An honest self review-Outsource thinking

An honest self review-Outsource thinking

Learning from mistakes

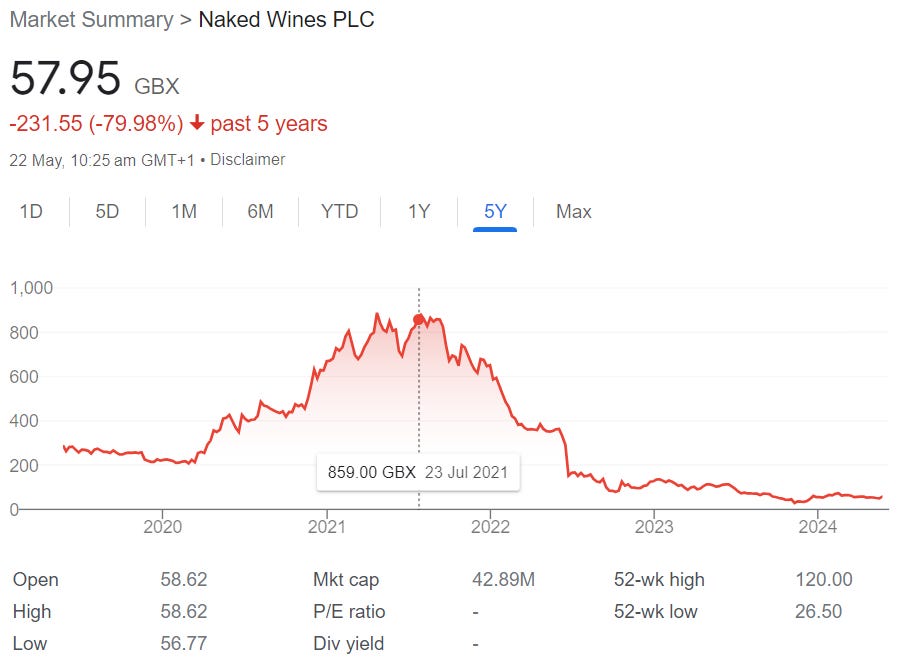

Today post is slightly different than my usual post. It is a post mortem on a mistake that I made throughout my investment journey. It is my worst performing stock and the stock dropped by 93% from its peak. (I took at 80% permanent loss from it but luckily it was a small position) It is called Naked Wine. I am pretty sure I will have a lot more mistakes in the future but I think that it is best for me to review it so that I won’t repeat the same mistakes.

I found that a lot of investors only discuss their biggest winner but not biggest loser. To me, both are equally important and I am here to make a dissection on why would I made this mistake and how to correct from it. It is my personal experience and the mistake I made is called outsource thinking.

I think it is common to fall under trap of Halo effect where when someone better or smarter is investing in a stock, it must be wise choice. Imagine that some of the smartest thinkers like Elliot Turner and Nobert Lou (i respect both of them and often read their writings) invested in this stock, it feels like I am shielded from mistakes.

I am outsourcing my thinking to them and failed to realize that it might not fall within my circle of competence. That is why I put a lot of emphasis on circle of competence and only invest in company that I can understand as well as only invest in really high quality business. You can read my previous post on My personal archive - The road to become a successful quality investor.

The thesis

If you are my regular reader, you would know that I am a big fan of Nick sleep. I am fascinated by the idea of share scale of economy. It means sharing the saving that gain from scale and thereby create a strong flywheel effect that is hard to compete. I am obsess with this business model and hope to invest in company that practice this religiously.

Then, I came across this company called Naked Wine and it was pitched by Elliot Turner. He did a great job on explaining the company and I hope that I can be half as good as him. Click here to read his fantastic work.

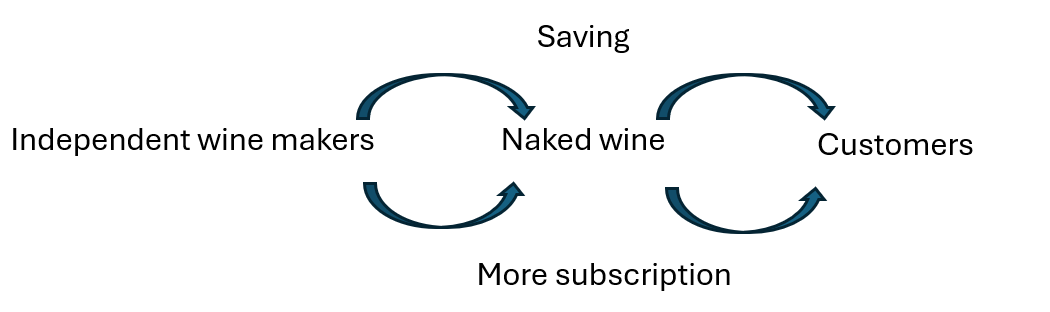

The company seems to fit the idea of share scale of economy. It is a wine subscription business that aim to eliminate middleman (wholesaler and distributor) by connecting the winemaker directly to buyer. Then, the company would markup 40% and any excess of saving will be passed directly to their customers.

The story sounds compelling from a few perspective:

Sources: TQI capital

The independent wine makers will have access to a scale platform due to Naked wine commitment and therefore can focus on making good wines without distraction. The excess saving from bypassing the wholesalers/retailers can be passed to customers. Cheaper but better wine should in theory attract more customers and lead to more wine makers joining its ecosystem. This will create the so called network effect from the process.

In addition, the platform has attracted millions in reviews which in theory will give them a better recommendation system to target their customers and create another flywheel effect. Everything sound so appealing if the business can scale. That is a big “If” and the business overestimate their ability to sell due to Covid and eventually stuck with large amount of inventory and face liquidity issues.

The mistakes:

I am not a wine drinker and failed to recognise that it is not within my circle of competence. Will the customers continue to order through online or it is just a covid effect? I believe wine drinker should understand this better.

Does share scale of economy works in every business model? My view is that if the customers couldn’t recognise the savings that passed to them, it would be disastrous to the company. There is no comparison to be made like Costco. You can easily compare Costco price to other retailers to know if it is a bargain, but would you be able to tell if some random wine is really cheaper and better quality?

I failed to recognise the base rate effect where most business will fail. Most poor business can’t last more than a decade and I should pay more attention on track record.

Most importantly, I “outsource” my thinking and failed to exercise my own judgement. The reason that we shouldn’t follow others ideas is because we might not have the conviction like them. It can be that I am early but not wrong. However, if I have no conviction to hold through the drawdown, I would have sold it before it became a multi-bagger. Thus, you can’t skip the basic work (read annual report, think like a businessman, run through checklist, etc) that will make you a great investors.

Conclusion

Hopefully my readers can learn something through this post and keep in mind that investing is simple but not easy. Please do your own due diligence and don’t let others to persuade you otherwise. I believe that most people shouldn’t invest on their own and it would better off to invest in index fund as mentioned by Warren Buffett. Unless you are truly passionate about investing and willing to go extra mile for it, it is just a tough game to beat it consistently.

Lastly, I am going to Hongkong next week to attend AGMs and meets some private investors. Thus, I will be away for a week and come back the following week. Hopefully, I can share some take aways on my Hongkong trip in my next post. If any of my readers are interested to meet me up in Hongkong (2/06/2024 - 07/06/2024), I am more than happy to meet for a coffee. Cheers!!! Just shoot me an email or direct message me.

Disclosure: Please do your own due diligence. This post is merely for education purpose and my curiosity to the world. Cheers!!!

Good write-up TQI, thank you for sharing your honest post mortem.

Thanks. It is not easy to open up but I am hoping my readers will be more cautious and exercise their own diligence when reading up my write up. I hope more of us could share mistakes so that we could learn and grow together. Cheers.