$IT: The 800 pounds of gorilla within the research firm industry

$IT: The 800 pounds of gorilla within the research firm industry

Gartner: The toll booth for software companies

Before i start my post, i would like make an announcement on my latest posting frequency. I will be reducing my post to only once a month implying that there will only be 12 ideas a year.

The reason being that only great ideas will be presented to my fellow readers and with high filtering criterias, the investable universe will only shrink further. Besides, to improve my quality of research, it also requires more time and effort to do so.

That being said, i am still keen on completing my goal to present 100 high qualify companies and committed to do so. A step at a time.

Company: Gartner

Ticker: IT, listed in US

Industry: Technology, Research & Analytics

Investment thesis

Sources: Gartner website

Have you ever seen these diagrams before? It is known as the Gartner Magic Quadrant and Hype Cycle. Gartner, founded by Gideon Gartner, has revolutionized the landscape of research on industry, especially on information technology. He was known as the father of the modern analyst industry.

*The year Eugene Hall joined as CEO (current CEO)

Sources: Company 10k fillings

The reason that got me interested in Gartner is its ability to compound both its growth of revenue and free cash flows consistently over the years. As a result, it is not surprising that its performance has easily beat the market by compounding 13% for almost 40 years. (110x since IPO). It is intriguing to learn about the company and how it manages to achieve it. (Note: it shares the characteristics of great companies: asset light, long runway, high margin and operating leverage)

Section 1: Gartner history: how it was founded and became the industry leaders

Section 2: Gartner business model and operating segment: I discussed its key products and growth profile

Section 3: The Industry and Competitive Dynamics: Gartner addressable market, competitive moats, and current competitors are highlighted here

Section 4: Management, Capital Allocation, and Incentives

Section 5: Conclusion

Section 1: Gartner history

The company was incorporated in 1979 by Gideon Gartner (unfortunately, he passed aways in 2020). Formerly an IBM employee, Mr. Gartner initially focused on helping corporate customers decide which IBM products were best suited for their needs.

Before Mr. Gartner’s foray into the business, the research sector produced thick 200 to 300-page reports for clients, which often sat on shelves gathering dust. IT managers were hungry for concise and accessible information and advice. Mr. Gartner insisted that Gartner Group reports could not exceed two pages.

Short and comprehensible was the format, but more importantly, the research had to be of the highest quality. “He brought a Wall Street research approach to the IT industry,” said George F. Colony, founder and chief executive of Forrester Research, a rival firm.

Subsequently, the company IPO’d in 1987, was purchased by British communications firm Saatchi & Saatchi for $90mn a year later, was bought back by Gartner’s management team in an LBO assisted by Bain Capital and Dun & Bradstreet in 1990, and re-IPO’d in 1993.

Gartner reached its new peak when it introduced its best known product - Magic Quadrant as shown below. It has taken the research market by storm and attracted a lot of attention. Subsequently, it became the industry standard for IT products classification and its competitors introduced similar products to compete as shown below.

In conclusion, the foundation for Gartner is always about Information technology. However, with its new CEO, Eugene Hall joining in 2004, he is determined to push Gartner further as there is so much opportunity lying ahead of them.

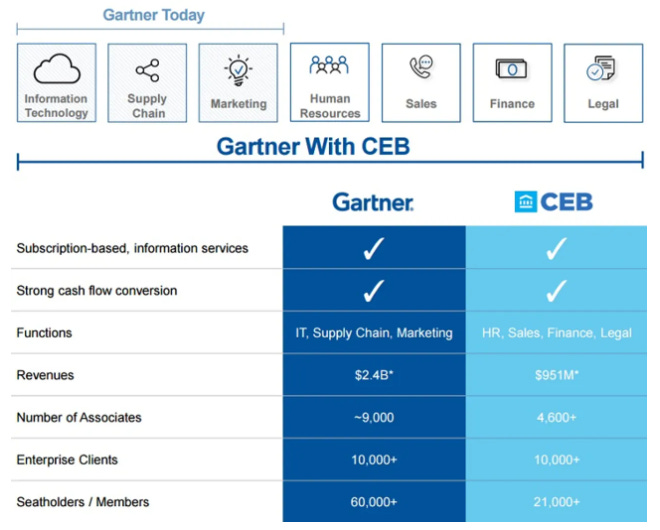

They are not going to stop at the IT department. Gartner made its first move to diversify into supply chain technology by acquiring AMR in 2009, organic launch in 2012 to expand into Marketing technology. The final touch for Gartner is to extend its tentacles into the remaining functional departments (HR, sales, finance and legal) with the purchase of CEB.inc.

Section 2: Gartner business model and operating segment

Source: Annual report 2022

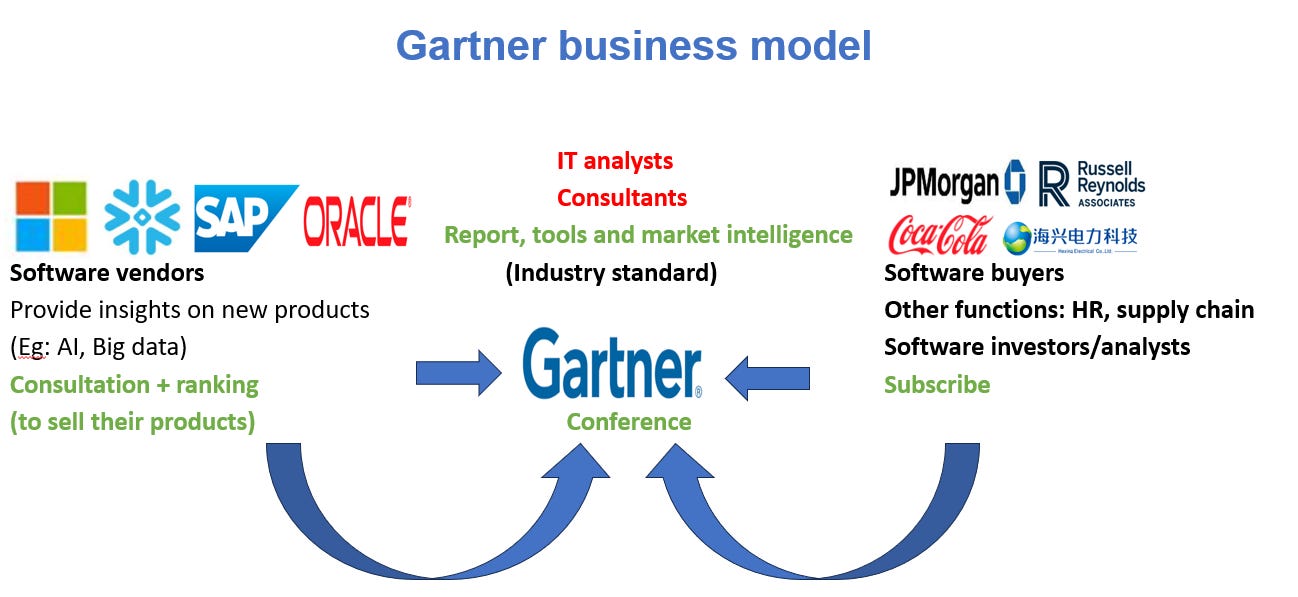

The above graphic clearly illustrated how Gartner made money. Basically, Gartner made money by becoming a “platform” for both vendors and users to purchase or sell their products, especially for the IT industry. It is literally the toll booth for software sales.

To be absolutely clear, Gartner only provides information/tools to help users to make decisions or measure performance. There is no involvement in the deployment of software implementation. It is different from IT service providers like Accenture or EPAM that actually assist with the IT transitions.

Sources: Company Filings

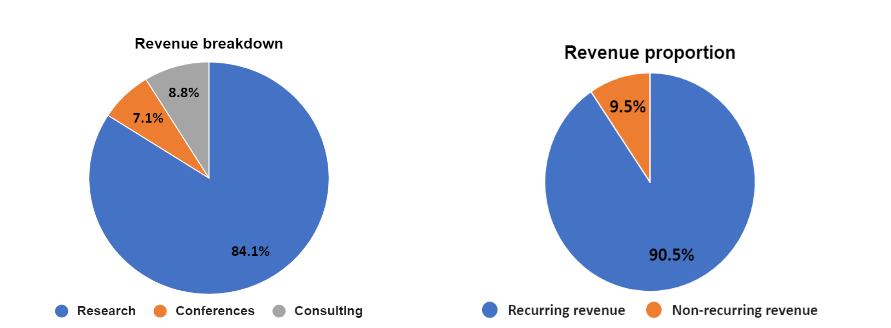

Let's explore how it has evolved over the years. In 2022, Gartner reports its operation into 3 segments: Research, Consulting and conference. Most of the revenue is recurring and I will be discussing them separately.

Recurring revenue

Let's start with Gartner core business.

Source: Company 10k fillings

Research (85%): Within this segment, it includes Global tech sales (GTS) that sells products and services to users and providers of technology while Global business sales (GBS) sells products and services to all other functional leaders, such as human resources, supply chain, finance and marketing. It is the most profitable segment with an average contribution margin of 72%.

For these businesses, it is on a subscription basis and the users have to pay upfront. As for the contract term, it has a minimum contract period of 12 months and 70% of their contracts were multi-year. (bulk of it is 2 years)

Non-Recurring revenue

Source: Company 10k fillings

Consulting (9%): Providing consultant services to CIO or other senior executives to help drive technology-related initiatives. I believe it also includes consulting services that “helps” their smaller software vendors to improve “ranking” so that they could sell their products better against bigger vendors.

It is the least profitable segment due to the cost of each consultant being expensive. The average contribution margin for this segment is around 33%.

Source: Company 10k fillings

Conference (7%): Organizing conferences, workshops and events including its unique flagship IT Symposium/Xpo series. Both vendor and customer usually use these events to network or socialize. It became a must go conference for tech specialists and it is crucial in ensuring a steady flow of new vendors and customers.

Gartner typically made around $6k revenue per attendees and it is a lucrative opportunity as the contribution margin is often as high as 50%. This is an important part of the company's strategies to bring new leads and build connections with potential customers or vendors.

Section 3: The Industry and Competitive Dynamics

Sources: Gartner 2023 presentation slides

With Gartner diversification into other sectors, its TAM has expanded over the years to reach around $200bil. For the IT sector, it has around 6.5% market share while 0.7% for the rest of the market. Even if Gartner was to grow 15% for the next 15 years, it will only be 15% of the current addressable market, suggesting that there is still a long runway for the company.

Competitive landscape

Gartner is definitely the 800 pounds gorilla within this space with their revenue 10x its nearest competitors, Forrester. Its competitor 2022 operating margin is only 6% while Gartner is around 3.5x higher. It shows that scale matters in this case and Gartner being the biggest has benefited from the operating leverage.

The market is relatively fragmented with the top players like Forrester, IDC, Frost and Sullivan, etc making up less than 10% of the market share. There is no doubt that the research report industry was commoditised and its competitors could easily copy their products which explained the fragmentation, but it is likely that the industry will consolidate further due to the acquisitions made within the industry over the years.

However, what separates Gartner is not only its products, but also the ecosystem that was created by Gartner as well as the carefully nurtured C-suites community. Read further to understand Gartner Moat.

Gartner ecosystem

The success of Gartner lies in its carefully curated ecosystem. Gartner is a master in building a platform. First of all, it takes Gartner years of efforts to build the best brand within the IT industry analyst firms. It has literally become the industry standard for anyone who is interested to peek into the IT industry.

By positioning themselves as the leading players, It has the share of mind moat and it is crucial in defending their territory. The beauty of being a default in the industry is that competitors have to spend relatively more to acquire each customer. The cost of acquisition difference allowed Gartner to maintain above average margin while charging a reasonable price.

Subsequently, their conference business comes into plays. It is one of the most important funnels for Gartner to gain leads as it has the reputation to attract top decision makers such as the C-level communities (either vendor or buyer) for networking purposes and learning about the industry. As there is more interaction between the participants, it will create connections that help to cement more solid relationships between them.

Then, its consultant/salesman becomes the deal breaker that nudges them into closing deals as they are seen as the knowledgeable and “independent” (i will discuss the independent part later) parties that should know more about the products or services. This certainly helps to give confidence for more deals to happen within the Gartner platform.

Besides, with their expanding database and information, Gartner will be able to create a benchmark for their customers to measure the performance of the software against their peers. It is an important catalyst for their customers to continue to upgrade their products.

Secondly, given the increase in complexity in software products, Gartner becomes the ultimate “filter” for new customers with the Magic Quadrant as they have a team of analysts constantly researching about the topics. Take Cybersecurity as an example. As per an analyst covering the space, industry expert firms are gaining more grounds due to it being a complex space to navigate because the market itself is incredibly crowded.

“There is a never-ending list of “me too” vendors in each of the sub-segments commonly abbreviated by few-letter acronyms that can take a long time to untangle - SSPM, CSPM, EDR, XDR, NDR, SASE, DLP, ZTNA, SDP, NGFV, IDS, IPS, IAM, VPN, SSO, UBA, UEBA, WAF, FWaaS, MDR, CASB, SIEM, SOAR, XSOAR, AV, and many more.

Each of these and other market sub-segments features a broad range of vendors offering seemingly identical tools but positioning them differently, often claiming a creation of a new market. The functionality these products offer overlaps between and across different categories. To make matters worse, there are anywhere between 3000 and 10,000 vendors in the industry (the number depends on which source you use). “

And perhaps most important of all, Gartner provides a ‘CGW’ (Can't Go Wrong) benefit for users. Similar to how purchasers of IT ‘couldn’t get fired for choosing IBM’ once upon a time, choosing a product blessed by Gartner (e.g. in the top tier of its Magic Quadrant) gives executives the ability to outsource the blame if they end up choosing the wrong vendor.

As for the vendors, it is a similar case where new or existing vendors would want to list their latest products in the most crowded platform as it gives them the highest exposure for the client base. Since there is a “limited” spot to be listed in the Gartner ecosystem, vendors are willing to invest a lot of resources such as educating Gartner analysts for free on their new products, paying them a fee for obtaining the highest ranking,etc.

This will undoubtedly reinforce the Gartner moat as they obtain proprietary information for free and subsequently resell the information to interested parties like investors or securities analysts. On top of that, Gartner also could collect more information than their peers and “sell” the information flow back to vendors so that vendors can tailor the products to their targeted customers.

The value proposition is that the investment made by vendors would easily be paid off if they managed to attract the attention of the top decision makers. That is why the top players in the IT industries such as Microsoft, Oracle,etc are willing to pay top money for the spot. It is one of the best funnels to sell their products or at least gain exposure from it.

Strong pricing power

Gartner contracts usually make up a small portion of the client budgets, especially for big tech companies like Microsoft, Google, SAP,etc. On average, both GTS and GBS customers paid them around $260k and $200k respectively annually. For comparison, Microsoft spent $22bil annually on sales and marketing expenses. As a result, It has a lot of room for growth especially on pricing. (increasing by 5% since 2020)

“Yes. So we've had larger-than-usual price increases over the recent past, because of accelerated inflation. And we've had, I'd say, essentially zero pushback from our clients on it. And if you look at the cost of Gartner for an individual user or for even a contract for the company, it's a small ticket item.

And whether it increases 3% or 7% isn't a swing factor. The swing factor is the value we provide. And we provide a tremendous better value to these clients for the costs that they have to pay, spend any alternative and can provide some credible value. So we have had, I'd say, kind of, no measurable pushback on our price increases, even though they're at higher rates. Eugene Hall, Q4FY2022.”

Negative working capital

Lastly, since Gartner is paid upfront, they are essentially supplier funded. The negative working capital helps to fund Gartner expansion such as increasing its sales workforce, consultants and research analysts to further reinforce their scale advantage. This “superpower” has helped to separate Gartner from its nearest competitors. Look at the steady build up of deferred revenue over the years, it is pretty impressive!!

Source: Company 10k fillings

Bear argument

There will never be a perfect company and it is the same for Gartner. Below is an argument by the bears.

Conflict of interest

The biggest bear theory for Gartner will be their appearance of being independent. This is because most of the time, when Gartner is looking to beat the Wall Street estimate, it will likely promote the companies that paid the most instead of the best products. It suffers from the similar fate as Moody as as their fees are typically paid by the issuers.

Of course, Gartner will argue that they don’t make decisions for the clients but when they conveniently omit the best option from the list of choice, there is no doubt that their customers will likely pick from the recommended options. This pay to play model is essentially controversial and it has attracted lawsuits to Gartner. For example, as extracted from one of the analysts blog:

“In 2014, Gartner was sued by NetScout once again claiming the “pay-to-play” model. NetScout argued that "Gartner is not independent, objective or unbiased, and its business model is extortionate by its very nature. Its substantial success is due to the worst-kept secret in the IT industry:

Gartner has a 'pay-to-play' business model that by its design rewards Gartner clients who spend substantial sums on its various services by ranking them favorably in its influential Magic Quadrant research reports and punish technology companies that choose not to spend substantial sums on Gartner services." The judge eventually granted Gartner motion to dismiss the NetScout lawsuit.”

One of the smaller competitors also teased that although Gartner being one of the largest research firms, its analysts only made up a small portion (2.2k/19k=12%) of the company's workforce while salespeople made up 25%.

Despite that, there is a good reason for that as C-suites usually have limited knowledge on certain fields and need a salesperson to explain the value created by its research report. As a result, its salespeople are the key drivers for them to support its 12-16% contract value growth target. VIC analyst has an interesting way to look at its investment in sales associates.

Regulation

The conflict of interest issues will likely lead to other potential risks, ie: tightening of regulations. It is well known that the industry is loosely regulated. However, if more competitors are complaining about their monopolistic practices, it could be a problem for Gartner. (they tried but not much has happened)

For example, they have to be transparent about the “price” paid by the top vendors to be included in the top bracket of the ranking. It will likely tarnish their reputation of being “independent”. However, my belief is that as long as the content provided by them is value-added, it shouldn’t matter too much since they have the scale to cover the entire functions for a company.

Decentralisation

Bear also argues that gone are the times when “Gartner says” was perceived as ground truth. Today, independent analysts are building up their own brand. For example, the rise of platforms for individual creatives such as Substack enabled many people to monetize their wisdom and community.

Many are starting to realize that they don’t need hundreds of analysts - they will rather pay less, and directly to the few people whose opinions, experience, and insights they value. Having a stamp of approval from a large powerhouse certainly helps, but it is no longer a requirement.

However, the challenge of monetizing insights remains: there is a strong need for solid industry analysis, but it’s not always clear how an independent analyst can make money. If they don’t offer advice and services on top of the market insights they produce, they become a very smart journalist, not an analyst. (Unlikely to be a big threat for Gartner)

Section 4: Management, Capital Allocation, and Incentives

Management

Eugene A. Hall has been the CEO for Gartner since 2004. Hall began his career with 16 years at McKinsey & Company, where he structured and conducted high-impact turnaround and growth programs for a variety of electronics, telecommunications and financial services clients.

Subsequently, he joined Gartner as chief executive in 2004 after serving at Automatic Data Processing (ADP) as president of financial and technology services and then president of major accounts.

Since becoming CEO at Gartner, Hall has led the company to great success. His focus on improved client satisfaction and operational effectiveness, as well as acquisitions has brought the company to new heights. Don’t forget about his right hand man, Craig Safian (CFO) that assists in deploying capital effectively. He has stayed as long as Eugene in the company.

Besides, he is also a very low profile guy (last public interview was in 2011) and it reminds me of the founder of constellation software, Mark Leonard. These are the CEOs who focus on improving the company. As per an interview by Barrons:

“Gene Hall is one of those really great leaders who are not audacious or bigger than life,” says Silicon Valley executive Maynard Webb, who was on the Gartner board that hired Hall. “He’s one of those quiet folks who just gets the job done.”

It is also not surprising that the company is seasoned with an experienced board of directors with more than half of them having stayed with the company for more than 20 years. It does suggest that the company culture remains resilient.

Capital allocation

Management has done a good job in allocating capital. Most of the capital was returned to shareholders as it is a capital light business. As a result, its share counts have decreased by 30% since 2006. As for other cash flow, it is mainly deployed for acquisitions as shown below.

Source: Company 10k fillings

Throughout the life of Gartner. It usually acquires companies that are less than $100mil but there was an exception in 2017 where Gartner is estimated to pay $2.6bill (70% cash + 30% share) to purchase CEB Inc, the industry leader in providing best practice and talent management insights. There will be a quick coverage on this purchase as it is the biggest acquisition made by Gartner.

Acquisition

It is generally good to see that the company lists out all their acquisitions in their website since 2004 and is transparent about it. The company has made 36 acquisitions since its IPO. Click here to see more.

CEB inc - Gartner paid $3.6bil or 4x P/S (share price increase in value) or 14x LTM EBITDA-25% for CEB inc. (Note: Gartner sold its talent assessment division for $400mil as it didn’t fit into their acquisition criterias. So, the net purchase price is around $3.2bil )

Since the acquisitions, it has been growing at around 14% annually as it is leveraging on Gartner scale and brands to improve its wallet share and retention. Assuming it can grow by 12% annually for the next 5 years at a 30% EBITDA margin, it could be generating a 16% ROI. (It is certainly not a bad deal for a fast growing business)

Sources: Gartner 2017 presentation slide

The rationale for acquiring CEB is that IT products and services are not only going to be prioritized by IT industries, but also other industries players. It is a growth driver for Gartner and more crucially, gives them the required expertise to penetrate midsize enterprises.

Management ownership and incentives

Management in overall owns about 4% with the CEO owning around 1.7%. Note: the CEO has been selling its holdings over the years but still is a big part of his total wealth (estimated to be $490mil).

Incentives

It is not surprising to see that the top management remuneration packages are performance based. Eg: CEO pay package comprises 7% fixed salary, 8% bonus and 85% of long term incentive (SARs and PSUs)*. It is good to dissect how they reward their top management as it will affect how they manage the company.

Short term compensation

Sources: 2023 Proxy report

The first one is a cash bonus. The reward is determined based on 2 metrics: revenue/50% and EBITDA/50%. Each year, the remuneration committee will be setting a target and its threshold for growth rate is between 9% to 13%. (subject to change)

Long term compensation

Sources: 2023 Proxy report

As for long term compensation, it is solely based on contract value as management determines that it is the key driver for Gartner to continue to perform well. Each year, the remuneration board will be setting the threshold for entitlement with a growth rate between 10% to 15%. (subject to change)

The weighting for its reward is split into 70% PSU and 30% SAR and these awards have a 7 years exercise term. It is to align their interest to shareholders. In overall, the metrics thresholds are fairly reasonable (not easy for a $5bil sales business to grow low double digit).

*stock appreciation rights (“SARs”) and performance-based restricted stock units (“PSUs”)

Section 5: Conclusion

There is no accident that Gartner became the market leader in the industry. It is due to their carefully curated ecosystem that I have discussed earlier - being the ultimate platform for software transactions. Besides, there is also a strong tailwind on digitisation as well as future technology advancement (AI, big data, IOT,etc + who know what else) that makes insights more valuable into the future.

Coupled with strong leadership (Note: Eugene might be retiring soon as his contract will end in 2026. it is just my pure speculation) and capital allocation, they will likely perform well in the future. Gartner is likely to remain the centre for the IT transactions and continue to grab a piece from the high margin IT products and services.

However, like every great company, the company valuation is always trading at a premium except during Covid-19. At current valuation, it is not trading at the margin of safety levels and it should be included in the watchlist in case there is any bargain turning up.

After all the research that I have done, investing is just not easy. Everything is easy to conclude in hindsight but to be able to invest early in Gartner, investors really require foresight. You must be able to predict correctly that technological advancement will overtake the world (worst still that it happened after the dotcom bubble) and Gartner being the ultimate platform benefited alongside. Besides, there is also a need to predict that Gartner is able to recruit a great capital allocator.

Disclaimer: I have no position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. However, i might have position in the future and i might be bias. Invest at your own discretion.

Resources

How to understand whether Gartner is worth the investment by Brightwork research

Gartner research by Value investor club

Gartner, Forrester and cybersecurity: a deep dive into the trends, challenges & the future of the notorious industry analyst firms by Venture in security