$ODFL : The impeccable wall

$ODFL : The impeccable wall

Best in class LTL operator

Company: Old Dominion Freight Line

Ticker: ODFL , listed in US

Industry: Logistic

Old Dominion Freight Lines (ODFL) caught the attention of a lot of investors on twitter due to their outsize return. It is a 200x baggers stock from the day it IPO in 1991. So, how does a company operating in a tough industry manage to outperform the market with such a wide margin? I will be trying to uncover the underlying reasons behind it.

History of the trucking industry

The trucking industry has undergone several changes of regulation throughout the years. The biggest impact to the industry would be the introduction of the Motor Carrier Act of 1980.

The act has helped in liberalizing the rules of ICC regulation, such as how truckers enter new lanes and set their rates, which yielded more benefits and new competition.

Ever since the new law, a lot of new firms entered the market, primarily non-union low-cost carriers. As a result, consumers reaped the benefits of a more efficient, low-cost service.

Old Dominion Freight Line (ODFL), being one of the biggest beneficiaries of the deregulation, has taken advantage of it by expanding its operations aggressively and providing great service. They were able to make a name for themselves in the LTL industry.

Introduction

ODFL is one of the largest North American less-than-truckload (“LTL”) motor carriers. They provide regional, inter-regional and national LTL services (97% of revenue) through a single integrated, union-free organization.

In addition to its core LTL services, the Company offers a range of value-added services including container drayage, truckload brokerage and supply chain consulting. (3% of revenue)

Industry overview

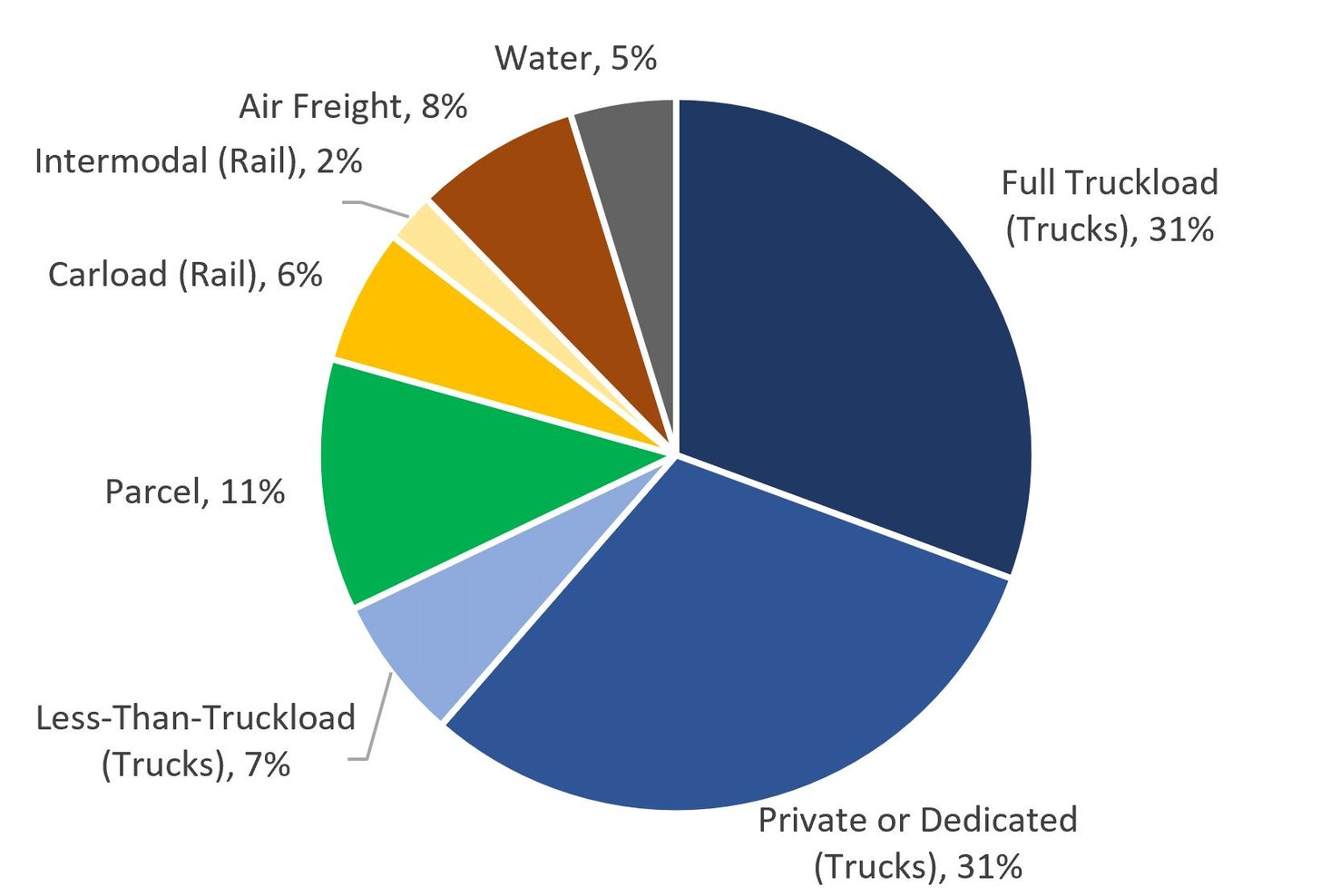

Let's have an overview on the broader industry. As per Council of Supply Chain Management Professionals (CSCMP), freight transportation in the U.S. is worth $1T/year spend industry. Below is a breakdown of the spending by categories:

Trucking broadly is the backbone of the U.S. domestic supply chain, and accounts for ~80% of U.S. transportation spend. It makes sense as most of the deliveries are usually performed on land.

The LTL industry is generally cyclical and it depends on the industrial and retail activities. For the past few quarters, the LTL companies had record breaking quarters mainly due to tight capacity(high spot freight rates) and fuel surcharges.

Besides, the market has also lost two huge LTL players—New England Motor Freight in 2020 and Central Freight Lines late last year—which has further tightened capacity.

As ODFL is a pure LTL player, it is important to determine the LTL industry total addressable market (TAM). As per CSCMP, the market size for LTL is relatively small but has increased steadily from $19.4bil (2002) to $39bil (2020). LTL is a niche (7%) in the trucking industry and has been growing consistently at around 4% CAGR annually.

Business model

It is important to understand how the trucking industry works. In general, there are 2 types of business models for the trucking business (FTL VS LTL). Typically, a trailer has a capacity to fit 24-26 pallets per shipment and the freight weight is about 1,000-2,000 pound pallets. Although they are operating within the same industry, their unit economics differ materially.

1) Full Truckload (FTL) - It is a point-to-point, high variable cost/low fixed cost business. FTL is ideal for companies that have bulk shipments coming from one location and going to one location within a short timeframe. The benefit of FTL is that they are flexible and will be able to adjust their cost and capacity accordingly.

However, it is fragmented with 90% of industry capacity operating 6 or fewer trucks. As a result, the barriers of entry are low. They are usually price takers due to low switching costs (based on market spot rate). Bigger shippers have more pricing power as they have the capacity and they usually sign a long term contract with their customers to negotiate better rates.

2) Less than truckload (LTL) - LTL is a network, hub-and-spoke business model, with material concentration among the largest companies. LTL is ideal for smaller companies that have small capacity to deliver their goods with no tight deadline.

To further understand the model, we need to study how it operates.

LTL carriers (1) will pick up shipments in an area and bring them to a local terminal to be consolidated based on where they are going. Then, shipments are organized and loaded onto another trailer to be long-hauled (2) (usually by truck or rail) to the local terminal of their destination city.

Once the cargo has arrived in the destination city, shipments are again unloaded at the terminal, organized, and loaded onto local trucks for the final leg of their journey. (3)

By looking at the above illustration, we can clearly see that LTL carriers need to incur significantly higher capex as they need to consolidate freights through service centers before their final delivery.

As a result, the barriers of entry are high and they are usually price makers and have a higher bargaining power due to low switching costs.

Metrics

The business model for LTL is certainly more complex than full truckload. However, the metrics should not differ much in this context. This is because essentially, the trucking business is about getting more shipments from Point A to Point B as efficiently and accurately as possible. I believe the below metrics are important to measure the company long term performance:

Key metric #1: Total volume - Volume is measured in tons and in shipments. It is to measure the company capacity. The company has been increasing its volume and shipments steadily (4.4%) over the past 5 years by increasing fleets and service centers (hubs).

By increasing the company capacity, they are able to leverage their network density to reduce cost. While volume increases, operating cost/revenue reduced over the years. (economy of scale)

Key metric #2: Yield management/price. It can be measured by revenue per shipment, hundred weight or intercity mile. It is to measure ODFL pricing power. The company can increase their capacity all they want but if there is a low take rate for its new capacity, there is no point to increase the capacity.

The company has been able to consistently increase their revenue per mile, per shipment and per weight. It is growing at around 7% CAGR for the past 5 years. This implies that the company has been optimizing their network and maximizing their yield so that they can achieve sustainable above average margin.

Bull

Capacity

Yield and maximizing capacity are the key objectives of an LTL carrier. Carriers will prioritize freight that fits their network and improves efficiency so they can provide the best pricing and service for shippers, delivering predictability and employing tender strategies that effectively serve the carrier’s network.

ODFL has been focusing on network optimization by accepting the right freight in the right lanes at the right time. For example, 70% of the ODFL business is contract business with large national accounts and they negotiate on the basis of the profitability of that account.

By planning carefully on their network density, ODFL has essentially located their service centers at the best location which they have the best reach to its community than their competitors. Besides, with their expanding infrastructure, it also allows them to provide faster delivery. Ie:next-day service through each of their regions covering the United states. (approximately 70% of freight)

As more volume is brought in-house, purchased transportation (more expensive) goes down, and operating margins go up. The effect of reducing outsourcing is more than linear because of the advantages gained in efficiencies and accuracy of shipments. Higher margins will go to carriers that best manage their capacity.

Efficiency

When ODFL builds up their capacity, there is a need to manage the efficiency for their service centers. This is because their business model involves long transit time due to extra steps like loading, unloading and handling.

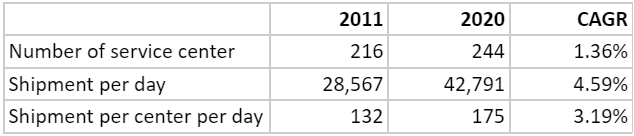

ODFL has been the best in class in terms of managing efficiencies in the LTL industry. By looking at the table below, the company efficiency has improved significantly over the years. They are able to deliver more per service center.

It is attributable to 2 of their strategies. Firstly, ODFL manages service center efficiency by using the “door pressure report”. It is used to examine how often the loading-bay doors are used daily and how much freight is being pushed through a service center.

ODFL understands that too much activity and door pressure, measured by higher numbers per door, can gum up the works. Throwing manpower at it doesn’t help, because then workers and forklifts bump into each other. Thus, door pressure became the main metric they use to assess need for expansion.

“You have to have a fluid dock operation,” said Bates, comparing too-busy service centers to a Black Friday at an overwhelmed Walmart. “You start pushing more than you can handle, and you start losing your efficiency.” Those inefficiencies can mean line-haul drivers stuck at docks and delayed deliveries from the centers to the receivers.

Of course, it could be duplicated by their competitors easily. However, if coupled with the company's strategic expansion on their service centers, it became harder to duplicate.

Obtaining land to build a new service center is not easy. It is due to the strict zoning requirements (take years to obtain a permit) and “not in my backyard” phenomenon (NIMBY).

It is also getting harder to secure a prime location to build new service centers especially in highly populated areas like New York, California, Chicago,etc. For example, ODFL worked for years to get the permits to build a new Chicago facility.

All these differentiation add up and give ODFL an edge over their competitors. In short, they can fulfill more shipments due to increased capacity through their hub and lower the cost of delivery (strategic location + efficient process = more deliveries).

People

It is well known that the trucking industry has high turnover of drivers due to long working hours (typically night shift) and low wages. Based on the American Trucking Association in 2021, the drivers turnover is approaching 89% annually. As for LTL, the turnover is much lower (average around 11%) as most of its drivers make shorter runs and work life balance.

Old Dominion is far from immune from those challenges, but has found success through its competitive wages and in-house training center. Their drivers' pay ranges from $60k-$100k annually as compared to the average annual wage for heavy and tractor-trailer truck drivers to be $44,500 based on Bureau of Labor Statistics. As a result, their annual staff turnover remains lower at around 9%.

Another reason for their better retention might be also attributable to their capacity and shipment flow. Most drivers are in it for the money and they are looking for the highest paid job. As a result, the company with more capacity and workload will attract more truckers (more hours to work = higher pay), vice versa.

Another advantage for ODFL is that they are among the few non-unionized players in the LTL market. This is an important factor as 80% of their variable costs are being paid to their drivers.

Historically, unionized players in the LTL market were plagued by pension costs. These companies continue to suffer from consistent low profitability and high debt. As a result, the market share for unionized players decreased from 45% to 23.8% and the non-union market share increased from 55% to 76.2% in 2021.

For example, Yellow, ArcBest and TFI International (acquire UPS Freight for $800mil), are the largest unionized LTL carriers and have higher employee costs. Yellow and ArcBest's 2021 salaries, wages and benefits as a percentage of revenue averaged 52% vs. 47% for non-union carriers Saia, Old Dominion and XPO.

As a result, the company has higher driver retention. This is important as more experienced drivers improve their level of services and further reinforce the company lead in quality services.

Services

Another competitive advantage for the company would be their level of services. ODFL has been obsessed with their service quality. ODFL has some of the best performance in metrics like cargo claims as % of Revenue and on time delivery. The cargo claim has dropped from 1.6% to a mere 0.1%. It is 5x better than the industry average of 0.5%. The company also is able to deliver 99% on time and has been one of the best in the industry.

To quote Warren Buffett, “the best way to hedge against inflation is to provide the best service or products”. ODFL learnt their lesson well during the 2007-2008 financial crisis. The company refused to reduce prices by lowering their quality of services and caused the company to lose 20% of sales during that period.

“However, customers noticed some non-price factors were missing, Gantt said — factors such as on-time delivery, quality of customer service, care of the shipment.” As a result, most of the customers return to ODFL the year after.

Another important trend would be the big push towards big box retail receiving distribution centers, with on-time deliveries and things like Walmart’s on-time in full (OTIF), and other retailers using a required arrival date (RAD) or an MABD (must arrive by date). If the vendor is unable to deliver on time, there will be a charge back by all these big box retailers.

“A lot of times we are seeing that in the 3%-to-3.5% range. If a vendor has a $100,000 invoice for a shipment it is moving, and it is late, 3% of that is taken right off of the invoice and not paid back to the vendor. Said Dave Bates, Senior Vice president of ODFL”.

As a result, the shippers are willing to pay for better services to reduce any unnecessary cost. ODFL being the best will be able to charge a premium price and continue to reinvest for better quality service to drive their flywheel.

To make a comparison between their competitors, ODFL has been able to earn the highest revenue per shipment.

Bear

There is no doubt that ODFL operates in a tough industry. Some bear analysts have been questioning what it is that ODFL does that another trucker can’t do? There are still lots of competitors and they see no moat for the company. Below is an extract from one of the analyst from Morningstar:

In our view, even the best operators (like Old Dominion) struggle to carve out a sustainable competitive edge via the key economic moat sources: cost advantage, intangible assets, switching costs, and network effect.

"At first glance, it might appear that the high-fixed-cost nature of LTL operations should allow for enduring scale-based cost advantages, or perhaps benefits from superior internal processes that optimize line-haul and pickup and delivery efficiency. However, routines capable of maximizing productivity can be replicated by well-capitalized competitors over time, and scale economies have largely proved insufficient across the industry. The near bankruptcy of industry behemoth YRC Worldwide following the 2009 freight recession stands as a prime example."

Regulation

Another risk for the LTL operators would be the change in regulation. Any changes like restriction on driver hours, increasing drug or alcohol testing frequency, etc will cause the industry to experience a drop in productivity.

For example, under the Federal Motor Carrier Safety Regulations (FMCSRs), a person is not physically qualified to drive a Commercial Motor Vehicle (CMV) if he or she uses any Schedule I controlled substance such as marijuana even if it is recommended by a licensed medical practitioner.”

The situation is especially difficult for drivers who consume because many of them travel through multiple states with varying approaches to legalization.

The latest change in drug regulation by FMCSA was that they have increased the drug testing frequency rates from 25% to 50% in 2020. As a result, it is expected to add around 50 mil - 70 mil cost for testing annually for the trucking industry and decrease the supply of drivers due to detected more drug cases.

Fuel

The trucking industry is definitely affected by the volatile fuel market. The fuel price is unpredictable and companies are doing their best to minimize fuel price movement. As a result, the company policy is very important to manage the surging fuel price.

As for ODFL, they do have their own fuel storage and pumping facilities on certain service centers. This is to take advantage of low fuel prices for storage purposes. Besides, they also have a fuel surcharge program to transfer some of their cost to its customers to minimize the fuel price impact.

Competitor analysis

Market share

The industry will continue to consolidate as smaller competitors are unable to compete efficiently. The largest 5 and 10 LTL motor carriers accounted for approximately 58% and 83%, respectively, of the domestic LTL market in 2021.

As for ODFL, its market share has grown from 2.9% in 2010 to 12.1% in 2021. It is currently the 3rd largest LTL operator in the North American market by revenue.

However, there is increasing interest from third-party logistics companies and digital marketplaces. This is due to higher profitability posted by the LTL players, it has attracted more players into the industry. For example, Knight-Swift acquired AAA Cooper Transportation in 2021 and Uber offered Uber Freight to compete within the sectors.

Although there is increasing competition, the incumbents still have the upper hand due to their experience and scale. It takes years to build the strategic infrastructure to reach their scale and enable them to deliver their goods efficiently.

Efficiency

By looking at the metrics above, ODFL stands out. Although their competitors have more service centers, they are experiencing decreasing shipment per day. (poor optimisation) On the other hand ODFL has been able to expand its service centers and increase their shipment per day concurrently.

This should be partly attributable to ODFL strategic expansion in improving their network density and efficiency which has resulted in great improvement in their shipment per service center per day.

Profitability/Yield management

The overall statistic that jumps out the most is that ODFL’s revenue/shipment is materially higher (1.5x) than all of its similarly sized competitors. It is due to them being able to carry more weight per shipment.

Based on the table above, ODFL's ability to optimize each shipment weight and charge a more premium price relative to its peers suggests great capacity and yield management. It helped them to generate above industry returns.

Management

Old Dominion Freight Line has been led by the Congdon family since 1934, when founders Lillian and Earl Congdon Sr. started the company with a single truck making runs between Richmond and Norfolk. With hard work and great execution, the company has transformed the company from small company to the national leading trucking company.

The company has been led by its own family members from grandfather to their grandson. However, as part of the company succession planning, Greg C. Gantt is the first non-family member to serve as president and CEO.

Gantt has been working with the company for more than 2 decades and had the benefit of working under both Earl and David Congdon as CEO. Earl Congdon Jr is a legend in the industry, having in March 2018 received the first ever Diamond Legacy Award from the American Trucking Associations.

Culture

ODFL shares the characteristics of great companies like Home Depot, etc. The company respects its employees and treats them as assets, instead of liabilities. As a result, there is no surprise to note that the average tenure of their drivers is around 8 years and average tenure of its BOD is around 9 years.

There is also an ownership culture here that is hard to copy. It is a family controlled business with them collectively owning close to 18% stake in the business. The family members still actively participate in the company although they are no longer steering the company. For example, David Condgon is still the executive chairman of the board.

Scuttleblurb also made an interesting point on the culture in his ODFL 2017 post:

“Two salesmen I spoke with a few years back had their entire 401(k)’s in Old Dominion stock and conveyed that Old Dominion stock is widely held among rank-and-file employees. ODFL shares comprise over 20% of employees’ 401(k) assets. A significant portion of service center managers’ quarterly bonuses are directly tied to profitability and service levels.”

Longevity of a business is highly correlated with the ownership of the owners as they will do their best to ensure their business thriving due to aligned interest.

Opportunities

E-commerce

E-commerce penetration has reached 20% of global retail sales and it is forecasted to reach 30% for the next 5 years. The main tailwinds for them would be the increasing demand for suppliers to sell to bigger players. ODFL is seeing business going to the distribution centers of companies like Amazon and Walmart.

Take Amazon Prime Day, for example, retailers were not allowed to participate in Amazon Prime Day unless their products were in an Amazon Distribution Center prior to the day. LTL spiked heavily in the weeks prior as retailers scrambled to get their goods to Amazon DC’s. In the words of CFO Adam Satterfield:

“The e-commerce trends, I think it is a long-term tailwind for the industry just because of the supply chain dynamics of how freight just sort of moves through versus large distribution centers to store deliveries versus the smaller fulfillment centers. Wolfe Research May 2020 Conference, transcript from TIKR.com

Current composition for their revenue breakdown are 55%-60% on industrial related, 25-30% retail related, and others 10%-20%. Looking forward, e-commerce should drive their sales further due to their specialization in next day or second day delivery.

Autonomous vehicles

Companies are working hard to invent the next generation autonomous trucks which would essentially revamp the whole trucking industry. With AV technology, companies could save huge amounts of costs by reducing drivers and fuel consumption. At the same time, they could operate their fleets with precision and around the clock (24/7 if possible).

Currently, there are regulations that a driver could only drive for 60 hours consecutively for a week. With no such restrictions, they could basically double the hours of operation and it means more profit for the company.

However, the technology might take years before it is mature enough for driving long distances and there will be rejections from the drivers as it means lesser work opportunities for them. It is a tough balance to maintain.

Financial comments

ODFL has been one of the best operators within the LTL industry. It has the highest profitability within the industry (GPM-53%, OPM-26%). For the past 5 years, the company has been growing its revenue at a CAGR of 12%, operating profit at a CAGR of 24% and operating cash flow at a CAGR of 23%. Its return on capital employed has also increased from 23%-37% over the past 5 years.

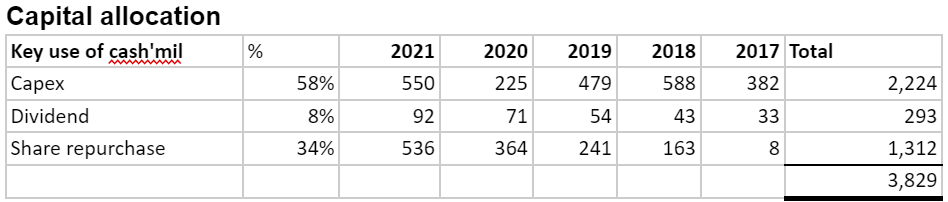

As for capital allocation, the company has been vocal on their strategy to grow organically. Their last acquisition was performed during 2007 and acquisitions usually destroy value than add value to the business.

They have been disciplined in allocating 58% of their cash flow for opening more service centers, growing their fleets, improving technology etc. It is crucial in improving the company network density which should lower their operating costs.

The rest of their cash flow (42%) was returned to its shareholders. The company has increased their dividend consistently and reduced their share count by 2% annually for the past 10 years.

It has a strong balance sheet and they are in a net cash position ($600mil). They rely less on debt and more on internally generated funds as it is the lowest cost of capital. Due to minimal use of debt, the company can easily survive the next crisis and take advantage of any market softness by acquiring more valuable assets at lower price.

In conclusion

ODFL operates in the LTL segment that is a rather niche market within the trucking industry. It is also fairly cyclical and depending on the economic activities from industrial and retail. It can be badly affected by excess capacity like what happened in the 2008 financial crisis.

However, there will always be some outliers which they could perform extremely well even if they operate in a tough industry. Costco being a great example. The key is to differentiate and execute well.

ODFL being one of the companies which have executed well over the years. The company has consistently outperformed the market and has a clear strategy to win market share. The key is to focus on increasing their efficiency to reduce cost, investing in their people and equipment, offering better services,etc.

Although the moat for the company is not visible, the ability to consistently generate incremental ROIC and market share means the company has been doing the right thing.

The author of 100 baggers commented that ODFL might have an “invisible moat”. An invisible moat is one that doesn’t seem to fit any of the traditional buckets, but one that leaves a trail of rising ROICs and increasing market share.

Like all great businesses, they always have a higher valuation. There is no exception for ODFL and it is richly valued as compared to their competitors. TIKR has a great comparison between the companies valuation. Quality business is important but its valuation is also equally important as well.

Disclaimer: I have no position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion.

Resources

Setting The Table: The Freight Transportation Industry by Vanck

Deep Dive: Old Dominion Freight Lines by Vanck

25: Old Dominion Freight Line (ODFL) by Adam Mead

How Old Dominion's service-center strategy drives LTL success by Jim Stinson

Q&A: Old Dominion's David Bates on the Keys to the LTL's Success by Deborah

Invisible Moats by Chris Mayer