$MAR : Without Reservations

$MAR : Without Reservations

How a Family Root Beer Stand Grew into a Global Hotel Company (JW Marriott)

It has been a while since my last research report. There are a lot of ideas out there but most are expensive in my view. I guess that is a problem for a value investor and I am still not willing to pay up for great companies. (How should I fix this?)

I realize that there are no best time to publish a report and I am going to publish one whenever I am ready. Thanks for sticking out with me. Today’s I am going to deep dive into Marriott, a hotel empire that didn’t get enough attention from the investing community. I hope you learn something from this post.

Company: Marriott International

Ticker: MAR 0.00%↑ , listed in US

Industry: Hospitality

Introduction

Sources: Marriott mogul on 55 years of change in the hotel business by CNBC

JW Marriott initially started in the restaurant business. In 1927, Hugh Colton and J. Willard Marriott pool $3,000 each to finance an A&W franchise, root beer concentrate in 1927. Later, a hot food is added and it was name as the Hot Shoppe. The company continue to grow until Bill Marriott, the son of JW Marriott joined the company and decided that the company should focus on lodging business instead of the restaurant businesses as it is highly competitive especially with the rise of Mac Donald and other fast food chains.

Twin bridges hotel was the start of the Marriott empire. From there, the company continues to build hotels all over America but the real growth are coming from the international markets. With tough events like real estate busts in the 1990s, 9/11 in the early 2000s, Covid-19 in 2020s, the company persist and eventually became the empire that we saw today.

Below are the outlines on my report:

The business model : I discussed how it transforms from a typical hotel owners to an asset light management company?

The industry dynamic : For this section, I explained the potential headwinds faced by Marriott due to the side effect of the pandemic and technology.

The competitive dynamics : I explored the good old days of Marriott and how the rise of the Online travel agency (OTA) like Booking or Airbnb are trying to make them irrelevant.

Bull vs Bear: It is the section which I combined the argument for and against investing in Marriott.

The management and capital allocation: I explained how the leaders in the company make a difference.

Conclusion: I summarized my thesis and thoughts on why I think Marriott will remain relevant even with technology disruption

1.Business model

The hotel industry has always been tough due to the fact that it is capital and human intensive. Besides, it has low barrier of entries and competitors could easily grow with banks happily financing the deals. Lastly, hotel chains are restricted by their pace of building hotels which make it significantly tougher to expand quickly.

Imagine forking out millions of dollars upfront, spending 2-4 years to build up a hotel, managing a pool of employees that has high turnover, the return on capital is simply average or below average. (due to no moat/competitive advantage)

Marriott used to follow the playbook of a typical hotel where it developed its own hotels and managed it. Then, they expanded aggressively by building for other assets owners in return for management services. Lastly, they pivot by spinning off its property development arm, Host hotels & Resort due to the lesson learned from the 1990s real estate bust (They became highly leverage by overbuilding its hotels).

To day, Marriott International is a different beast. It has transformed into a management service company that provide management services and franchise its brands to hotel owners/property developers. There are over 30 brands under its Marriott International portfolio through either acquisitions or internally developed. It is asset light, high margin and has no restriction on expansion. (a dream business)

Sources: Marriott International website

The benefit of franchising brands is that it could scale in a way physical property could not, and bringing multiple hotels together offered the opportunity for travel agency programs, corporate accounts and loyalty programs. Besides, multiple brands also gave Marriott clients opportunity to scale within the same locations. You can’t build too many St. Regis in the same town without diluting its brand but with Marriott, it gives flexibility to developers/asset owners to own multiple brands in the cities/towns that they liked.

Revenue breakdown

Sources: Annual reports

It earns its revenue from 5 different sources: providing i) management services (5% of Gross revenue) such as hiring, training, and supervising for hotel owners (charging based on % of room revenue). earning an ii) incentive fee (3% of Gross revenue) if they meet certain targets based on the hotel profits, iii) reimbursement from hotel owners (74% of Gross revenue) for the cost incurred from operating the hotels such as supplies, staff costs, furniture, renovation, etc.

It also earns from iv) franchise fees (12% of Gross revenue) for their brands which typically range from 4% to 7% of room revenues for all brands, plus 2 to 3% of food and beverage revenues for certain full-service brands. Included within this category are co-branded credit card fees which they are partnering with JPMorgan and American Express.

Lastly, it also operates its own hotels (26 hotels in US & Canada and 38 hotels internationally), licenses their trademarks for the sale of residential real estate, provides consultation on designs,etc which is classified as v) other revenue (7%).

However, the gross revenue doesn’t depict a true picture on Marriott as reimbursement revenue is simply a pass through and it will be offset with its reimbursement cost. Thus, the correct way to look at it will be on a net revenue basis. If this is the case, Franchise fees proportion will be the largest at 43%, management fees at 19%, incentive revenue at 9% and others at 29%.

These are very high margin revenue due to minimal cost associated with it except the other categories. As a result, the “real” adjusted net profit margin is around 43% which is very high compared to its competitor like Booking.com. (ie: 25% NPM)

Below is a summary of its rooms by regions, types, occupancy and members. An additional growth CAGR for the past 5 years was also included.

* The difference in rooms and regional rooms is due to timeshare

Despite the pandemic, the company manages to increase its room supplies and members at a relatively healthy rate. The most important point to note is that most of its growth came from Franchised which is the best for Marriott as it is capital light and high margin. Both members and room growth are important drivers for the company and there will be more discussions under the Industry dynamic sections.

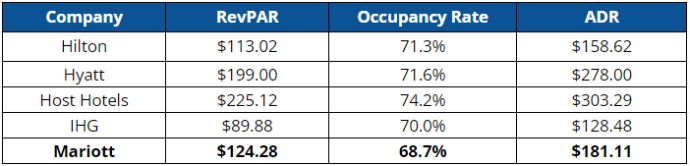

The trouble comes from record low occupancy rates which will affect the Revpar growth (a measure of same-store sales for the lodging industry. It is derived from occupancy x average daily hotel rate). It is the most important KPI for the industry.

My belief is that it will be temporary as travelling starts to pick up, it should recover. Based on the latest Q3FY23, the occupancy rates have rebounded to 67% for both International and 70% for Worldwide. Based on pre-pandemic occupancy, it is around 71% and 73% for both International and Worldwide respectively. There are still rooms for Revpar growth. (as evidenced by increase in both occupancy and average daily hotel rate)

2.The Industry dynamic

The travelling industry has been enjoying a tailwind due to the increasing wealth for the travelers. However, there are some headwinds (for both supplies and demand) going forward.

Room supplies

Firstly, the rooms under construction have been growing slower at 2.5% compared to historical rates of 4% due to factors such as increase in cost of construction, rise of interest rate, etc. Besides, with more competitors changing to a capital light business model, there is more competition for supplies. Below is a data compiled by Morgan Stanley:

So far, the future supplies of rooms are still aggregated (which is unlikely to change) towards the bigger brands like Hilton, Marriott, IHG due to their pricing power and huge number of members. However, Marriott is falling behind on the global shares of rooms under construction/existing shares: Hilton:3.8x, IHG:2.8x and Marriott:2.6x. (Marriott pipeline is around 557k rooms as of Q3FY23 with around 238k under construction)

Business travelling

Pandemic has changed the way businessmen interact. Eg: their preferred choice of meeting could be via Zoom instead of visiting the countries. As a result, there are fewer nights booked by them as compared to Pre-Covid era. How does it affect Marriott’s? Firstly, most conferences or events are organized from hotels. Secondly, when the money is out of the corporate pocket, price will not matter. It is best to choose from high quality hotels. As per The Point Guy (TPG):

“But what really pays the bills for Marriott are all the conferences at large city hotels or the business travelers spending the night at its network of Courtyards, Sheratons and Fairfield Inns”.

Although there is no breakdown in their customers, it is estimated that about 50% are business travelers. (industry average is around 30%) If business travelling is shrinking, Marriott might have to compete for leisure travelers which is more competitive. As per the CEO, there is a new trend of combining business and personal leisure but hard to see how it benefits Marriott.

3.The good old days

Before the rise of new competitors like Booking.com or Airbnb, their model is very much bullet proof. Marriott’s growing network of brands and properties offers a significant and self-reinforcing value proposition to both guests and hotel owners, which creates a strong competitive moat around the business.

For guests: Marriott provides a consistent and reliable experience in a large variety of destinations at various price points, as well as an attractive loyalty program with enhanced customer service, amenities, and awards. A good example is their Marriott Bonvoy membership and its various tiers rewards. Over half of their rooms are booked by members through their membership programs.

For hotel owners: Joining its network instantly helps the hotel owners to gain brand recognition and access to its large pools of loyal customers (190 million). Besides, they are able to leverage Marriott large-scale marketing programs, reservation and IT systems, as well as supply chain purchasing power to compete with other hotel chains.

With their strong branding, it should result in higher revenue per room (due to premium rate) as compared to running the hotel themselves. Thus, Marriott has created a flywheel and it is hard for its competitors to replicate.

Stickiness

Another key point to note will be stealing its supplies is virtually impossible as the contracts are very sticky and costly. For example, its hotel owner has to sign 20-30 year contracts and some contracts can go up to 50 years. Then it has to design and renovate according to Marriott standards which make switching to competitors expensive. Lastly, it has to re-renovate to its competitors standard and the revenue loss while renovating could be huge.

First mover advantage

Marriott also has a first mover advantage due to their long history of operation. This is because most of the hotel owners with prime locations in the early days were signed up by them. Imagine if the locations are located near city centers with easy access, great views, etc, it is hard for competitors to have the same or better pricing power than Marriott.

Coupled with the fact that most of the city centers are mature and new supplies are fairly hard to come by, new entrants will have hard time finding new supplies other than acquisitions which can be very expensive. This is certainly an unfair advantage for Marriott and some of the incumbents like Hilton and Hyatt.

The rise of aggregators

Marriott’s and its peers have benefited substantially from strong travelling tailwinds and cornering the high quality hotel supplies. However, the rise of aggregators like Booking.com or hotel alternatives like Airbnb have disrupted their business models. They have leveled the playing field for small to mid hotel owners as well as shattering the supply bottleneck. I particularly like the explanation by Ben Thompson on how OTA is affecting the hotel chains:

“The rise of online travel agents like Expedia and Priceline (now known as Booking.com) changed the industry significantly, and in exactly the way you would expect: first, online travel agents had effectively zero transactional costs, which meant they could scale up to however many people wished to use their services. Secondly, online travel agents had access to most hotels across chains: instead of going from brand to brand you could simply go to one site and compare prices and availability and then book.”

Essentially, these players are trying to commoditise its supply so that the brands of the hotels will not matter much to its customers. (which is very crucial to the incumbents) Thus, it will be a war for customer relationships. Every single one of them is trying to become the default platform when it comes to travelling.

Surviving as an Incumbent

So, how does Marriott plan to survive and thrive under such a competitive environment? The answer could lie on the below statement written by its ex-CEO when Marriott decided to make its biggest acquisitions, Starwood. Marriott CEO Arne Sorenson (unfortunately passed away in 2019) wrote on LinkedIn:

“We are convinced the greater size will help us stay competitive in a quickly-evolving marketplace. The hospitality industry today is filled with new and emerging options. Long gone are the days when a Marriott hotel competed against the Hilton hotel across the street. Product quality, great service and brands are still important aspects of our competitive landscape. In recent years, however, we have seen this landscape become more and more complex…

Even as the hotel industry itself has become more varied, the methods for planning and booking travel have also become varied — think not just TripAdvisor and Expedia, but Google and Alibaba, all provide services and seek to make a profit in our industry. Then, add home-sharing platforms like VRBO, Home Away and AirBnB. While each is very different from another, they look a bit like a combination of an intermediary and a traditional competitor.

So what do we do? First, we want to expand our offerings to ensure we have the right product in the right place to serve our loyal guests and capture new ones. Second, we want to be big enough to be able to cost-effectively invest in marketing and technology to stay front and center for our guests. Third, we want to have the best loyalty programs in the business. This merger does all that.”

It seems that Marriott thinks that scale could be the key to go against these new players. The rationale is that with scale, they could afford to cost-effectively invest to build a better product, marketing and technology to increase their customer loyalty.

Besides, they could also continue to acquire more international brands to expand their footprint in the international market to mimic the portfolio of aggregators. Of course, there is no way for them to scale faster than these aggregators but it is crucial in offering compatible products/services to their customers so that they don’t even look elsewhere.

4.Bull vs Bear argument

Bear believes that scale only solves part of the problem, which is to maintain its existing customers. This is because the membership will become more valuable overtime as more properties/partnerships are added into it. It is also tough for their members to give up all the points that they have collected as well as the free perks like free breakfast, exclusive lounge, free nights, etc. As a result, their existing customers should remain loyal.

However, their future growth will come from prospective customers and supplies. With OTAs accruing immense bargaining power through its ever increasing listings, their “membership program” is likely to be more valuable. It is like Marriott membership but maybe 2x more valuable as the points can be used for any hotels/services that are listed in their platform. Even these incumbents can’t afford not to list their properties in these platforms due to their global reach.

Bull argues otherwise. Bull draws a comparison with e-commerce. It is true that the competition is heating up as consumers will be able to compare price, location and services easily, but the rise of e-commerce doesn’t dilute brands' power. People still buy branded goods from the platform albeit there is more competition.

In this case, bull believes that brands will prevail and Nike is one of the best examples. Nike has reached the scale to sell directly to customers and do not rely on Amazon (an aggregator) to sell their goods. It is a good indication that good branding should be the ultimate winner. With Marriott's extensive brands portfolio, they should continue to perform well.

Besides, these hotel chains still control millions of rooms globally. As a result, with hotel chains getting larger, they can bargain for better rates. (ie: typical rate is around 15-20% but big hotel chains can get as low as 10-12%) as suggested by this VIC writer. Then, they could pass through the rates to their customer if they choose to book directly with the aggregators. (not much impact to these hotels chain margin)

My bet is that Marriott still needs to rely on these distribution channels as the hotel industry is fairly fragmented. However, they need to find ways to convince their customers to book directly and scale could be a good strategy. Once they are stuck with the Marriott ecosystem, it will be hard to switch.

The real trouble

My belief is that the real issues will be coming from the hotel alternatives like Airbnb, VRBO and HomeAway. Their business models essentially upend the supply constraint (arguably an important moat for hotel chains) and being able to offer at an attractive pricing due to minimal cost associated with it.

Although there are a fair share of horror stories like hidden cameras, inconsistent services, crazy cleaning fees, it is still an attractive alternative to hotels (cheaper on a per person basis). As a result, it is gaining so much popularity and growing to 15% of the US total accommodation room nights over the past decade.

It is becoming obvious that these OTAs/alternatives have an upper hand due to their far superior business model. (Scale, network effects, etc) The best defense against them will be from the regulation point of view. National Hotel Lobbyists have backed the local wars on Airbnb and are hoping for bans.

Their arguments are like when property managers are snapping up houses for alternative hotel uses, it will cause housing shortage and affordability issues or issues like loss of tax revenue as it is hard to trace, etc. Thus some countries or states are banning Airbnb such as New York, Los Angeles, Toronto, Singapore, Berlin, Paris, Edinburgh, Amsterdam, etc.

5.Management

Sources: Marriott history

If anyone wanted to know more about Marriott, “Without reservation” would be the book to go for. It was written by Bill Marriott, the son of JW Marriott. It is an authentic book that describes the company dedication on its people as they are in the people business.

Currently, the Marriott family collectively owns about 12% of the business. It is one of the rare businesses that is owned and run by the family. (The grandson sits as the Chairman) Their stake is significant enough for them to run the business like an owner. In this case, their interests are aligned with the long term shareholders.

The company shares similar characteristics of great companies like promoting internally (only 4 CEOs since inception in 1927), thinking long term, taking care of your employees, etc. Below are some tenets by his son, Bill Marriott’s - 12 Rules for Success from his blog, Marriott on the move (no longer available to read but can be read from his book: Without reservation):

Challenge your team to do better and do it often.

Take good care of your associates, and they'll take good care of your customers, and they'll come back.

Celebrate your peoples' success, not your own.

Know what you're good at and keep improving.

Do it and do it now. Err on the side of taking action. This is one of my favorite rules for success. There is such a thing as “analysis by paralysis” … don’t get weighed down by indecision. Go with your gut.

Communicate by listening to your customers, associates and competitors.

See and be seen. Get out of your office, walk the talk, make yourself visible and accessible.

Success is always in the details.

It's more important to hire people with the right qualities than with specific experience.

Customer needs may vary, but their bias for quality never does.

Always hire people who are smarter than you are.

View every problem as an opportunity to grow.

Arne Morris Sorenson was the first non-family member from the company but unfortunately passed away due to cancer. He is succeeded by Tony Capuano (58 years old). He has been with the company for nearly 28 years and counting. It is likely that non-family members will continue to lead but I believe that their culture will be preserved due to internally promoted practices (about 50%). Most of the top jobs are still held by highly experienced top management.

The management is incentivised based on adjusted EBITDA (60%) and quality assessment (40%) such as associate, customer and owner satisfaction. As for long term rewards (50% PSUs, 25% SARs and 25% RSUs), it is based on TSR which is aligned to shareholder interest. On ownership, the management collectively owns less than 1% of the company. It is still a substantial amount for the CEO at around $40mil worth of shares.

Capital allocation

The most obvious issue with the industry is their debt. Marriott debt/FCF is around 5x. Although these companies have low capital intensity, they are gearing up for global expansion through acquisitions.

Marriott was known for their deal-making skills. Parts of the 30 over brands portfolio was their acquisition effort to build a global portfolio. Marriott is also a share cannibal as they have aggressively bought back their stocks over the years. (share counts dropped by average 3% annually or 21% for the past 7 years)

Acquisition

There are limited deals done by Marriott for the past 5 years because of their biggest acquisition - Starwood and Covid-19. However, in 2023, the company resumed their acquisition activities. There are some hints that Marriott is expanding into affordable hotel chains by first acquiring Hoteles City express for $100mil (in Mexico) and then creating another new brand named StudioRes - targeting budget-friendly extended stay.

The acquisition of Starwood deserves a slightly deeper dive. Marriott made a surprise bid on Starwood at $12.2bil in 2016 at roughly 13 times enterprise value/EBITDA multiple. It was a 0.8 share exchange for every share (resulted in 150mil share issuance) of Starwood and $21 cash or $2.5bil. As a result, Marriott shares were diluted by 55% and was forced to take on debt close to $4.4bil debt ($1.9bil belongs to Starwood).

In my opinion, it is not an expensive acquisition given the portfolio acquired (proceeds of $1.5 billion from disposal of assets) as well as the synergy. It has improved the company's overall margin from 30% in 2015 to 42% in 2022. Assuming that the company improved Starwood operating margins close to the corporate average of 43%, we get close to a high single digit EBITDA multiple or about 12% return on investment.

6.Conclusion

Marriott International remains the largest hotel chain in the world by the number of rooms. It is a different beast from the traditional hotel chains that are capital heavy and low margin. This is because it sells brands and services, thus it is a capital light, high margin business. With its ever increasing portfolio to over 30 brands, it is set to remain the leading hotel chains.

The company's success lies in their ability to secure high quality hotels/properties (very sticky) across the world due to their strong brand name. Besides, with the irresistible membership programs, they have attracted close to 200 millions members which set them apart from their competitors.

However, the good days don’t last forever. The rise of aggregators and alternative hotel providers are eating their lunch. With their ever increasing listings, hotel chains are forced to join the network making their competitive advantage stronger. Despite that, they needed each other to thrive and with Marriott's strategy to gain scale, they were able to bargain for better commission rates thereby minimising the impact on their margin.

The real trouble comes from the alternative hotel providers with the notable player being Airbnb. It is able to create new supplies within prime/remote locations with their unique value proposition - turning residential properties into short term vacation houses.

Besides, it is able to charge a relatively lower price on a per customer basis as compared to hotels. As a result, it has gained so much popularity and is estimated to continue to grow rapidly. That being said, these companies do face challenges such as inconsistent services, regulatory constraints, etc.

Marriott also experienced a slow down in supplies due to developers and competition from peers. Business travelling, another major contributor for hotel chains, also suffered from structural changes due to pandemic. It might reduce their upside in increasing their occupancy.

Lastly, by looking at the bright side, Marriott remains the leading hotel chain with substantial family interest that is aligned with shareholders. Its long term oriented culture, great capital allocation, etc truly stands out within the investing community.

It is not a buy for me for now if we take into consideration its current valuation. I believe the market has priced in too much future growth for the business due to the recovery play of the travelling industry. However, it is a high quality business that passed my threshold. Patience is required and it will be on my watchlist. In case Mr. Market is giving a bargain, it is a buy for me.

I would want to end this research with a letter by JW Marriott to his son:

Sources: Without Reservations

Disclaimer: I might have position in the company and receive no fees for writing the post. I am not affiliated or have any role with the company. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion.

Resources

Without Reservations: How A Family Root Beer Stand Grew Into A Global Hotel Company by J.W. "Bill" Marriott Jr

In The Airbnb Era, This Deal Junkie CEO Built Marriott Into A Booming Hotel Juggernaut–And He’s Not Done Yet by Forbes

Marriott’s new CEO sat down with TPG to talk Bonvoy benefits, hot breakfast and more by The points guys

Competitors statistics by seeking alpha

Note: FY2022