OLLI – Scale Changes the Game

An earnings update on Ollie’s Bargain Outlet Q4 FY25

Dear readers,

It’s time for another earnings update on Ollie’s Bargain Outlet (OLLI) following the company’s Q4 FY25 earnings release.

If the previous quarter was about winning hearts and minds, this quarter was about something more structural:

scale is beginning to change the economics of the business.

Management made it clear that the company has reached what they describe as an inflection point, where growing size and industry disruption are creating better access to merchandise, better real estate opportunities, and stronger negotiating leverage with suppliers.

As CEO Eric van der Valk explained:

“Our growth and the continued consolidation of the retail sector is leading to more buying power and expanding our access to products.”

In other words, Ollie’s is no longer simply reacting to closeout opportunities.

It is beginning to shape them.

Financial Performance

Q4 FY25 Highlights

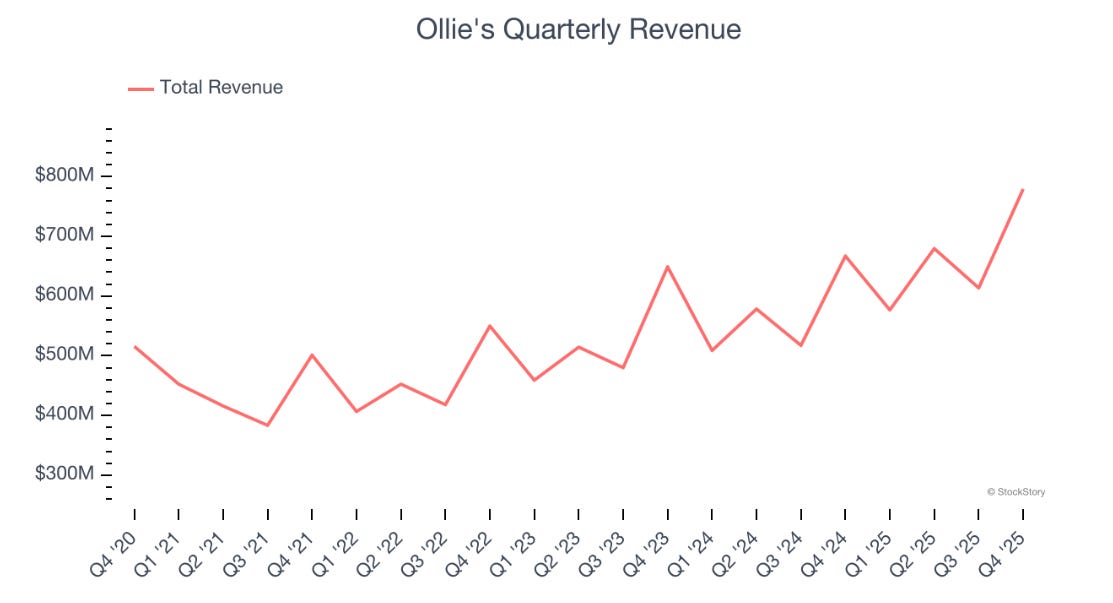

Net sales: $779 million, up 17% YoY

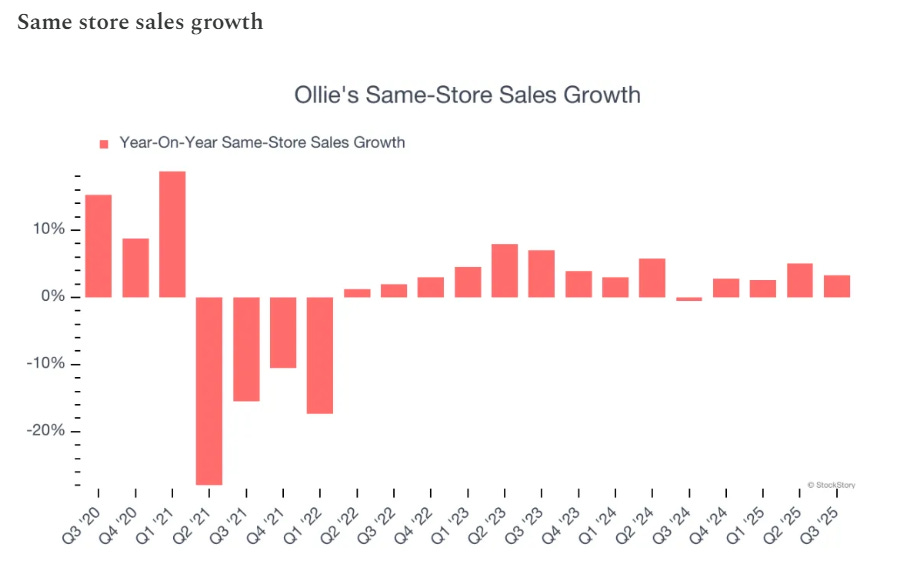

Comparable store sales: +3.6%

Adjusted EPS: $1.39, up 17% YoY

Adjusted EBITDA: $127 million, up 16% YoY

Gross margin: 39.9%

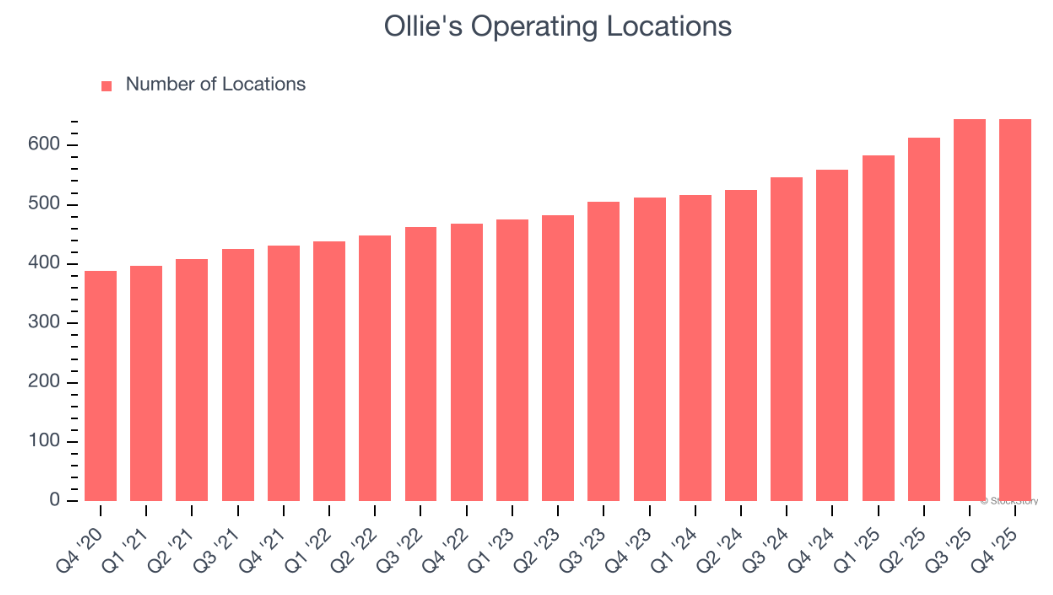

Stores: 658 locations across 35 states

Ollie’s Army members: 17 million

Cash and investments: $563 million

Long-term debt: none

The company also introduced a new long-term operating framework, targeting:

~10% annual store growth

2% comparable store sales growth

40.5% gross margin baseline

mid-teens EPS growth

Sales Growth

Sales growth remained strong at 17%, driven primarily by new store openings.

The company opened 86 stores in 2025, significantly above its previous record of 50.

More importantly, management believes this pace is sustainable.

With 658 stores today and a long-term target of over 1,300 stores, Ollie’s believes it is only halfway through its store expansion opportunity.

For FY26, management expects to open 75 new stores, with most leases already secured.

This translates into roughly:

~10% unit growth

~2% comp growth

Together, this implies ~12–15% revenue growth visibility for several years.

Same Store Sales

Comparable store sales grew 3.6% in the quarter.

Growth was driven by both:

basket size

transaction growth

Basket accounted for roughly two-thirds of comp growth, with transactions contributing the remaining one-third.

Importantly, management noted that the quarter was negatively impacted by severe winter storms, which caused temporary store closures. Absent those disruptions, January would likely have been the strongest month of the quarter.

Momentum has reportedly continued into Q1.

Retail Consolidation Is Creating Opportunity

One of the most interesting themes from the call was the unusually strong deal flow environment.

Management described deal flow as:

“off the charts across just about every category.”

This environment has been driven largely by retail consolidation.

Over the past two years, several value-oriented chains have either closed stores or entered restructuring, including:

Big Lots

Value City Furniture

American Freight

For Ollie’s, these disruptions create opportunity across multiple fronts:

Real estate availability

Access to inventory and closeouts

Hiring experienced retail staff

Customer demand migrating to remaining players

Stores located near former Big Lots locations have reportedly been among the strongest performing in the fleet.

Carpet Out, Furniture In

Another important metric for discount retailers is store productivity, usually measured by sales per store or per square foot. TJX and Ross have been the most successful off-price retailers largely because they consistently improved sales per store over time.

“We’ve also been on a journey thinking about this, how we value store space, how we drive higher space productivity within the box for multiple years at this point. Beginning with some of the learnings that we took away from our remodel program several years ago and it’s resulted in our confidence to accelerate some investments in the business and to steer categories in a more deliberate way.”

By contrast, Ollie’s sales per store have remained relatively flat at around $4.1 million annually. This makes management’s comments about optimizing category mix and store space, such as replacing carpet with furniture, particularly encouraging if it can help improve store productivity over time.

Management explained that wall-to-wall carpet has historically been a category with low productivity per square foot.

As a result, Ollie’s has begun replacing that space with entry-level furniture offerings, particularly living room furniture.

This decision is partly driven by the same retail consolidation mentioned earlier. With chains like American Freight disappearing, a gap has opened in the deep discount furniture market.

Furniture also offers several advantages within Ollie’s treasure-hunt model:

higher ticket items

strong demand during tax refund season

visually compelling in-store displays

better productivity per square foot

The initiative is still early and management noted the rollout is only about seven weeks in but early results have been encouraging.

That said, furniture may not be as straightforward as it appears even best-in-class operators like TJX have struggled to replicate the same success in furniture as in their core categories, and Ollie’s will likely have to compete directly with these experienced players. Below are some challenges i might think of:

Bulky logistics and inventory management, making furniture harder to handle than smaller closeout items.

Slower inventory turnover, which could pressure store productivity and working capital.

Execution risk, as furniture merchandising requires different expertise than Ollie’s traditional closeout categories.

Peer Comparison

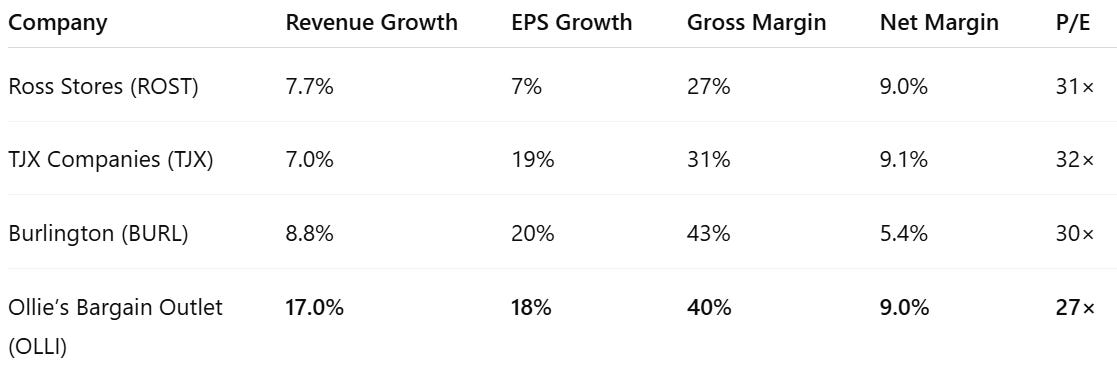

The off-price retail sector provides an interesting benchmark for evaluating Ollie’s positioning for FY2025 result.

Several observations stand out.

First, Ollie’s revenue growth is roughly double that of its peers, largely driven by store expansion.

Second, the company’s net margin remains comparable to the larger players, suggesting that despite its smaller scale, Ollie’s is still able to earn similar profitability.

Finally, despite these characteristics, Ollie’s currently trades at the lowest valuation multiple among the group.

The central question for investors is therefore not whether Ollie’s is growing quickly today, but whether that growth and margin structure can remain intact as the company scales toward 1,300 stores.

Balance Sheet

The balance sheet remains a strategic advantage.

The company ended the quarter with:

$563 million in cash

no meaningful long-term debt

Management also announced a commitment to return roughly 50% of free cash flow through share repurchases, beginning with approximately $100 million in buybacks during FY26.

This combination of strong cash generation and minimal leverage gives Ollie’s considerable flexibility when sourcing large closeout deals.

Conclusion

Q4 reinforced the core thesis behind Ollie’s.

The company continues to benefit from three powerful structural forces:

Retail industry consolidation

Scale advantages in the closeout market

A disciplined treasure-hunt merchandising model

As management put it:

“The most challenging decisions we have to make is what not to buy.”

When the primary constraint of a closeout retailer becomes selectivity rather than supply, the business is operating from a position of strength.

Ollie’s is still early in its store expansion journey, yet the advantages of scale are already beginning to appear in sourcing, real estate, and customer acquisition. I remain a confident long-term holder.

Disclaimer: I have a position in the company mentioned and receive no fees for writing this post. This is not investment advice. Invest at your own discretion.

Sources: I am using Stock story for charts.