Nick Sleep Wisdom - Part 2

Nick Sleep Wisdom - Part 2

The Nomad Capital

In the realm of revered investors, Nick Sleep stands out as an exemplar of humility and low-profile professionalism. The founder of Nomad Capital, he commenced his journey on September 10, 2001. Sleep's remarkable track record, a 20% (before fees) compounded annual return over 13 years until the fund's closure for personal reasons, solidifies his place as a legendary figure in the world of investing.

The series will be separated into a few parts:

Part 1: Nick Sleep investment philosophy and lessons (2001-2005)

Part 2: Nick Sleep investment philosophy and lessons (2006-2010)

Part 3: Nick Sleep investment philosophy and lessons (2011-2013)

Part 4: Nick Sleep mental models

Today's post will continue to delves into Nick Sleep's investment philosophy, lessons and stock pitches, offering insights into what we can learn from this legend to become better investors.

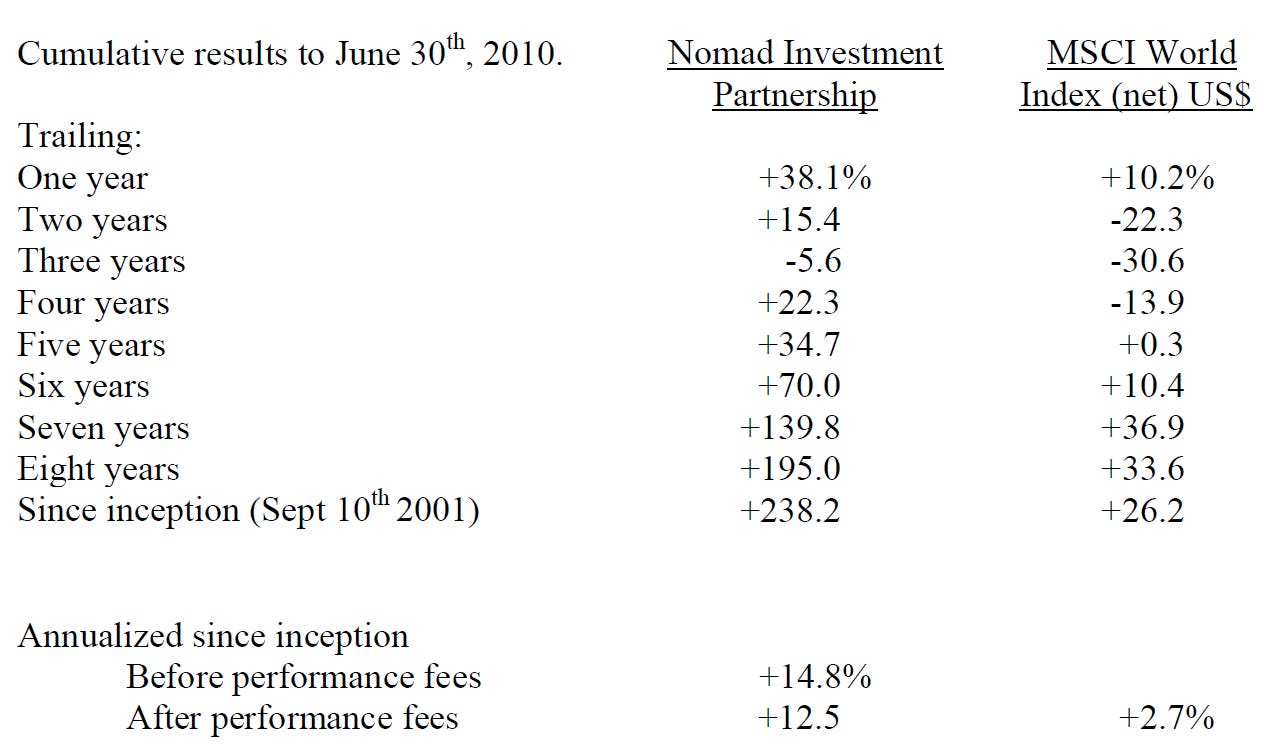

2006 is the year Nick Sleep and Zak leave their original firm - Marathon and run their own fund. It is also the first time the fund faces challenges from the 2008 financial crisis. However, they manage to pull through and not only survive but thrive as a result of their unmatchable insights on long term investing. (If you miss the Part 1, you may click on the link here)

Delving into the second four-year performance of his fund, notably in 2008—a year notorious for testing Nomad Capital. Amidst a 45% downturn, the fund's resilience significantly outshone the broader index on an annualized scale. The letters from this period stand out as profound guides, illuminating invaluable lessons on navigating stock market crises.

On Portfolio construction:

“It is commonplace for overall portfolio construction to be as a result of stock weightings built up from one to two to three percent of a portfolio and so on up to a target holding. This means that weightings are anchored at a small number with only outliers reaching double digits. There is another way to construct a portfolio, which is to invert and start at a hundred percent weighting and work down! If fund managers did this, I am sure they would end up with completely different portfolios.” Annual letter 2006

On dealing with mistakes

“We (strapping on the protective armour of the first-person plural) have made lots of mistakes. (I will be less cowardly) I have made lots of mistakes. Sometimes we made the mistakes ourselves. Sometimes we learnt from others. Sometimes they were direct investment mistakes. Sometimes they were part of growing up (look out for those private mistakes, they are full of investment lessons). But there they are. Warts and all. This is how life is. We do not justify them, but we do not condemn them either. Indeed, they are best not judged. Our model is to learn from our mistakes and what we learn we hope to give to you, in better performance results (in exchange for a performance fee!).”Annual letter 2007

On how to avoid making mistakes

“One trick to help see the world more clearly is to invert situations. A newspaper headline claiming that one third of the population wants something, also tells you that two-thirds don’t! In our opinion, the best book to hone the skills of inverting was written by Terry Arthur in 1975 and is entitled “95% is Crap – A plain man’s guide to British politics”. Terry is one of the most modest and thoughtful people Zak and I have had the pleasure of meeting, and he was one of the first investors in Nomad.” Annual letter 2007

On chasing yield

“Output maximisation looks efficient at least in the short term, but that is not the same as being long term optimal. The flaw to putting money to work immediately, for instance, is to presume that all relevant opportunity sets are available immediately. By accepting, say, a promoter’s promise of eight percent returns (six hundred basis points better than money on deposit), the investor denies himself the right to future opportunity sets which may be far better, like public equity circa 2008 and 2009, we would argue.

This is an easy concept to grasp when applied in hindsight, but much harder to see prospectively. A plan sponsor who argued that contrary to the income statement, his cash was not earning two percent but ten percent (a blend of two percent on deposit now and twelve percent from an as yet undefined opportunity set sometime in the future) risks being perceived by his peers as away with the fairies – the lawyers and auditors would not endorse his view - but he was right.

That is why, in the hands of Warren Buffett for example, one could rationally argue that cash is worth more than cash. That is not an argument for hoarding cash, as many do today. For the cash to be worth more than cash it must be invested intelligently. It is, however, an argument for a cash buffer, just in case, a little slack in the system.” Annual letter 2008

On selling too early

“1. Misanalysis, or using the wrong mental model: Investors are used to firms which have one good idea, such as a new product, but then struggle to replicate success and end up diluting returns (Zak and I call this the Barbie problem, as Mattel has struggled to replicate the economics of its famous doll). Taking this model and applying it to Wal-Mart would miss the company’s source of success entirely as the strategy of price givebacks did not change from year to year; culture plays a part in the continuity of a successful price giveback strategy and factors such as culture, because they are hard to quantify, often go undervalued by investors; investors presume regression to the mean starts at the time of their analysis or, as CFA students may recognize, in year three or five of a DCF analysis! Investors use valuation heuristics rather than assess the real value of the business.

2. Structural or behavioral: Active fund managers have to look active. One way to do this is to sell Wal-Mart, which appeared expensive (but actually wasn’t), to buy something that appeared cheaper (but err, also wasn’t); investors are not long-term and did not look further than the next few years or, more recently, few quarters. Evidence for this can be gleaned from the average holding periods for shares which stands at just a few months; fund managers wish to keep their jobs and espousing a ten-year view on a firm risks being a hostage to fortune; marketing folks require new stories to tell and new stocks in the portfolio provide new stories; fund managers sell their winners in order to appear diversified in the eyes of their clients.

3. Odds or incorrectly weighing the bet: In the words of my first boss, investors tend not to believe in “longevity of compound”. Conventional thinking has it that good things do not last, and indeed, on average that’s right! Empirical Research Partners, an investment research boutique, discovered that the chance of a growth stock keeping its status as a growth stock for five years is one in five, and for ten years just one in ten. On average, companies fail.” Annual letter 2009

On reducing reinvestment risks

“There are, broadly, two ways to behave as an investor. First, buy something cheap in anticipation of a rise in price, sell at a profit, and repeat. Almost everybody does this to some extent. And for some fund managers it requires, depending upon the number of shares in a portfolio and the time they are held, perhaps many hundred decisions a year.

Alternatively, the second way to invest is to buy shares in a great business at a reasonable price and let the business grow. This appears to require just one decision (to buy the shares) but, in reality, it requires daily decisions not to sell the shares as well! Almost no one does this, in part because it requires patience - and the locker room set does not do patience - but also because inactivity is the enemy of high fees.” Annual letter 2009

On doing the little thing right

“It is tempting when analysing such situations to look for the big thing the firm does right. In effect, one is looking for the smoking gun that explains the firm’s success. A smoking gun may be a vivid image, but the world does not always work like that. I should have known better when I asked what big idea had led to the firm’s success: “No, no, Nick, there is no secret sauce here”, one senior executive explained, “we don’t do one thing brilliantly, we do many, many things slightly better than others”.

I have heard this line frequently over the last twenty or so years, and I have always dismissed it as a fig leaf covering the lack of any real corporate advantage. And I think that all this time I may have been wrong.” Interim letter 2010

Stocks invested/discussed:

1)Air Asia

2)Games Workshop

3)MBIA (mistakes due to dilution risk)

4)Michael Page

5)Welsh insurance company

6)Asos

7)Amazon

Conclusion

It might be the best period for his fund to buy some of the highest quality companies like Amazon and Games Workshop at a super attractive price. Investing is a tough game (imagine dropping by 45%), so discipline (sticking to the high quality companies, pay a fair price and be patience) is going to be the key to long term compounding.

While the wording may seem lengthy, reading it is never dull. I'm quoting him directly to preserve his intended meaning. No summary is good enough to replace his original letters. You may read the complete letters from the archive here in his IGY foundation website. He is kind enough to share his wisdom and I think more investors need to know about it.

Disclosure: I am not affiliated to any of the authors or writers and didn’t receive any monetary compensation. It is merely for education purpose and my passion for investing. I might own stocks pitched by them and please do your own due diligence. Cheers!!!