnichannel is extremely valuable and differentiated because it is solving a different problem altogether. It is trying to create an unified experience where there is no difference between shopping online and offline. Customers could easily buy online, return offline and get their refund instantly.

“If you had basically discussed this like 3, 4 years ago that a fast food chain would work with a processor like ourselves to accept payments, I would have said that likelihood is relatively low because they just need pipes at a counter to process quickly.

But now it's completely shifted because it is about consumer insight. It is about making sure that no matter if you pay in the app or at a counter that you have to write the information. So it opens up a lot of new verticals, and that's what we're focusing on right now. The unified commerce opportunity is huge. We're ahead of competition, like there's no global player that can offer this in a single platform.” CEO, Pieter van der Does.

Besides, omnichannel has a higher barrier to entry and switching cost because the provider needs to co-locate its data center near every city to reduce latency (costly), replacing all the physical hardware (time consuming), etc. It is a tougher market but a better one for Adyen in the long run. I have to agree with the statement by Ben Thompson in the Lisa Ellis interview “I just think in general, online-only companies have a very hard time with the real world and the real world is always the ultimate moat.”

Sources: TQI calculation

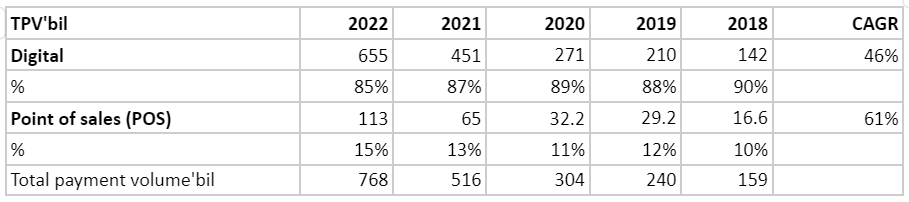

Although the physical volume remains small, there is a clear trend that shows Adyen is actively growing its POS volume.

Economy of scale

Payment industry is attractive because of high operating leverage. It is because the industry has high fixed costs (75% of the cost structure) but low variable costs. Incremental margin will be high. For Adyen context, Adyen posted ~54% EBITDA margin and ~30% incremental EBITDA margin in 2022.

With Adyen currently leading the enterprise market (scale), they could play to their strength by lowering their take rate to the lowest without hurting much of its margin as it has a low cost structure. However, Adyen has been reluctant to do so as price wars usually end up dragging the whole industry profitability. Incumbents should be the key market for them to grab share.

Management

Adyen is a founder-led company with the CEO, Pieter owning close to 3% of the company. (estimated to be around $1bil). I would only focus on a few key points which I think deserve more attention. Click here for more discussion.

Organic growth: Adyen founder is obsessed with organic growth and shun acquisition (0 acquisition to date) because he saw first hand on how the integration issues/patchwork continue to plague the incumbents.

“At Adyen we have a great preference for simplicity. Because if it’s simple, it’s easier for us to control it. So therefore we never made an acquisition. We only run one system. We only have engineers that are educated in the languages we use within the company.” CEO, Pieter van der Does.

Total control: The Adyen team has a strange obsession with control. I believe that they understand payment is a trust business. Thus, total control will give them an important differentiation vs their peers in the long term. Adyen built all their payment infrastructure in-house. It could be more capital intensive but in the long run, it creates more value (better security, uptime, processing speed).

For example, Adyen hosts its main systems in separate data centers in Europe, in the US and Australia. They do not outsource any administration to third parties, nor use any public cloud services for payment processing.

Cost conscious: Adyen cost structure is very lean and highly productive. (helps with low SBC-0.6% of revenue). For comparison, Stripe might be processing 10% more of TPV but have 2.5x more workforce than Adyen.

Sources: TQI calculation

This might be related to Adyen culture. Adyen CEOs have been vocal in their hiring process. This is because not only is staff the largest portion of their cost structure (25% of net revenue), it is also going to affect the company culture.

Pieter mentioned in a podcast: “The board still oversees every hire, regardless of the role. You cannot be hired at Adyen without speaking to one of the six board members. The reason we do it is to set the bar high to ensure that only the best talent joins Adyen.” (recently Adyen spoke about extending this group to 12 people to help them scale).

Adyen does benefit from Netherlands (60% of workforce) regulation, i.e. staff bonus cannot exceed 20% fixed compensation. I believe it is not sustainable as they will have to grow in the US market which has a higher compensation package (ie: 50% higher) but the impact will not be disastrous.

Conclusion

The payment industry is definitely complex but there are a few observations that I want to highlight for this research:

1) The merchant acquiring market is an exceptionally large market (estimated at $100bil revenue) and expected to grow at 8% due to the tailwinds like digitisation, growth in e-commerce, omnichannel expansion, etc.

2) The competition is intense due to a low barrier of entries especially for the US market. Payment orchestrators allowed large enterprises to only focus on cost and performance without being loyal to any company. (volume shifting) Legacies players (ie: pure processors) will likely be the market share donors although they are trying to reverse the trend by making big acquisitions- >10billions. (Most likely not going to be sustainable) Banks are harder to disrupt due to bundling of services.

3) Disruptors are focusing on their own territory but are increasingly expanding their reach into other end markets.

4) Lastly, my belief is that payment solutions are not a race to the bottom as payment is getting more complex especially for international payment. Besides, the rapid adoption of omnichannels by merchants are also giving these solution providers more opportunity to add value. “Payments are easy. Edge cases are hard.”

To conclude, I do believe that Adyen possesses competitive advantages over its competitors. It has the geographical edge, technology edge (full stack) as well as scale to compete. It has a low cost structure with highly productive staff (high profitability) and a solid balance sheet (net cash-EUR6bil). Lastly, it is founder led (substantial stake -$1bil), highly capable management team (good capital allocator), and solid culture (prudent and long term thinking)

The next important assessment will be on the company’s valuation. Even after the huge drawdown, the company is still trading at a premium (ie: 40x P/E). It is not a screaming bargain but deserves consideration. Based on my above assumption, if they can grow as per expected, the company is trading at a reasonable valuation and I am willing to pay a slightly premium price to own it. Therefore, it is a buy for me. (Add on further weakness)

Note: Although it is a high quality company, the industry is inherently complex and changing fast. Besides, the barriers of entry are lower than my expectation. Lastly, I have to take into account the “unknown unknown” factors (ie: AI, cryptocurrency) and discount due to my lack of knowledge in the payment industry. Thus, I will not allocate a huge position (ie: max 5% of my portfolio) as I am betting more on the management rather than the company.

Update: Ingo Uytdehaage will become the company’s co-CEO alongside Pieter van der Does (due to Pieter health reasons).

Disclaimer: I have position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion.

Resources

The history of merchant acquiring |Rise of the full stack acquirer by Monetary Musings

Worldpay’s M&A Strategy and The Future of PayPal is Braintree by Jareau

Problems for Adyen and Paypal in the competitive payments landscape by Tech Investment

Fintech 🧠 Food - Is payments a race to the bottom? by Simon Taylor

An Interview with Lisa Ellis about Payments by Ben Thompson

Adyen: The “Navy SEAL” Team of Payments by MBI

Appendix

Payment ecosystem

Complexity of Europe payment ecosystem