$Morn: Democratizing financial data

A fallen angel - The road to redemption

Company: Morningstar

Ticker: Morn, listed in US

Industry: Technology, Analytics

Investment thesis

It is rare to have a founder that truly follows Warren Buffett closely when they are setting up a company. When I was reading about the Morningstar founder, Joe Mansueto story, it occurred to me that he possesses one of those rare characters that made him so successful- Capital allocation. From his first annual shareholder letters, he uses moat to explain his company's competitive advantage. A term popularized by Buffett.

“In addition to understanding a company’s business model, it’s also important to understand its “economic moat.” This is a term we’ve borrowed from Warren Buffett to describe a company’s sustainable competitive advantage—the barrier that protects the company castle.” 2005 annual report.

Since its IPO in 2005, the market capitalization of Morningstar has expanded considerably by reaching its peak at 10x of its IPO price. However, the company is currently experiencing some setbacks which caused the market capitalisation to drop by a third from its peak but slowly recovering.

For example, although its revenue has been growing at high double digit for the past 5 years, its operating income actually declined by mid double digit and their operating margin shrink to a mere 7% (excluding one-off expenses) as compared to their usual 20%. Based on the latest Q12023 quarter, it is poised to perform worse for the year as it is posting a rare loss for Q1.

It is intriguing to look into the company as it has a history of outperforming the market due to the industry they are operating in. It is an asset light, long runway, high margin and operating leverage industry.

Section 1: Morningstar history: how it was founded and became the industry leaders

Section 2: Morningstar operating segment: I discussed its key products and growth profile

Section 3: The Industry and Competitive Dynamics: Morningstar addressable market, competitive moats, and current competitors are highlighted here

Section 4: Management, Capital Allocation, and Incentives

Section 5: Conclusion

Section 1: Morningstar history

Like so many devotees of Warren Buffett, Joe was inspired by Warren Buffett's no nonsense and easy to understand investment style from reading a book by John Train- The Money Masters. It got him excited about investing and this is where he got his ideas of compiling information on all these super investors holdings in the 1970s. (It seems like Morningstar could be the origin for all the data compilation websites like Data Roma, a popular superinvestor compilation database.)

"These are great vehicles for most people to invest in." Here I can hire the very best money managers in the world at pennies on the dollar, and it's a very democratic notion. Previously, only the Rockefellers could hire great money managers to manage their wealth. Now with funds, Joe Sixpack can go and hire John Templeton, and I just thought it was a cool idea. Extracted from a podcast “Invest like the best”

He didn’t start out with Morningstar as he thinks that he should gather some experience before starting his own business. He started off at a venture capital firm but decided that he wanted to learn more about security analysis. So he left to join Harris Associates, the funds practice value investing and is also the biggest institutional owner of Berkshire. He actually got to cover Berkshire Hathaway and learned about the company inside out.

After a few years of practice, it is time for him to answer to his entrepreneurial calling. The first product from Morningstar was called a mutual fund sourcebook. It was a quarterly, and it covered all of the equity funds in the country. It was a 400 page book including all the information needed such as holdings, investment philosophy, etc. (Remember, all these happened in the 1980s where there is not much information and it has to be collated manually).

The great thing about publications is that people paid them in advance for it to be rendered their services in the future. It created a float that helped fund the growth of Morningstar. This is nothing new as Buffett pioneered the concept by using insurance float and Joe truly makes use of this negative working capital to drive his business further.

You could buy one copy for $32.50, subscribe for a year, four copies for $110. And so I took out an ad, and even before I had to pay the printer to print this book, even before I had to pay Barron's for the ad, money was coming in. Extracted from a podcast “Invest like the best”

As of today, the float/deferred revenue stands at $456mil. It will continue to be a great way to fund their future growth and it is growing very fast.

Sources: Company Filings

Rating and classification

Morningstar started off as a data company but evolved to be a rating business. The first big break comes from their rating and classification system that simplifies investing. It makes investing in funds easy when there are ratings/classification attached to it. Even a layman who has no investment experience could easily differentiate the good from the bad. (Rating 1 means impaired, 5 means exceptional) Below is an example of Morningstar rating a fund:

Source: Morningstar website

However, for it to be successful, they need to create a trustable brand. Coupled with the tailwind from Global Analyst Research Settlement (12 firms included in the settlement agreed to spend a total of about $450 million to provide independent research for 5 years in 2003), Joe doubled down on providing independent, unbiased research and advice. The company built a huge analyst team to take advantage of the situation.

And the analyst team was never told, "Just say good things about a fund." It's "Give your true unvarnished opinion about security." And because you're willing to criticize as well as praise, you develop an unusual degree of trust among your readers. Extracted from a podcast “Invest like the best”

As a result, they earned trust from the end users (the investors that bought the funds from banks) since Morningstar is looking after their interest. It has a cascading effect as more users prefer to use their research/ratings, more wealth managers will have to use Morningstar database.

This has created a flywheel with more companies using their products ranging from big brokerage firms to small financial advisors. They became “Moody" or “S & P” for fund ratings. Subsequently, they expanded their rating services into securities, bonds, ESG, 529 college savings plans, etc.

Section 2: Morningstar operating segment

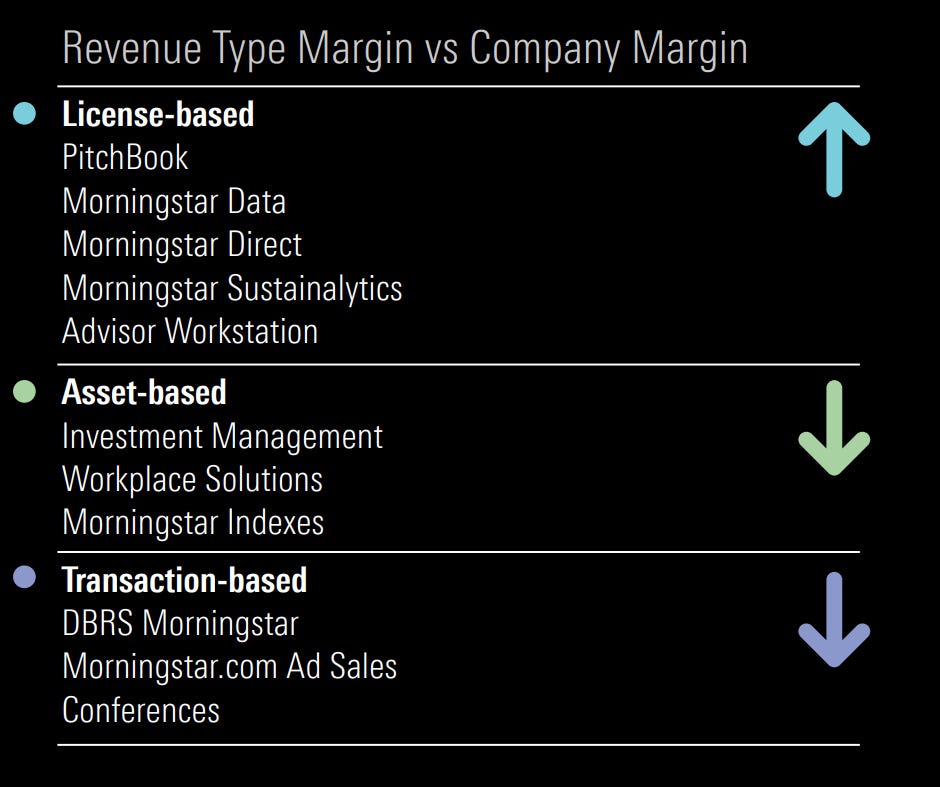

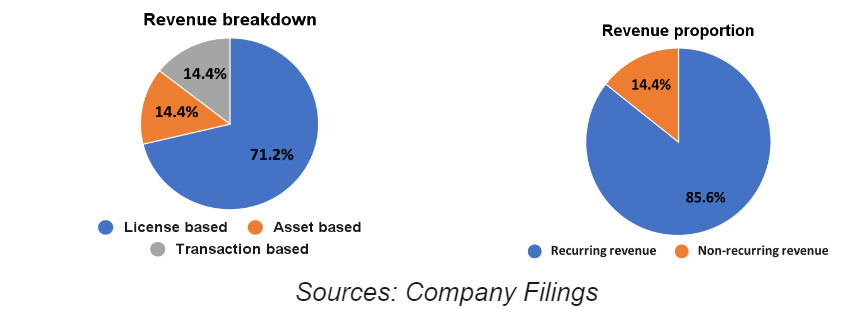

Let's see how Morningstar has evolved. In 2022, Morningstar reports its products into three categories based on revenue models: license-, asset- and transaction-based. Let me discuss them separately.

Recurring revenue

License based revenue

Sources: Company Fillings

License-based (71%): subscription services including Data, Direct, Workstation, premium memberships on Morningstar.com, PitchBook and Sustainalytics. Let me go a little deeper in some of the Morningstar key products.

It is good to start with the core products that build the Morningstar foundation.

Morningstar data is probably the most important product within the Morningstar ecosystem. It is their database that keeps track of millions of data points covering ETFs, closed-end funds, variable annuities, separate accounts, global equities, management and director biographies, insurance-based products, commercial mortgage-backed securities (CMBS), and 529 college savings plans, etc.

It is also probably the most open database where they will license their products to any company that wants to use it. A good example is Bing Finance, google finance, etc. They wanted to democratise financial information and the best way to do it is to be available in any medium of distribution.

Morningstar Direct is for institutions. It is similar to Bloomberg terminal where it provides various data points to institutions for research purposes. Currently, there are 18,421 licenses with an ASP of around $10,032 per license per year. It has grown steadily and served as a very reliable cash generative machine.

Morningstar Advisor Workstation is for financial advisors and specifically targeting enterprise customers. Basically, it is the software that is used by financial professionals, especially financial advisors for data and portfolio management. Currently, they are serving close to 232 clients globally. It used to be a huge part of Morningstar but the share is shrinking due to the consolidation of the wealth management industry.

That being said, it continuously remains as a cash cow for Morningstar to redeploy the cash to other higher growth investments. For their license business, the contracts typically last for 1-3 years.

Lastly, Morningstar.com is the website that provides proprietary research for retail investors. Currently, the memberships are priced at $249/year or $34/month and there are around 108,405 members. With the rise of financial blogging and twitter, they are losing members (peaked at 180,000) but it is still a good source of income, especially the advertising revenue derived from their website.

Sources: Company Fillings

It is time to address the elephants in the room. The 2 key products that the management is investing aggressively for the future growth of the company. It is the Pitchbook and Sustainalytics. It is growing very fast and it is taking more shares for the Morningstar business.

Let's dissect one by one. The founding story of Pitchbook is quite similar to most ambitious founders. It is to solve a pain point and become rich as a result. Gabbert, the CEO of Pitchbook is probably one of the legendary guys that never gives up despite 200 rejections. He discovered a lack of clear research for private equity deals and decided to start his company to solve these problems by becoming the ultimate platform for deal making.

CNBC has a great story about how he cold-called potential investors (including Joe Mansueto, the founder of Morningstar) and eventually sold his company for $225mil to Morningstar. Since then, it has become the core product for Morningstar to drive their future growth. (More to discuss under the section 3)

As for Sustainalytics, it is the company that has partnered with Morningstar for a long period of time before Morningstar acquired it to drive their ESG growth due to the tailwind and high margin potential for the sector. Sustainalytic provides analytics, risk and rating for ESG products.

Asset based revenue

Sources: Company Fillings

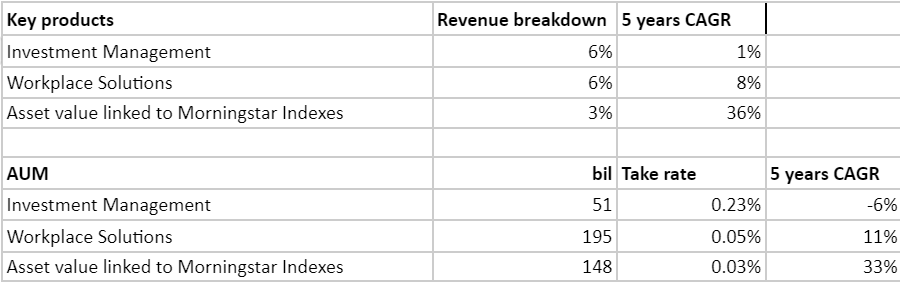

Asset-based (14%): fees collected on AUM in Morningstar’s Investment Management (Managed Account), Workplace Solutions and Index products. It is a highly profitable segment (OPM at around 50%.) It has high incremental profit due to the operating leverage and low operating cost. Note: the disclosure on margin by segment stop in 2016.

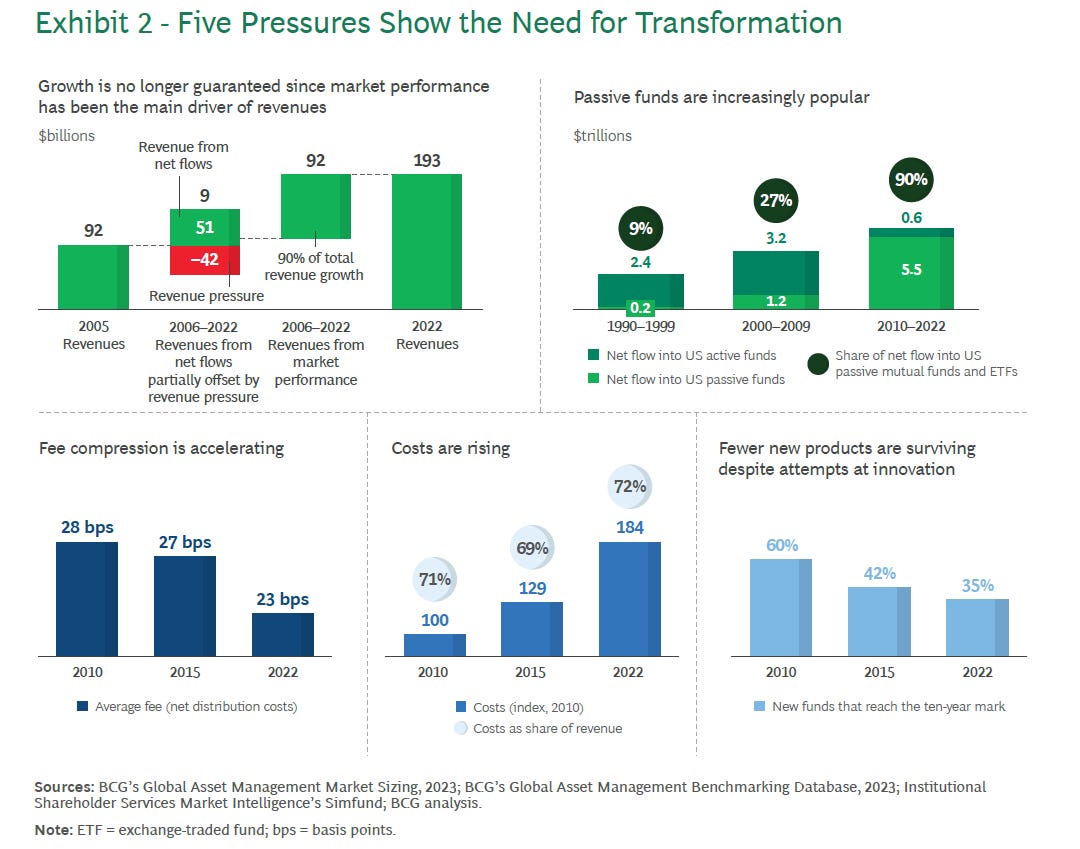

However, there will be some headwinds going forward for the active fund management industry (Morningstar has big exposure in active management) as discussed by BCG such as passive funds becoming increasingly popular, fee compression is accelerating, costs are rising,etc, Morningstar asset based segment might experience margin compression.

Despite the headwind, Morningstar is optimistic about the active fund management industry and is actively improving their product offering. Morningstar Wealth is the latest product (consolidating a few products such as Investment management, Morningstar Office ByAllAccount, etc) that aims to provide a comprehensive, end-to-end wealth platform designed to help independent advisors through every step of their investment workflow globally.

With the rise of 401k in the US (retirement saving plans), Morningstar Workplace solution is one of the leaders due to their unique capability of democratising fund investing (think of their fund ratings). Employees could easily purchase funds that fit their criteria for retirement based on a simplified investing process. For example, Morningstar just completed the enrollment of 11,000 Raytheon Technologies participants, representing about $3.2 billion in assets under management.

Lastly, indexes business (Equity, fixed income, multi asset, alternative, ESG, private market) for Morningstar has been gaining traction as they are riding on the tailwind of passive funds. Besides, they are also offering direct indexing as a solution to assist the financial advisors to outperform the market with lower cost as compared to mutual funds. It is a step taken to compete with the low cost passive funds.

Non-recurring revenue

Transaction based revenue

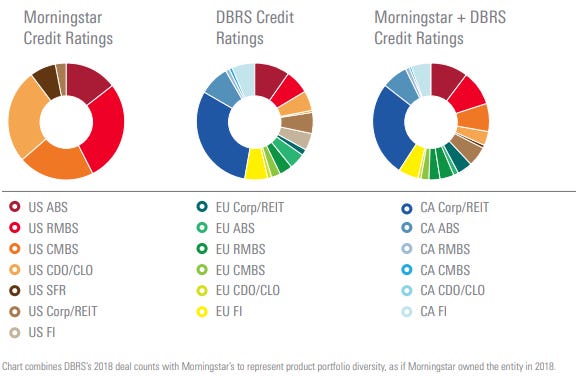

Transaction-based (14%): primarily credit ratings by the ratings agency, DBRS Morningstar, ESG 2nd opinion and a smaller advertising and conference business. The company entered the credit ratings market when it acquired realpoint (focus on rating CMBS and RMBS) in 2009. Subsequently, the company made another big acquisition- DBRS to expand their exposure in different markets such as Canada and Europe.

Source: Morningstar letter for DBRS acquisition in 2018

Morningstar mainly focused on the middle market as it is less competitive in the US (big 3 dominated the credit ratings market). It is definitely more cyclical than the other business but the operating leverage offered them a good opportunity to make outsize earnings.

In overall, Morningstar revenue is becoming less predictable due to their exposure into more cyclical types of revenue.

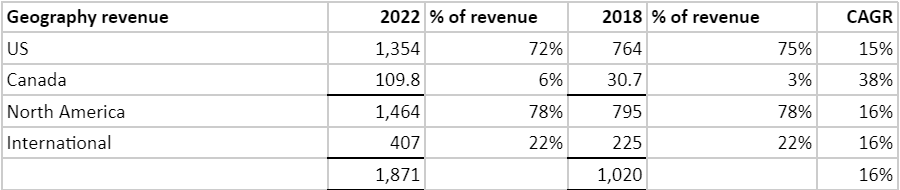

Geographical revenue

Sources: Company Filings

Geographically, the revenue breakdown between domestic and international markets remain similar at 78% vs 22% for the past 5 years despite management ambition to expand globally. Morningstar unable to capture the international market quick enough to increase their economy of scale that will help to increase their margin.

Section 3: The Industry and Competitive Dynamics

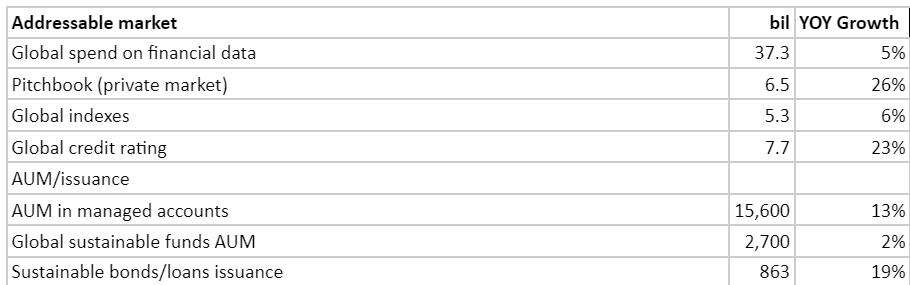

Morningstar participates in a large market. During Morningstar annual shareholder meeting, they made an estimate as per below:

Source: Annual shareholder meeting, 2023

Even though the market they participate in is big, Morningstar is still increasingly investing in areas in which they are new and have no true competitive advantage. I believe that Morningstar has been too aggressive in expanding their business and is losing focus. Let's discuss each segment's competitive advantages and competition.

Morningstar branded license business

Joe has made a pretty compelling case with their Morningstar branded license business (Ie: Data, Direct, Workstation). First of all, it has high customer-switching costs. Morningstar is a classic razor and blades business. Once they install their software, their customer will need their data and research. These data and research “blades'' are time-sensitive and require updating to be valuable.

Besides, it was deeply embedded into their workflows and alot of the customer data was stored within their software. Customers can switch to a new razor, but in a large enterprise, switching can be time-consuming and costly. (Migrating data can be a nightmare and unless there is much better options, there is no motivation to move)

In addition, due to sticky customers (evident by high renewal rate, close to 100%), the float (deferred revenue as mentioned above) will be a reliable source of cheap funding to reinvest back into the business. As a result, when Joe was in the helm (until 2016), the company rarely borrowed money and it was self -sufficient.

Lastly, since they could build one and sell many times, it offers impressive economies of scale with high incremental margins and free cash flows. Joe has truly built an impressive business. However, the slow down in growth for their core business has prompted his successors to search for high growth opportunities. (Due to headwind of active fund management above)

New growth area (Pitchbook and Sustainalytic)

Pitchbook could be the next big thing for Morningstar as it possesses strong network effects. Imagine if you are a P/E or venture capitalist, you would want the most comprehensive database for you to compare and look for ideas. Same goes to the new startup that is looking for fundings, they will be looking for the platform that has the highest chance of success to raise funds. They will happily share their information for free to earn a spot on their platform.

Management understands the potential and has been aggressively collecting data so that more “fuel” will be added to turn their flywheel. For example, it has accumulated 3.6mil of privately held companies information (as of 2023 June) and is expanding. There are close to 2m deals done on the platform.

That being said, Pitchbook is still at its early stage. Their competitors like CB insight, another impressive startup is also rapidly building up a comprehensive database. Don’t forget all the legacies players like Capital IQ, Bloomberg, Factset,etc which have the firepower to compete.

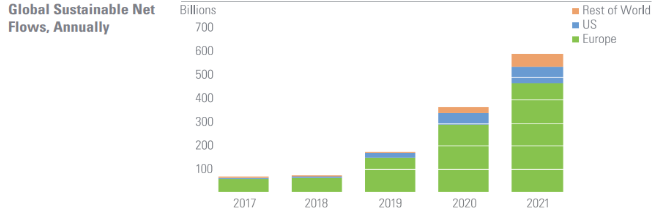

Another area of growth will be on ESG with their acquisitions on Sustainalytic. Morningstar is ramping up its investment in ESG by increasing alot of headcounts in this segment to build up their database. (ie: investing $30-40mil annually) It is likely to be losing money at its current revenue- $100mil. (based on my estimation of 100k annual salary for its analysts for around 885 of them, salary alone will cost around $90mil.)

Source: 2022 annual report

Management has been upfront on the investment made and it is likely to erode their margin further but their ESG data is important to be integrated into their ecosystem so that they could be at least on par or exceed their competitors.

Besides, given the tailwind of ESG funding (refer to above diagram), Morningstar has a real chance to capture the market. However, MSCI seems to have a better chance in succeeding due to their relationship with their customers. It is definitely going to be competitive but an attractive opportunity.

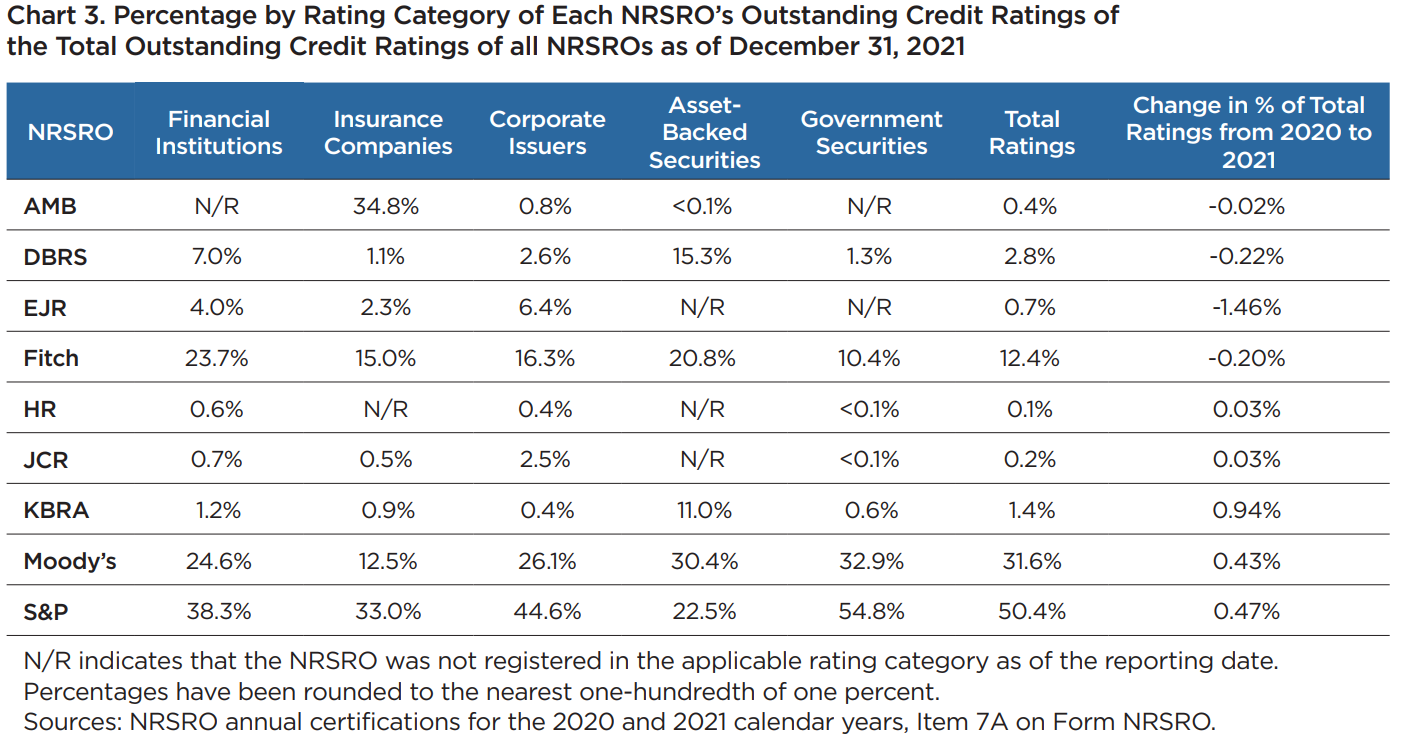

Morningstar DBRS

Morningstar is eager to disrupt the top 3 credit rating agencies but it is not taking much share from them. Big 3 still remains dominant and it is likely to be the case for the foreseeable future. As a result, Morningstar has to compete in the middle market which is less competitive but also less profitable.

Let's understand the credit rating industry. In overall, the Government securities category accounted for 79.0% of the total number of credit ratings reported across all categories with the rest composed of Asset-backed securities (7.7%), financial institutions (6.4%), corporate issuers (5.9%) and insurance companies (1%).

Extracted from office of credit ratings

Based on the above diagram, Morningstar has more market share like ABS/financial institutions but it is only a small pie within the credit rating industries. (assuming $7.7bil at 14% share is only worth $1bil). It is hard to tell if they can win more shares since there is no obvious strength over their competitors.

This could be the sign that it is a bad capital allocation. This is because credit rating largely depends on the firm's ability to reduce cost of capital (not price competition) and if they are not as credible, they are unlikely to create much value. Besides, the data they collected from these middle markets is also less valuable and harder to sell. Lastly, it is also highly regulated and the cost of compliance will be very high making it potentially a poor investment.

Morningstar is proud of their rating capabilities (fund rating) but credit ratings are a different beast altogether as the incumbents have a formidable moat. Game selection is important and Morningstar picks the hardest landscape to compete shows that they are not leveraging their strength.

Section 4: Management, Capital Allocation, and Incentives

Building on Buffett’s Example

As mentioned from the introduction, it is rare that any management follows Buffett playbook as closely as Joe. It does seem that he possesses the qualities of great management - highly ethical, honest and looking after shareholders interest. One good example is that he publicly stated that he will start trimming his stock progressively and explaining his rationale. (He owned close to 70% when the company IPO)

Another example is that there will be no earning calls or forecasts, long term thinking, encouraging shareholder questions,etc (imitating Buffett style). Extracted from IPO document:

“You’ve probably noticed we do some things that aren’t the norm for public companies. We don’t give earnings forecasts or guidance, and we don’t hold conference calls or one-on-one meetings with investors or potential shareholders. Earnings guidance seems unnecessary because the market will simply adjust its company valuation once we report our actual results.

At the same time, earnings guidance has the potential to create questionable incentives for running the business. We don’t want to encourage our management team to simply “make the numbers” and possibly make decisions that don’t help build shareholder value over the long haul.”

Even after he is no longer running the business, the culture was closely followed by his successor. Below is an interview of Kunal, the current CEO:

“That question about role models provided an opportunity to talk about Berkshire Hathaway and its chairman, Warren Buffett, whose approach to investing deeply influenced Mansueto. “Joe certainly has taken some pages from Buffett’s playbook,” Kapoor said. “The tradition of putting the investor at the center, thinking about the long term, not getting too caught up in the swings of the day-to-day market. I have a very deep contrarian streak myself.”

That being said, I have doubts about the new CEO's ability to allocate capital effectively. Upon his takeover, both the ROE and ROCE went downhill to low single digit. Of course, it is easy to justify low returns due to aggressive investment, but it seems to deviate from Morningstar's principle of investing prudently.

The new management has singlehandedly increased its debt from almost zero to $1bil. Coupled with rapid headcount growth (2x their headcounts in 5 years), the management might have issues in servicing increasing interest cost. I project that they will likely cut their headcount in the near term or cut dividend and buyback to solve their near term issues Refer to the capital allocation section for more information.

Capital allocation

Sources: Company Filling

Acquisition has been an important strategy for Morningstar but it used to be small scale acquisitions (improving their database) and focus more on organic growth. Only after the new CEO (Kunal) took over, acquisitions have been huge. I will be going through the 2 latest big acquisitions by Morningstar.

DBRS credit agencies. Morningstar has been eyeing the credit rating market and made an acquisition at the end of 2018 to be the fourth largest credit rating agencies. The company paid $669mil to acquire $169mil of revenue. (mainly fund with debt) Assuming a 20% net profit margin, Morningstar would be paying 20 P/E for this business. Since the acquisitions, it has been growing at around 10% annually.

Assuming it can grow by 10% annually, it could be generating a 10% of ROI which is not great but decent. However, there is a need to bear in mind that it is highly cyclical and depending on the market cycle. When time is bad, they will suffer badly due to high fixed costs in nature.

For example, the current marco environment (high interest rate and low growth) has caused them to suffer double digit declines in revenue. (I have discussed in Section 3 why this could be a bad acquisition so i will not repeat again here)

Leveraged Commentary & Data. LCD is the industry standard for leveraged loan data, news, analysis, and indexes. It is the only provider of real-time coverage of the U.S. and European leveraged loan and high-yield bond markets, from deal inception through the trading life of the debt.

It also provides growing coverage of investment grade bond issuance, distressed debt, corporate bankruptcies, middle market transactions and CLO/fundraising. Over 20 years, LCD has provided data on over 30,000 issuers and 85,000 transactions.

Besides, LCD has more than 500 leveraged loan indexes in the U.S. and Europe tracking performance, index characteristics, and risk measures of over 1,800 loans. (Complementing their indexes business)

It is an important piece for PitchBook to become a comprehensive and centralized solution for the private capital and debt markets, enabling due diligence and deal making workflows. It paid $650mil to acquire $56mil of revenue from S&P Global in 2022. (mainly funded with debt) It is definitely an expensive acquisition - 10x P/S. (Alternatively, this could be a high margin business as it has only 60 employees. Assuming 100k for each staff, it is likely to be a 60% operating margin business)

Although it is justifiable, the return on investment could be bad due to the price they paid. For it to be great, their execution has to be flawless. It is currently integrated into Pitchbook platform and it will take time to see the result. This investment could take years for them to recoup if it failed to realise their intended goal.

I certainly think that the acquisition is unnecessary at this stage since the market is relatively underpenetrated and they could succeed without it. It is a risky investment given that they are highly levered after the acquisition.

Overall, the big acquisition made by Morningstar seems to be rushed and as a result, the company has accumulated a huge amount of debt. (2.5x levered) The good news is that there is no equity issued to acquire these companies as they deemed stocks as an important asset. (Stock counts have reduced by 15% for the past 10 years)

Ownership

The founder/chairman has a big stake in the company at around 39.3%. However, he is actively reducing the stake to reduce concentration risk. The pace remains slow and I don't see it as a bad sign as he is very transparent about it.

He seems to enjoy his semi-retirement life by buying an American professional soccer franchise (Chicago Fire FC), several media companies, real estate properties and other ventures. Another interesting development is that he has pledged to give most of his wealth to a charity run by Warren Buffett.

As for the rest of the top management, they only have 0.6% stake in the company. It is counterintuitive that most of the management does not seem to be interested in owning more of the stocks despite having a positive long term view. (Possibly to diversify concentration risks as they have high exposure in the company)

Incentive

Based on the above table, Its SBC has been higher than its peer. It is attributable to their performance based rewards: ie: high variable remuneration. CEO pay package comprises 8% fixed salary (500k), 69% equity and 23% target annual incentive.

It is good to dissect how they reward their top management. The first one is the target annual incentive. It varies based on the proposal of the remuneration board. Eg, for 2022, it was decided to be around $1.5mil. Annual incentive will be paid based on 2 metrics with revenue consisting of 67% and EBITBA at 33%. (Changed from 50%-50% but will be reverted back as complained by shareholders) The company seems to focus alot of unprofitable growth.

Sources: Company proxy statement

As for equity based compensation, the company has increased its mix to 75% market stock units (MSU) and 25% restricted stock units (RSU). This change should align the director's interest as MSU is vested based on past 3 years total shareholder return (TSR).

Sources: Company proxy statement

However, it doesn’t seem to have a high threshold as a 7% (keep changing) of total shareholder return (TSR) annually is sufficient for them to be entitled for the MSU that made up a majority of their remuneration. In addition, if there is financial outperformance, they may receive an additional number of shares. (it is called the revenue kicker at 100%-150% of shares earned)

Since the founder stepped down as CEO, it is pretty rare to see its executive aligning to shareholders. Ie: buying shares from the open market. (Note: It is worth mentioning that Joe's salary has been fixed at 100k since 2000 as he believes his compensation should be directly aligned with other shareholders. It is something that has been long gone since the Buffett generation.)

“I’m trying to set a good example. I don’t need to take a high salary, which would impede the success of Morningstar.”From an interview with Chicago Magazine.

Section 5: Conclusion

Joe Mansueto built an impressive business with the rise of active management in the 90s. Mutual funds become the new way to invest for investors and Morningstar sitting in between all the action stands to benefit greatly from this tailwind.

However, with the evolution of fund management bias towards passive investment, Morningstar is facing a huge challenge given their reliance on the active fund management industry. For example, as per BCG report, global AUM stands at $100trillion with the split of 25% (passive) and 75% (active). Passive management funds (market shares increase from 10% to 25% in 2021) (ETF) suggests that more investors are leaning towards passive.

Thus, regardless of how strong their fund rating business would be, a shrinking market would not likely to help them in the long run. As a result, the management has been actively diversifying into other businesses that they could build on to be the next growth machine on a sustainable basis.

Pitchbook, the final touch by Joe Mansueto before he stepped down as CEO is likely to be the gem for the company. It has the potential to grow to become the hub for private deal making but it is still at the early stage. As for other newly acquired businesses like sustainalytics or DBRS, it will still need time to see the results but unlikely to do as well as Pitchbook.

Lastly, active management is unlikely to be gone forever but it is likely to remain as the “tool” for the top 10% of the population to access in order to outperform the market. It could still be an attractive business due to the operating leverage and Morningstar is not giving up on it.

Morningstar has certainly evolved themselves over time and they have shown that they are willing to step outside of their comfort zone. With their aggressive investment lately, I believe that their net profit margin will bottom and are ready for a rebound as they realise that it is no longer sustainable in this environment. (Ie: slowing hiring, absence of severance payment for the China market and committed to reduce debt)

The current valuation (with normalised earning) also doesn't seem stretched as well as most of their peers are trading above 30x P/E given the stickiness of their business nature. Despite some poor capital allocation and short term hiccups, the business remains resilient and as long as they are investing in a business that has high ROI, it will still be considered as a high quality business. Any weakness deserve an add.

Disclaimer: I have no position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. However, i might have position in the future and i might be bias. Invest at your own discretion.

Reference

The Quiet Billionaire: Morningstar CEO Joe Mansueto by Chicago

Morningstar CEO Kunal Kapoor Is All In for Investors by Chicago Booth Magazine

Joe Mansueto - Lessons From the Founder of Morningstar by Business breakdown

Morningstar by VIC

The Tide Has Turned: The future of asset management industry by BCG

Interesting extracts from 2023 shareholder meeting: