$MSCI: The plumbers of modern finance

$MSCI: The plumbers of modern finance

Superior track record

Company: MSCI Inc

Ticker: MSCI , listed in US

Industry: Financial, Indices and financial data

Investment thesis

The investment thesis for MSCI is a fairly simple one. It is the belief that passive investment and global investment will continue to gain traction. MSCI should be the major beneficiary given that they are highly exposed in the indices business especially for the global market.

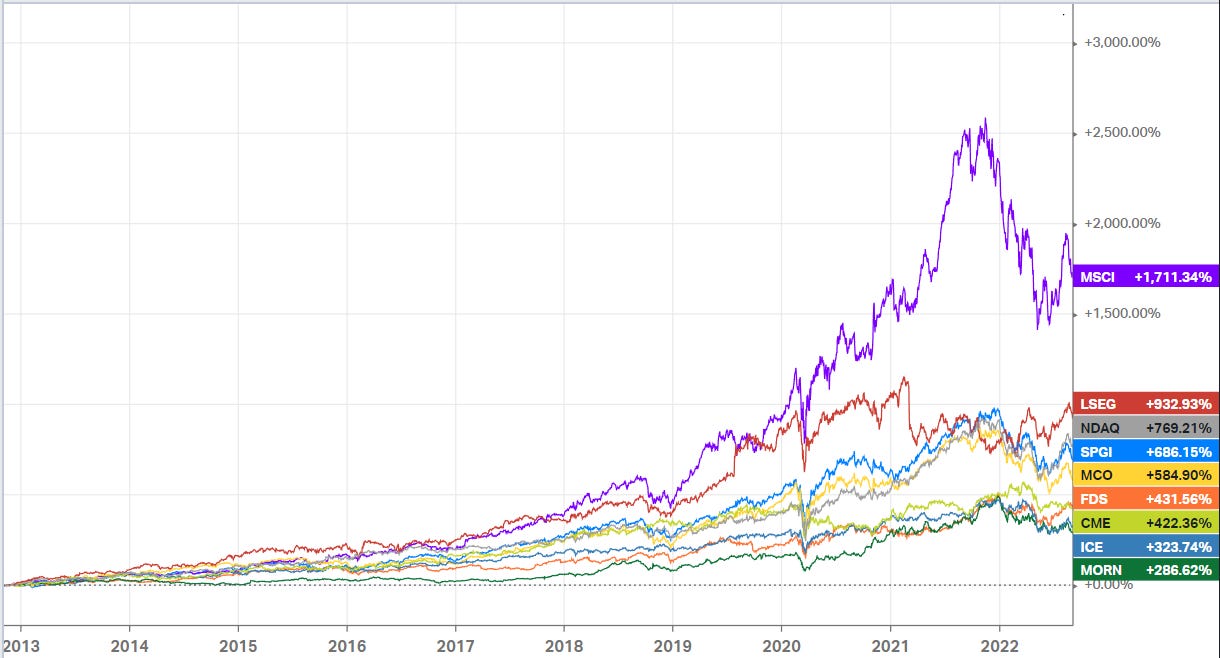

It is a 17x investment since its IPO in 2007 and it has vastly outperformed its peers over the past 10 years period as per Koyfin. Although it is lesser known than S&P 500 indices for the general public, MSCI has slowly gained recognition among the investment community.

This research is about determining the business competitive advantage and how MSCI can continue to outperform in the ever competitive financial market. As well as discovering the future growth driver that will continue to propel the business future growth.

Looking back

The pioneer for international indexes was actually coming for the company called Capital International. They are the first to publish indexes covering the global stock market for non-U.S. markets. In 1986, Morgan Stanley saw the opportunity and then licensed the rights to the indexes from Capital International and branded the indexes as the Morgan Stanley Capital International (MSCI) indexes.

By the 1980s, the MSCI indexes were the primary benchmark indexes outside of the U.S. before being joined by FTSE, Citibank, and Standard & Poor's. After Dow Jones started float weighting its index funds, MSCI followed. In 2004, MSCI acquired Barra, Inc., to form MSCI Barra.

In mid-2007, parent company Morgan Stanley decided to divest MSCI. This was followed by an initial public offering of a minority of stock in November 2007. The divestment was completed in 2009.

Introduction

Fast forward to today, MSCI became the leading provider of investment decision support tools such as indices, risk management,etc to investment institutions worldwide. MSCI currently has 3 major businesses: Indices, analytics and data.

Indices (62%)

This segment earns its revenue from 2 sources. Firstly, It earns its revenue from subscriptions by licensing their data to asset owners such as pension funds, endowments, managers,etc for purposes like benchmarking, asset allocation,etc. On average, a client paid about $130k per year for the subscription.

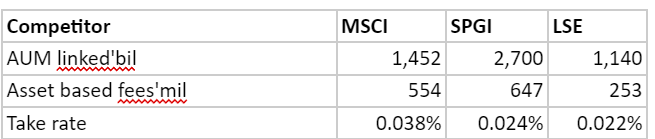

Another source of revenue is based on the assets linked to their indices. Based on my calculation, MSCI usually charges around 3-4bps on the linked assets. Its take rate has been fairly stable over the years. The segment has high recurring revenue (97%) and has minimal churn (4-5%) annually.

The beauty for the indices business is that it is asset light and there is minimal incremental cost for additional sales. The unit economics for the business is very attractive. As a result, the margin for the business has been improving over time.

Analytics (27%)

This segment earns its revenue from selling risk management tools, performance attribution and portfolio management content to their customers on a subscription basis. It is also a highly recurring business.

ESG and climate (8%)

As for this segment, it is the new driver for MSCI future growth due to more awareness on ESG investing. MSCI being the pioneer for the ESG investing concepts are enjoying the fruit of their labour.

Others (4%)

It is the other segment that comprises private assets such as Real estate and Burgiss group (private equity). It is the management's new focus to diversify their footprint into multiple asset classes.

Bull

The plumbers of modern finance

The most obvious example for the plumbers of modern finance are Visa and Mastercard which take a few basis points off every transaction. It is simply one of the best business models. However, in my opinion, the most lucrative basis point charges are for intellectual property. This is where indices players like S&P, MSCI and FTSE Russell come into play.

Building up an index is easy. All they need are some people and computers to compute the indices. The most common form of index calculation method is the market capitalization weighted approach. Bears argue that most funds can do it by themselves.

However, it is not possible for these funds to do well due to the following argument by some bull analysts:

1) Scale - Most funds are unable to produce their own indices as they are simply too small and lack the scale to do it profitably. The cost of building their own indices is also hard to justify due to lack of AUM linked to it. It is also hard for them to monetise their products more efficiently than the incumbent such as collecting asset linked fees.

2) Distribution - Most fund houses lack the distribution channels to distribute their products. When the big 3 indexers basically dominate the distribution channel by working with the biggest asset managers in the world, there is no room for smaller players to compete.

3) Resources - Designing and rebalancing indices in real-time within a regulated environment is often not as easy as it looks, and requires specific data, expertise and insight. It might not be worth it for smaller fund houses to save a few basis points to create their own indices.

Thus, there is a need for independent indexers with great brand names and reputation for providing such services as they could do it more efficiently and transfer the savings to their customers.

MSCI happened to be one of the 3 biggest indexers in the world. This is due to their relentless effort of building up their brands. They understand the power of brands and they could leverage their brands to embed themselves into different asset classes such as bonds, private assets, alternative investment,etc. Imagine PnG or Unilever without the burden of the capex but still command strong pricing power. This is how powerful MSCI could become.

MSCI strength lies on how they have positioned themself. The key is to be globalised. They have branded themselves as the global indexer by being as neutral as possible with each country's regulators. The most popular indices for MSCI are MSCI world index, MSCI ACWI index, MSCI Emerging Markets,etc.

This was the argument by the CEO and below is the transcript by the CEO with Barron interview:

“When I took over MSCI, the SPDR ETF was already in place and MSCI was working on the first ETF for international markets. We could blanket the world with futures and options for equity indices. Later, I realised what we did in equity, we could do in fixed income, in global private asset classes, in real estate. We were international. A lot of the other providers were mostly domestic, catering to domestic investing”

As a result, their indices are the best for investors who want to obtain global diversification. Their competitors are seen as more pro western countries and might be perceived as less diversified as a result. This is a good move by MSCI as they could avoid going head to head with S&P 500 who is dominant in the local market and gaining share of mind for the global market.

Bull also argues that brands will help to drive their flywheel as great brand recognition will enhance credibility of their client products. This will in turn attract more funds to offer products that are linked to their indices. It will create positive feedback loops to further strengthen their brands.

Another advantage will be the scale effects that I mentioned above. MSCI Inc calculates more than 274,000 benchmarks on a daily basis and there are about $1.4 trillions of AUM linked to their indices. It means that they can make use of their operating leverage to offer a cheaper alternative for fund houses that want to produce their own indices. Recently, MSCI offered a new platform that allowed fund houses to offer their own custom indices with MSCI as the data provider.

Besides, due to their scale, they could collect more proprietary data and release products that are more complex and tailor made. One of the bull argues that real money is to be made from newer and more complex indices that are required to power the rise of alternative investing ideas.

These indices can charge more in basis point fees – anything from 5 to 50 basis points depending on the complexity. MSCI could mix and match the indices using their proprietary information. A good example of this will be factor models + equity indexes = Factor indexes, ESG ratings + fixed income indexes = ESG FI indexes, etc.

Lastly, MSCI products are also very sticky. It is evidenced by the company's exceptional retention ratio. It is usually around 95%-96% suggesting that clients are either satisfied with services or there are no better alternatives.

Once the asset owner has selected the benchmark, they rarely change it due to liquidity, and tax considerations such as capital gains. As the funds continue to grow unless it doesn't perform well or investors pull out funds from the AUM such as during the financial crisis, there is no reason for their clients to switch due to they are stuck within the MSCI ecosystem.

To be more specific on the MSCI ecosystem, it is their ability to cross sell their products. It is the classic land and expand approach. Once the client is in the MSCI ecosystem, MSCI will cross sell other types of products such as risk management back testing, other asset classes data,etc. As a result, they will be integrated into the MSCI services.

Based on the 2021 investor day presentation, the longer the clients stayed with MSCI, the more products they are buying. For example, all product lines increased from 55 to 60% and the subscriptions per client also increased over the years from 60k to 99k as they stayed longer with MSCI.

Competition

The most notable competitors for MSCI are SPGI and FTSE Russell. These 3 providers alone owned close to 80% of the indices market share. They are taking the lead in the domestic market. The US certainly is a very big market but it is also highly competitive.

Performance

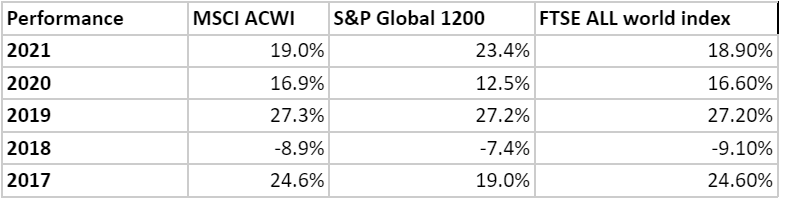

Thus, MSCI has positioned themselves as the global indices and it gives MSCI better pricing power due to lesser competition for their international market. It has the highest take rate among its competitors. However, their competitors aren't going to back down without a fight by introducing similar products like S&P Global 1200 and FTSE All world index.

Based on the factsheet of each global index funds performance, their performance is fairly similar. Although their competitors are going after the similar pie, MSCI is still the go to for international investment due to the effects of share of minds.

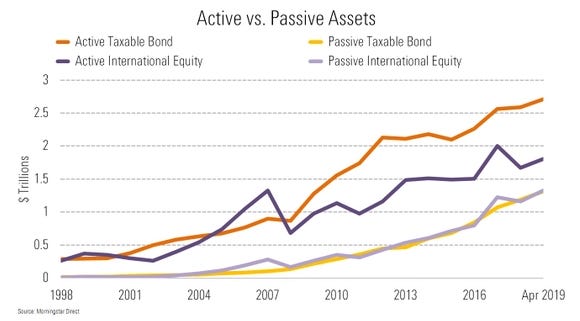

As for competition with active management, there are certain areas of the market where it is still being dominated by the active investment funds. Low information transparency and trading difficulty are some of those areas that active investment has the upper hand. International market, bond fund,etc is a good example of low transparency and harder to trade due to regulation constraints.

For example, as per morningstar research, 95% of municipal bonds are in active strategies. Investors still prefer active managers in international stocks and taxable bond funds.

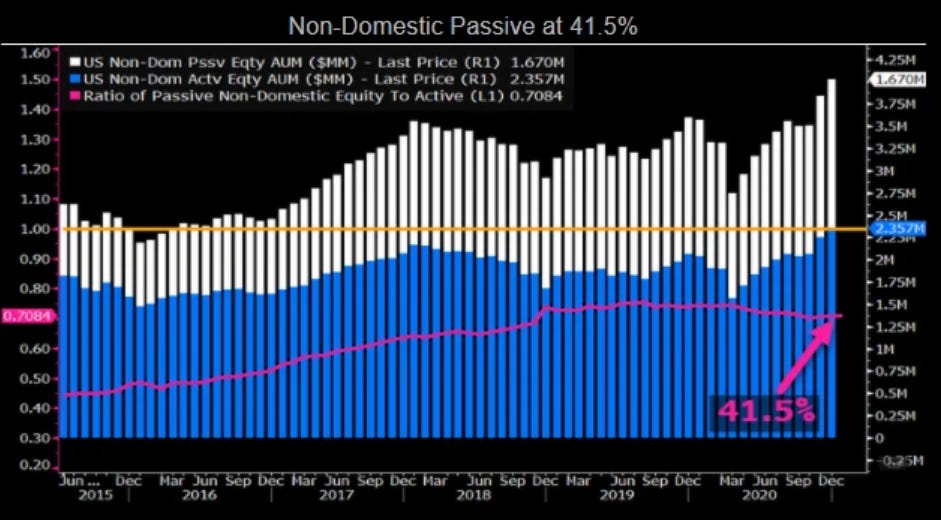

Another evidence is based on Bloomberg analysis. International and global equity funds were the only area where passive management lost market share over the past two years due to poorer performance as compared to US equities.

That being said, it is likely that the international market will continue to gain interest as more reform for international markets to attract fund flows into their countries. On top of that, there is an increasing interest for clients to seek for more diversification across the globe instead of concentrating on US companies.

Bear

Self indexing

One of the main concerns for the index provider is the rise of self-index by large fund houses. In the ever competitive environment for asset management, these fund houses are consistently under pressure to lower the expense ratio in order to attract more AUM.

As per Morningstar research, as expense ratios are shrinking over the years, fund houses are finding ways to cut costs. Self indexing might be a good way to reduce expense ratio provided they have the scale and distribution channel. For example, several large asset managers have chosen to self-index a portion of their assets (State street, Goldman sach).

However, there is an issue of conflict of interest. A great example would be the Libor benchmark scandal where bankers colluded to manipulate the interest rate. Thus, an independent player is more likely to resolve this type of problem. So far, this trend has been limited, with no noticeable impact on MSCI or the other index providers.

As for other clients, they are moving for cheaper alternatives to minimise their cost. For example, Vanguard, the world’s second-largest fund manager, in 2012 discontinued using MSCI and moved to the services of the Centre for Research in Security Prices and FTSE Russell. More recently, State Street Global Advisors swapped out MSCI for German index firm Solactive for four of its exchange traded funds (ETFs), reducing their expense ratios significantly.

Another worrying trend for MSCI is that their clients like Blackrock, Vanguard, etc are gaining more bargaining power over them and affecting their pricing power. For example, Blackrock being one of the largest fund houses managing over $9.5 trillions of assets contributes close to 12% of MSCI revenue.

That being said, the revenue lost could be compensated by the growth of AUM that linked to their indexes. This is actually better for the existing players as this will increase the barrier of entries for new entrants who will need higher AUM to breakeven. The power will accrue to the players with the scale.

Management

HENRY A. FERNANDEZ was a managing director at morgan stanley. He is one of the few key executives that leads the MSCI transition to becoming a fully independent public company from morgan stanley. As per an interview with Barrons, he agreed to lead the company because he saw what MSCI could become:

There is also no doubt that he and his team are creating so much value for their shareholders. This is in part due to the top management's superior capital allocation skills. It ties to top management ability in understanding business drivers. They have set a high bar for their investment criteria they called as triple crown:

1. High return for projects invested (ROI)

2. Quick payback <3 years

3. Prefer investment with greater impact on valuation

He is also a big fan of the outsider, the book discussing great capital allocators suggesting that he is highly conscious on how to create value for his shareholders. In of the interview with Barron, when asked how he spent his spare time, the CEO mentioned the following:

“I’m rereading The Outsiders, about CEOs who have created an enormous amount of shareholder value. I’m a business nerd” by Henry.

On incentive, the management is highly aligned with shareholders as over 92% of their compensation is variable and tied to their long term performance. Although it is not a family owned business, the management collectively owned a meaningful stake of 3% in the company (worth about $1bil). Coupled with high retention of top management (most of the executives stayed more than 10 years), the company is in good hands.

Financial analysis

As for the company growth, sales growth has been consistent at 13% CAGR but operating income has increased by more at 16.5% CAGR for the past 5 years. Their net margin has reached its high at around 36%. This can be attributable to the effect of operating leverage. I believe that they should be able to continue to improve their margin as they continue to grow.

The common playbook for highly predictable cash flow companies is to make use of debt for reinvestment or return to shareholder purposes. There is also no exception for MSCI. Although they are in net debt of $2.9bil, however, their predictable FCF ($905mil annually) should be able to pay off their debts fairly easily. (Most debt matures after 2029) One interesting observation is that their equity is negative due to constant share buyback.

On capital allocation, MSCI certainly benefited from their incredible capital light business model. As a result, the management plays an important role in allocating capital. The company has a great track record of returning their capital at the right time by repurchasing its share during its share price weakness. Share count has been reduced by about 2% annually which is fairly aggressive.

MSCI also has been careful with their acquisition and recently made an acquisition on RCA, a real estate data company to strengthen their private asset segment. RCA has recorded over $40 trillion of commercial property transactions linked to over 200,000 investor and lender profiles; it might be a great addition to the company portfolio. As for the price, It is an all cash deal ($1bil) to prevent dilution for its shareholders. Although there is no mention of the multiple paid, it is estimated to be around 30x EBITDA at the point of acquisition as per annual report disclosure.

The rationale is simple. MSCI has always been a data processing factory but now they are rapidly becoming a data building machine. By acquiring more data providers, they could build up a database that is proprietary to them.

With their expanding database, they could create a platform for their client to access their code and allow their clients developers to customise their offerings and scale various use cases.

Opportunities

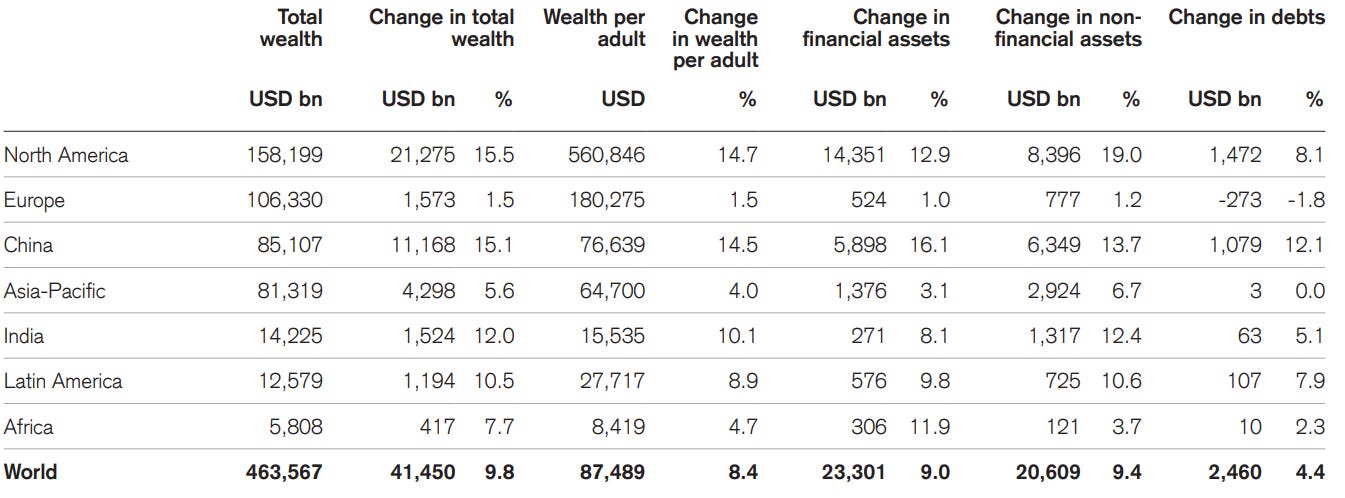

The industry is certainly experiencing tailwinds. Firstly, it is the general wealth increase for individuals. According to credit suisse, global wealth in 2021 is estimated to be around 463.6 trillion and expected to increase by 7% over the next 5 years. With growing wealth, there will be more funds flowing into investment vehicles that generate higher yield.

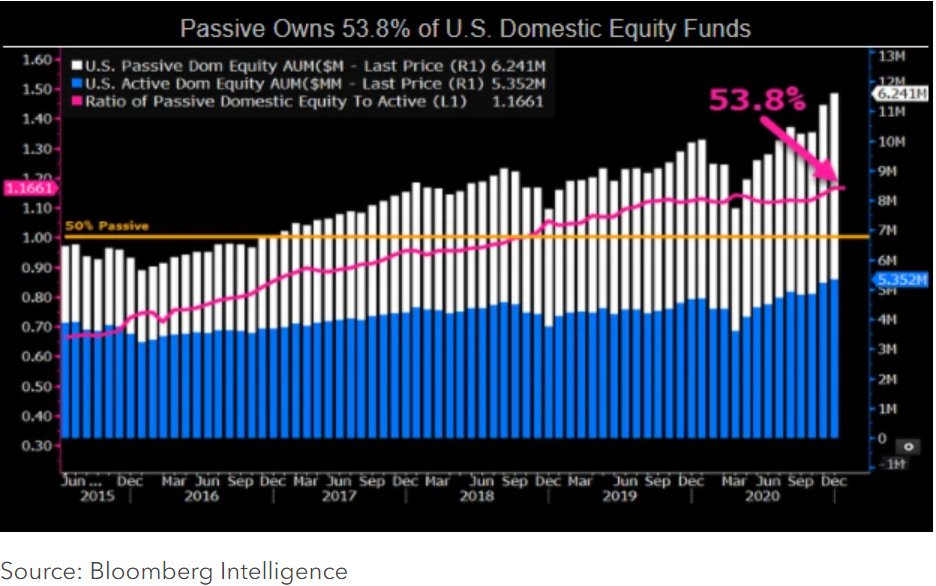

Besides, according to Bloomberg, more funds are flowing into passive investment. By looking at the chart below, passive investment shares have been increasing over the years and it has reached 53.8%. It is forecasted to increase further and this is an inevitable trend that will continue to disrupt the active investment landscape.

This trend is aligned with MSCI growth over the years. There are more assets linked to passive indices like S&P, MSCI,etc. For example, the growth of AUM linked to MSCI products has increased steadily at a 13% CAGR (from $192bil to $1.4trillion) since MSCI went listed.

Lastly, sustainable investing like ESG/Climate indices and rating will be the major drivers for MSCI future growth. The concept of ESG has been gaining a lot of traction lately with the MSCI slogan to help global investors to build portfolios for a better world. As per Bloomberg estimates, MSCI is estimated to own almost 60% market share in this segment.

MSCI is still at a very early stage of ESG rating. Bloomberg Intelligence projected that more than one-third of all globally managed assets, amounting to more than $50 trillion, could carry explicit ESG labels by 2025. Besides, as per MSCI investor presentation, the penetration rate for ESG is still relatively low at around 30%. This segment alone is worth more than 4bil and is growing very fast.

MSCI wants to be the key player in the ESG rating business. It will be a very lucrative business as it is fairly similar to credit rating agencies but without regulation. UBS Group AG, found MSCI earns almost 40¢ out of every dollar the investment industry spends on such data, far more than any rival.

However, there is an interesting article from Bloomberg that mentioned that the ESG rating by MSCI is purely based on profitability and greenwashing by big corporations. Their rating methodologies are also very subjective and thus resulted in inconsistencies across different raters.

Lastly, as per another bear, ESG investing does not benefit the investors but instead benefiting the corporations who are advocating the importance of ESG investing. For example, big fund houses could charge higher fees, ESG consultants earning high fees in ESG consultation, more ESG disclosure benefits accounting and audit firms,etc. In the end, it is just another tool for companies to exploit their clients.

Conclusion

MSCI has set a high bar for themselves since their IPO. It certainly ticks the boxes of high quality business such as great brand name, sticky ecosystem, strong operating leverage, long run way, etc. Betting in MSCI is equivalent to betting that passive and sustainable investing will thrive in the future. It is certainly not a bad bet as the future is moving that way.

Besides, MSCI is well positioned to benefit from the key secular themes in asset management: shift from active to passive investment, ESG/Climate investment, the growth of Private Assets,etc.

The irony being that as a company, it has far outperformed their own products. It would be better off to invest in MSCI than products index to their indices. To justify current valuation, the company needs to grow 11% for the next 15 years. It is certainly an expensive stock that should be revisited when the valuation is more reasonable.

Disclaimer: I have no position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion. If you like my post, please also consider to follow me on twitter as well.

Resources

MSCI Deep Dive by Enlightened Capital

Stocks in my portfolio: Why I invested in MSCI plus how to invest in global equities by Adventurous investor Newsletter

The Financial Index Industry by Committee for Economic Development

MSCI, the largest ESG rating company, doesn’t even try to measure the impact of a corporation on the world. It’s all about whether the world might mess with the bottom line by Bloomberg

Why ESG is fatally flawed by Chris Leithner

Hi, I usually don't time the market but my view is that the market has priced in alot of future growth in its current valuation and it is richly valued. However, there is no doubt that the company is high quality based on my personal quality assessment criteria. Please do your own due diligence when buying any stocks I mentioned.

Is it now a buy? I guess so