$BAM: Moving Towards The Trillion Dollar Funds

$BAM: Moving Towards The Trillion Dollar Funds

Brookfield Asset Management: The "Canada" Buffett

Company: Brookfield asset management

Ticker: BAM/BAM.TO, listed in US/Canada

Industry: Asset management

Finally i have found a company that is reasonably price and high quality. I have made a move by slowly accumulating the shares. If you want to learn more about the company, read further. I promise Brookfield Asset Management will worth your time looking at it. The CEO, Bruce Flatt is probably one of the smartest and humble guy on earth. He is known as the Canada Buffett due to his track record but it doesn’t seems that he is getting enough attention.

Investment thesis

Brookfield is by far one of the most complex companies that I have ever analysed before. The reason being that it is made up of a lot of moving parts and it is fairly difficult to determine the intrinsic value of the company. However, the management's recent spin-off of its asset management arm caught my attention as its business model is easy to understand.

It is an asset light with recurring revenue and high margin business. Eagle capital point did a fairly good job in covering the spin-off story. Click here for more. Here is another great research on brookfield as well. Thus, this report will be focusing on the spin-off asset - Brookfield asset management ($BAM).

Here is a quick argument by bull on why they will outperform:

1. Brookfield has the scale to access large and complex projects such as infrastructure, nuclear power, ports, semiconductor,etc globally. It is easier to fund millions of dollars but not billion dollar projects quickly to take advantage of the irrational selling price. (High barrier to entry)

2. Brookfield took pride in their expertise for funding capital intensive and complex projects. A good example is that they could invest in depressed assets such as Westinghouse, the formerly bankrupt nuclear reactor maker. or intel for their foundries for an attractive price and generate high IRR.

3. It has the brand to raise funds quickly. Brookfield has a long term track record as compared to other newer managers and it is easier to convince new investors to invest with them (incumbency advantage, you don't get fired for choosing IBM)

4. It has annuity-like cash flow streams as the majority (83%) of their fee-bearing capital is long duration (10-12 year average fund life due to locked up). Thus it is not affected by volatility in the market and avoids unnecessary interruption for compounding unlike T.Rowe price and Diamond Hill.

It does look attractive given the above arguments by the bulls. However, there is a need to further research before a decision is made. The key focus for this write up will be on the company's competitive advantage, management, future growth, competitive landscape, risk,etc.

Organisation structure and split

There are a few things to take into consideration before a further dive. First of all, there is a need to understand the post spin off structure. Brookfield corporation (Ticker:BN), the holding company, owned 75% of the company while Brookfield asset management (Ticker: BAM), known as “the managers”, were entitled to 25% of the company. Both companies have the equal right to appoint the board members.

Firstly, BAM will receive 100% of the management fees and 2/3 of future carried interest. BN will retain 100% of the legacy carried interest and 1/3 of the future carried interest. Secondly, it has zero debt with $3 bil of cash and financial assets. Lastly, the management is targeting a payout ratio of 90%.

The reason for the spin-off is to unlock the value for their shareholders as they believe that the asset management division deserves higher valuation since it possesses the similar scale and competitive advantages as compared to KKR or blackstone.

The potential upside to invest in BAM could be either profit from capital gain (multiple expansion) or collect an increasing dividend yield. (expected quarterly dividend is $0.32/4.2%). Management is expecting that the distributable earning will grow by 15% annually for the next five years. At this price, if based on its projection, it could have a cost yield of 8%.

Introduction

Brookfield Asset Management is one of the largest alternative asset management (AUM of $800bil and fee-bearing capital close to $418bil) companies in the world. It invests in real estate, infrastructure, credit, private equity, renewable energy, and insurance. It is a relatively low profile company as compared to KKR or blackstone.

Alternative assets

Before I proceed further, I would like to give an overview on how the alternative investment companies work and this should help to simplify the complex world of private equity and alternative asset managers. (Alex from seeking Alpha did a great job in explaining alternative asset manager)

In general, most people are familiar with traditional asset managers such as Vanguard that manage stock, bond and market market funds, exchange-traded funds ("ETFs") charging small fees for this (0.05%-1%). Alternative (or alt) asset managers are different. The word "alternative" means that the assets they manage are different from public stocks, bonds, and cash instruments.

The best known alternative asset is private equity where these companies acquire public companies by making it private and restructure it to sell for a profit. However, Alt manager has increased their scope dramatically and private equity is just a segment. Other familiar examples are real estate, private credit, venture capital, hedge fund, etc.

Since alternative assets by definition are not being traded on public markets they are relatively illiquid. It may take years to improve a piece of real estate or to turn around a company and sell them. The illiquid nature of alternative assets requires patient capital.

Thus, only institutions with long-term investment horizons can supply it such as Pension plans, endowment funds, and sovereign wealth funds. However, things might change going forward as they are tapping into the retail and insurance market which I will further explain under the tailwind section.

Fee

All fees belong to two broad categories: management fees assessed on Asset under management (AUM) similar to mutual funds and performance fees dependent on beating specific performance targets within funds (much smaller advice and transaction fees are grouped with management fees).

Alt managers charge rather high management fees that typically start with 1% of AUM. Since they are charged quarterly and the private funds are illiquid and "sticky," with a long duration (or even permanent in certain cases), management fees are continuous, recurring, and predictable.

Business model

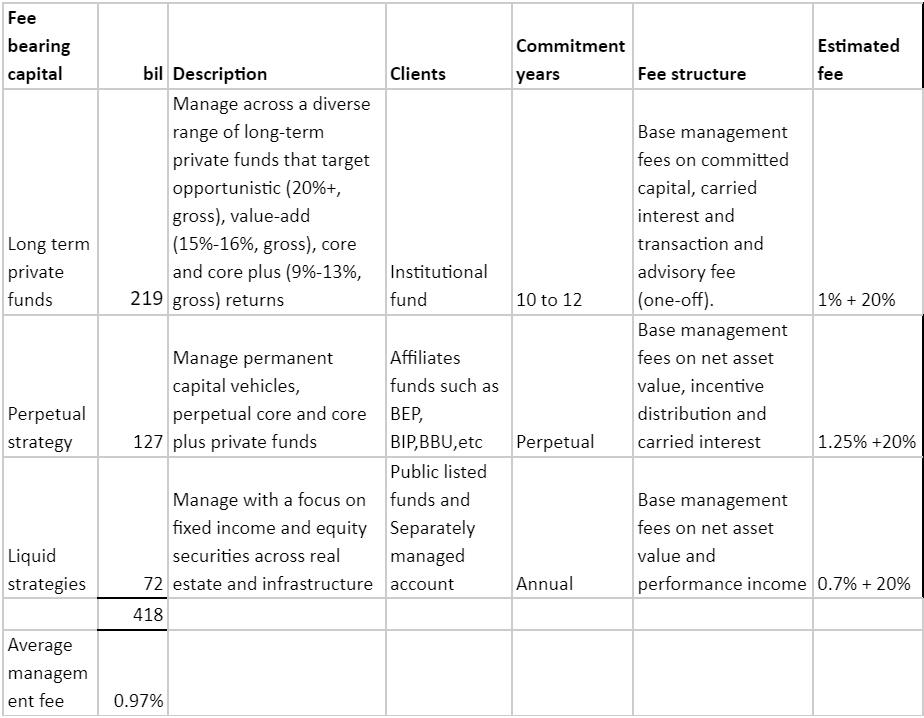

How does BAM make money? As explained above, they make money from collecting management fees + performance fees if they outperform. It has three key product categories: (i) long-term private funds, (ii) permanent capital vehicles and perpetual strategies and (iii) liquid strategies.

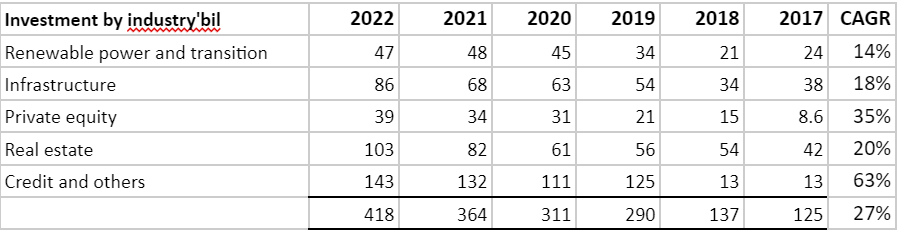

These are invested across five principal strategies: (i) Renewable Power and Transition, (ii) Infrastructure, (iii) Private Equity, (iv) Real Estate, and (v) Credit and other. Below table is a summary of the fund fee structure.

Source: Company Fillings, TQI Capital

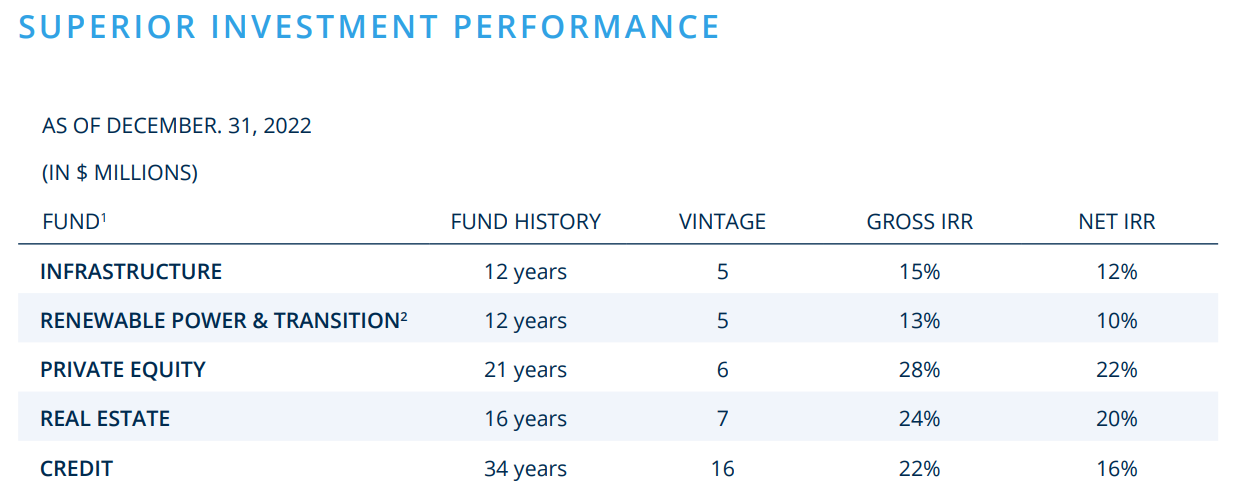

Although they do disclose fairly well, there is no disclosure by cohort for their maturity on long term private funds. This is because if most of their customers choose not to renew after expiry, it will significantly affect their fee bearing capital and management fees. Of course, the reason for not continuing with them might be due to factors like poor returns or better opportunities elsewhere. Let look at their fund performance:

Based on their previous performance, their net IRR for each fund seems to be decent ranging from 10% to 20%. As long as they could continue to outperform the market and their peers, the funds will most likely stick with them. However, their performance might be affected if interest rate continued to rise rapidly and it will be discussed under the risk section.

The next logical step would be to look at the cost structure of the company. For any asset management company, human resources typically make up a big portion of the cost. So, an important question to discuss will be: does the management try to reward themselves or shareholders?

A quick look at the income statement will tell us that the company is earning an exceptionally high fee related earnings (FRE) of around 50%-60%. It does imply that most value accrues to BAM shareholders. Other resources also confirm the fact. For example, based on an interview on a business podcast - Business breakdown:

“Investment professionals typically have a 30% interest in the carried interest of a flagship private fund. And the Brookfield parent keeps 70% of the realized carried interest.”

Bull vs Bear

Co-investment

Generally, alternative fund managers try to be as asset-light as possible. However, Brookfield strategy is slightly different from the other competitors where Brookfield will co-invest alongside with their private funds usually at around 15-25%.

Alignment of interests is an effective tool to attract third parties. They are “eating their own cooking” and if the investment turns out to be great, they will be benefiting from it as well. The downside being that it is more capital intensive and thus lower return on investment.

Surprisingly, this co-investment method seems to matter little when compared with Blackstone (the biggest company in the industry). They are asset-light, contributing only about 0.5% to assets under management ("AUM"). Blackstone has established a remarkable track record, particularly in real estate, and this track record - a unique intangible asset - appears more important than a significant alignment of interests.

Free riding structure

Thus, with this spin-off, BAM will enjoy the inherent advantage of free riding their holding company (BN) effort. For example, BN will continue to co-invest alongside with their clients but not at the expense of BAM. BAM will be able to enjoy the labor of their asset heavy holding company (BN) to perform all the heavy lifting such as recruiting, funding the projects, doing market research and marketing,etc.

Alexander Steinberg, an analyst has a good example on how BAM is benefiting from the spin off:

BN has just announced a $1.1B acquisition of Argo Group (ARGO), a specialty P&C insurer. Being an insurer, ARGO has investments (about $5B) and at least a part of these investments will end up under BAM's management generating fee-related earnings. To achieve this growth, BAM will not spend a penny. Sales and marketing are not required either. Growth will be achieved without any effort due to BN's support!

Besides, when the investment does well, BAM will be able to collect higher management fees due to increase in funds value. Thus, this has created unique circumstances where BAM can achieve high growth with minimal reinvestment. This is why they are able to distribute most of their earnings and grow at double digit. This is a truly astonishing structure that most of the other competitors lack as compared to Brookfield.

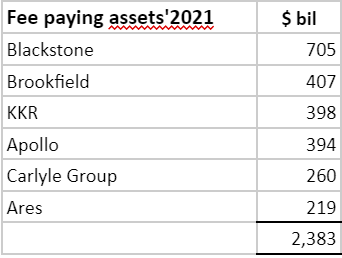

Competitive landscape

Source: Company Fillings, TQI Capital

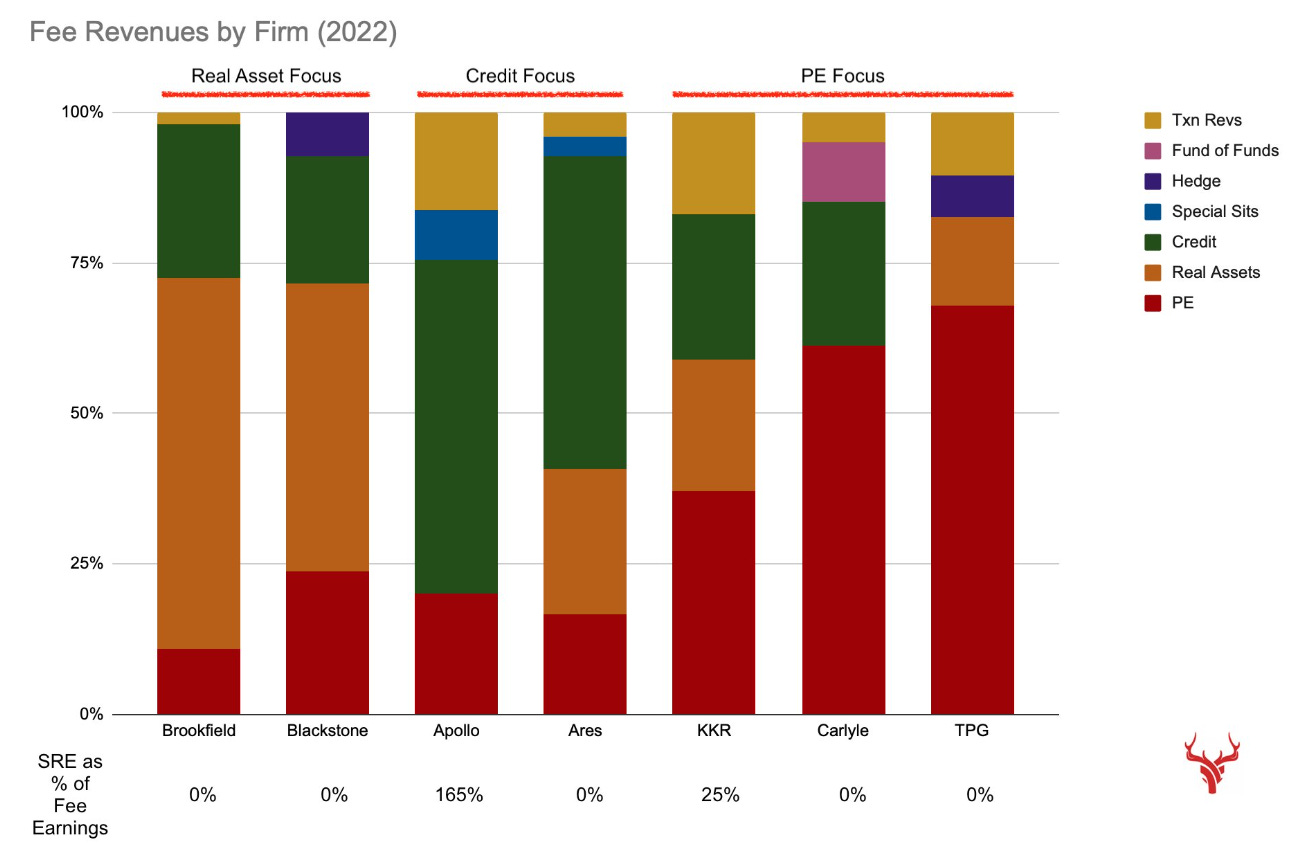

Basically, the top 6 companies above serve as the benchmark for the industries with Blackstone leading the pack. However, there are different focus of strategies by each company as shown below:

Sources: The red dear

Essentially, each company has their own strengths and target customers. For example, Brookfield and Ares have more stable fees as their structure is all about consistent management fees. As for Blackstone or KKR, their fees are more lumpy as they rely more on performance and during good times, their performance fees would be high but low during bad times.

That being said, the revenue split might differ in the future due to change in strategies. Companies are constantly evolving and copying their competitors strengths. For example, more companies are getting into insurance as it is a good source of funding to earn management fees which I will be discussing under the tailwind section.

Management

Bruce Flatt, the mastermind behind the rise of Brookfield didn't seem to get enough attention from his track records. He has outperformed the market with a 20 years 19% investment record. According to an article from Forbes, Flatt is known as Canada's Warren Buffett.

Flatt has been called Canada's Warren Buffett not only because he's a contrarian, long-term investor but also because his investment strategy relies less on price than on patience and the power of compounding income streams. "We will pay more for quality because in the fullness of time, real assets will generally always go up in value," Flatt says. "We'd rather earn a 12% to 15% net return over 20 years than a 25% return over three."

It is also hard not to attribute the firm success to his partners. All of them have roughly 20 years of experience at Brookfield and they act like a partnership. Each runs a big international business and, Flatt says, "any of the four others could run this company."

Control/ownership

Brookfield Asset Management has two classes of shares. Class A shares are traded on public exchanges. These shares give owners the right to vote for half the board of directors. Class B shares are owned entirely by insiders and give those owners the right to vote for the other half of directors. This article has a good overview of their ownership structure:

“The ownership structure of Brookfield is even more complicated. But the basic idea is that the managers of Brookfield, called “partners”, are the stewards of the class B shares and commit to investing a substantial portion of their net worth in class A shares as well. Brookfield believes this creates stability and will reward partners committed to growing the business.

Essentially, there are about 50 “partners” who are former and current managers of Brookfield. They in turn own all the outstanding class B shares through a company called Partners Ltd which is partly governed by what is known as the “BAM Partnership”. Control of Brookfield’s class B shares gives the “partners” the right to elect half the board of directors. From this control position, the partners can guide the direction of Brookfield without having to hold a majority economic interest.”

If a “fundamental disagreement” breaks out among this inner circle, a designated back-up set of directors — which includes former British civil servant Gus O’Donnell — would temporarily take over the group’s powers as reported by Financial post. Flatt and his predecessor Jack Cockwell each control a third of the trust, with the remainder split evenly among five senior colleagues.

Although the partnership collectively owns 20% (Flatt has the biggest stake at 4.18% stake) of the company, it has the voting power to overrule the rest. The management is arguing that the partnership model is likened to Goldman Sachs’ former partnership. Power concentration could be a good thing if the management has high integrity, calibre and putting shareholder interest first but it is rarely the case.

Incentives

The thing about tightly controlled organisations is that the management is rewarded based on the board discretion and it is supposed to be aligned with shareholders interest. There is no outline on how their performance is being measured such as using metrics of return on invested capital, revenue growth,etc.

Although the management has emphasized that a majority of their interest is tied to the company with close to 10 years of vesting period, this does not mean that they are working in the interest of shareholders. As a result, to invest in this company, there is a need to have high confidence in the management capability.

Other issues

Other issues like bribery and corruption remain with the companies and it is running in many of their subsidiaries. In 2012, for example, Brookfield was hit with a civil lawsuit in Brazil, as well as an SEC and Department of Justice investigation for alleged bribery by some of its employees. The SEC and DOJ investigations closed with no charges. Or dealing with Jared Kushner (Trump daughter in-law) by paying $1.3bil upfront for his ill timed assets bought at around $1.8bil- the 666 fifth avenue.

Bonus article : The Paper World of Brookfield Asset Management. It talks about BAM earnings quality and heavy reliance of RPT. Although the article is dated in 2013, some of the information is still relevant.

Total addressable market

Source: Company Fillings, TQI Capital

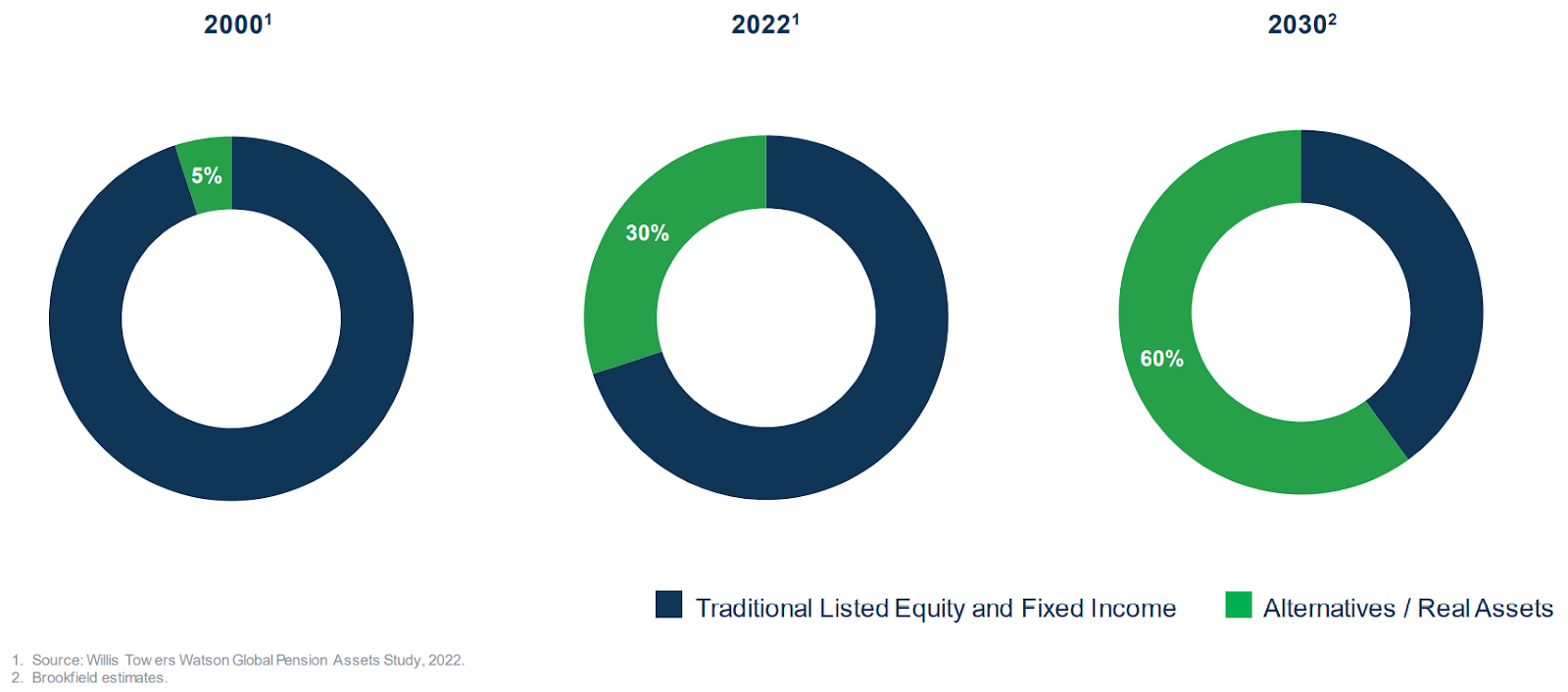

The long term bull case for the industry is the shift of fund allocation by Institutional investors. When an institution is getting bigger and chasing for higher return, there is no doubt that there will be more allocation of funds to alternative investment. Other growth would be coming from retail investors such as HNW individuals that have the money to diversify their exposure.

Let's take a look at the global assets, as per CAIA, global assets are worth around $153trillion and alternative assets make up $18trillion or 12%. It is still small as compared to other asset classes and there is definitely more room for expansion when the barrier to invest in these asset classes is lower.

This is why Brookfield has a target to hit $1 trillion fee paying assets by 2027 or 2.5x of its current fee-paying assets. There will be challenges to raise an average $100 bil for the next 5 years unless they are able to acquire more companies. However, it is not impossible given their size. For example, in 2021, BAM successfully raised $100bil for 15 of their funds. However, fundraising activities slowed down in 2023 due to the possibility of recession.

Tailwind

Asset Under Management (AUM)

AUM is the single most important metric for all asset managers as it is directly related to the size of fees. For context, their fee paying capital has been growing at 27% CAGR for the past 6 years. Besides, their uncalled capital is also growing quickly and it is reaching $87bil in 2022.

Source: Company Fillings, TQI Capital

Assuming a 1% take rate for the uncalled capital, it will potentially add another $870mil of fees revenue for years to come.

Area of growth

Below is a breakdown of their investment by industry

Source: Company Fillings, TQI Capital

Management is actively growing their fee paying capital by expanding into other segments such as credit. The fastest way to grow was to acquire a business. Thus, in 2019, the company made an acquisition of Oaktree, a fund run by the legendary investor Howard marks. The firm paid about $4.5bil to acquire 62% of the business and Howard will continue to run the business until 2029.

Based on some bull analysts, the rationale for acquiring this business is not only for diversification (hedge for high interest rate) and helping to fund their real estate portfolio, it is also their masterplan for something bigger. Brookfield is trying to replicate the success of Apollo with the help of their new insurance business.

The idea is rather simple in theory. Certain types of insurance products, such as fixed annuities, are long-term in nature. An insurer faces a payout many years after receiving money from an individual (or a company in the case of a group annuity) which makes annuities suitable for funding private credit. This channel is already working remarkably well for Apollo.

Insurance

Brookfield is in the process of building its insurance subsidiary which is expected to contribute to assets under management at scale quite shortly. For example, in 2020, Brookfield formed Brookfield Reinsurance and in 2022, it completed its acquisition of American National in an all-cash transaction valued at approximately $5.1 billion.

This acquisition was a necessary step as Brookfield now has a capable underwriting group with various insurance licenses in all 50 states and an ability to grow its insurance business organically. But the key prize was ~$30B in an insurance float that Brookfield was about to invest more profitably. It is like a perpetual capital that Brookfield could use for reinvestment and eventually, it will be a major source of fee paying capital.

Infrastructure

Source: Company Fillings, TQI Capital

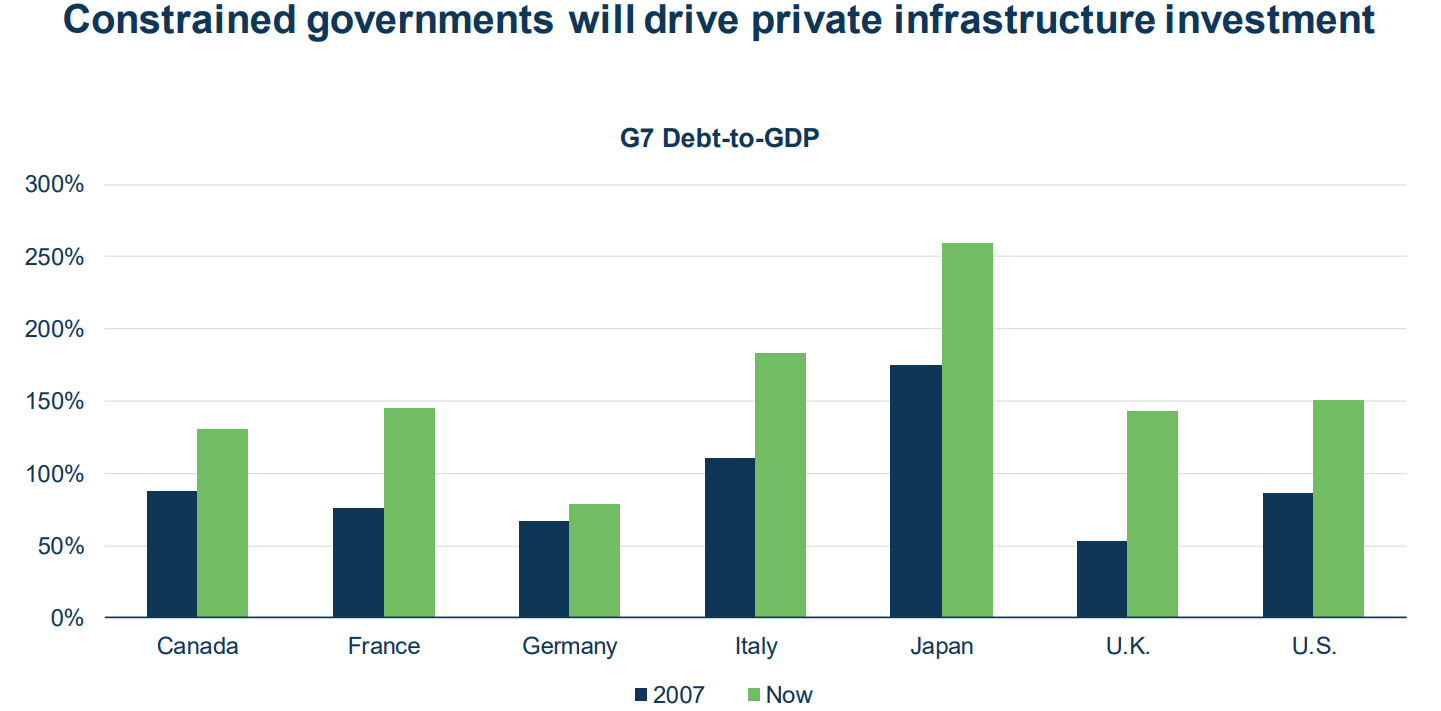

Besides, management also believes the private alternative investment industry is poised to grow further especially infrastructure related projects as governments are constrained with debt to fund for these kinds of projects. For example, G7 Debt to GDP has exceeded 100% and there is a limit on how much it can grow. Thus, future investment will mainly rely on private funds and this will drive the company's future growth.

Risk and challenges

Interest rate

Brookfield asset management (old BN and BAM) has been operating under an artificially low interest rate and benefited from it for the past 20 years. Most of the projects they invested in achieved an outstanding return at around 10%-20%. However, under higher interest rates environment, the return might not be great due to:

1) real assets are highly sensitive to interest rates as it will affect their valuation. It will reduce the overall return upon realisation

2) cost of funding will be higher (as they are usually highly levered) and bring down the profitability of asset owners

Since they have high exposure in real assets and their fees are tied to their fee bearing capitals as well as their performance, their precious recurring fees might be disrupted. Of course, I am not trying to be a macro analyst to predict the direction of interest rate, but a persistent high interest rate will definitely affect their business.

Source of fundings

Brookfield has been opening its gate to more customers such as High Net Worth (HNW) individuals, retail (usually has a shorter lock up),etc to increase their fee bearing capital. A good example of this would be Blackstone non-traded REITS, a credit vehicle to individuals via independent distribution channels (banks, broker-dealers, etc.)

However, when many investors want to exit simultaneously due to some financial stress, the vehicle quickly becomes illiquid. It recently happened with investors in Blackstone non-traded vehicles and may or may not have consequences for the industry.

Given low retail wallet share (5% of BAM committed capital), if they succeed in penetrating the “retail opportunity”, there will be change in funding base and style drift. Although it expanded their TAM, this would dilute the quality of their fundings and it could look like today’s mutual funds companies as argued by Red Deer investments. Their funds will have a low lockup period and their clients could easily move around to other funds.

Don’t get me wrong, economy of scale is still a good moat for the investment industry as additional fee bearing capital will only give them more profitability due to operating leverage such as Vanguard. However, their fees will be less predictable and it moves against their strength of having highly sticky funds.

Conclusion

Brookfield asset management is an interesting company that was spin-off to free ride the resources from its holding company. It has all the characteristics of being a good business such as asset light, high margin, low reinvestment capital, huge TAM, etc. There is also a meaningful upside to these returns if the asset management business earns performance fees on its AUM.

However, an interesting development from most fund managers was that they are selling off their stake in BAM and keeping BN, the holding company. Even their CEO, Bruce Flatt has recently sold off part of his holding in BAM to purchase BN. It is definitely head scratching given BAM is relatively more straightforward, has stable earnings, no debt and generates higher return on investment.

Some explanation could be that BN is relatively undervalued as referred by Baskin wealth management:

A 75% stake in BAM worth $39 billion,

Stakes in Brookfield’s publicly listed affiliates Brookfield Renewable Partners, Brookfield Infrastructure Partners, and Brookfield Business Partners worth $20 billion at current market prices

Various stakes in BAM’s funds valued at $12 billion,

Brookfield Property Group (BPG), a large portfolio of malls and office towers around the world

An insurance business focused on annuities with about $4 billion in equity value,

100% share of the net carried interest (i.e., performance fees) charged on existing funds managed by BAM and a 1/3 share of the net carried interest on new BAM funds.

There also could be substantial mis-pricing driven by excessive pessimism over commercial real estate. Ie: BPY, a property holding company of BN has defaulted 2 loans due to vacancy and high interest rates. However, BN has a non-recourse structure in which a failure in one of its assets/companies will not affect the others.

All in, the company is fairly valued based on my above valuation and it could be a decent investment by investing in this high quality business. Assuming the business could be growing at 9% +4% of dividend yield, it could easily generate 13% of return for the next 5 years.

Disclaimer: I have position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion.

Resources

How Brookfield And Peers Make Money And How You Can Participate In 2023 by Alexander Steinberg (Must read as he is really good at explaining BAM and BN)

Brookfield's Bruce Flatt: Billionaire Toll Collector Of The 21st Century by Forbes

Brookfield Asset Management: A Classic Special Situation by Eagle Point Capital

Brookfield Asset Management by VIC

The Paper World of Brookfield Asset Management by the foundation for financial Journalism

Nima Shayegh - Brookfield Asset Management by Colossus

Some Initial Thoughts on Brookfield's Oaktree Purchase by Concentrated compounding

Meet our bargain-hunting, globe-trotting, skyline-dominating, ruthlessly smart CEOs of the Year by ROB Magazine

Source: 2021 annual report - BN related companies