Prosus: The tencent proxy

Is Prosus a good vessel for investor to buy Tencent?

Position for the Long Term

I recently watched a video of Pulak Prasad, one of the investors I admire most where he spoke about being completely comfortable missing Amazon.

That stayed with me.

He didn’t say Amazon wasn’t a great company. He simply acknowledged that it wasn’t within his framework at the time. And he was at peace with that. Different strokes for different folks.

I even wrote to him about it, and he was kind enough to reply. The message was simple but powerful: you do not have to play every game. You do not have to own every winner.

That is exactly what I want to practise.

When you manage your own capital, you do not have to perform for quarterly optics. You do not have to chase what is working simply because it is working. You do not have to follow the crowd.

You can choose your path.

And I am, by nature, a contrarian.

Right now, the obvious trade is artificial intelligence. You did not need extraordinary insight to generate strong returns over the past year. Buying memory manufacturers, advanced packaging players, AI infrastructure providers, or even Chinese model companies like MiniMax or Atlas Knowledge could have easily doubled or tripled your capital in a short period. I call them FOMO trades. Many investors did exactly that and they deserve the credit.

But when investing begins to feel easy, I become cautious. Consensus trades tend to embed perfection into valuation. When expectations stretch too far, even small disappointments can trigger sharp repricing. That is not a dynamic I am comfortable underwriting with deep conviction.

I do not optimise for speed.

I optimise for survival.

My time horizon is measured in years, not quarters. I am not trying to predict which stock will outperform over the next three months. I prefer businesses that have been tested over time, companies that have demonstrated resilience across cycles, leadership changes, regulatory shifts, and competitive pressure.

My target is simple: protect the downside and allow the upside to take care of itself. I am less concerned about timing the exact bottom. What concerns me far more is permanent capital loss: getting the business wrong, misjudging the moat, or backing poor capital allocation.

Investing is hard. Contrarian investing is harder. I may miss some spectacular winners along the way. But I would rather miss what I do not fully understand than chase what I cannot underwrite with conviction.

That discipline is what leads me to situations like Prosus.

Prosus: More Than a “Tencent Proxy”?

Prosus is often reduced to a single sentence: it is merely a Tencent proxy. For years, management themselves joked that Prosus was simply “Tencent minus.” Its valuation is cheaper than the Tencent holding itself.

The company that once made one of the greatest investments in history somehow became a perpetual discount vehicle for that very success.

In investor conversations, Prosus was not analysed on its own merits. It was treated as a derivative, a slightly more complicated way to own Tencent, with a structural haircut attached. “Why not just buy Tencent directly?” was the constant refrain.

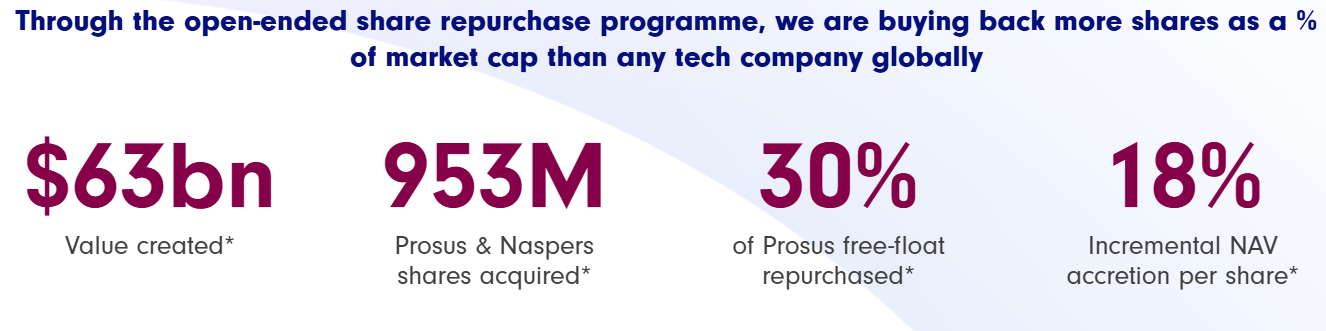

Sources: Prosus share buyback program

New management is acutely aware of this perception. The current capital recycling strategy, selling a portions of Tencent to buy back Prosus shares, is essentially an attempt to reverse the nickname. If Prosus has been trading as “Tencent minus,” the goal is to turn it into “Tencent plus” on a per-share basis.

Whether they succeed is still an open question.

That simplified description of Prosus as merely a Tencent wrapper also oversimplifies the situation. Yes, Prosus owns a substantial stake in Tencent, an investment that traces back to one of the most extraordinary capital allocation decisions in modern history.

In 2001, Naspers invested thirty-two million dollars into a relatively unknown Chinese internet company. That stake eventually grew into an asset worth well over one hundred billion dollars. Few investments in global markets can rival that magnitude of value creation. History will remember that investment as exceptional.

However, the relevant question today is not what happened two decades ago. The real question is whether Prosus is simply a lucky relic of that decision, or whether it remains a discounted capital allocation platform with meaningful compounding potential from current prices.

To answer that, we must understand the foundation beneath it: Tencent.

Tencent: The Foundation Beneath Prosus

If Prosus is largely a reflection of Tencent, then the first question is not about holding company discounts or capital recycling. It is about the quality of the underlying asset.

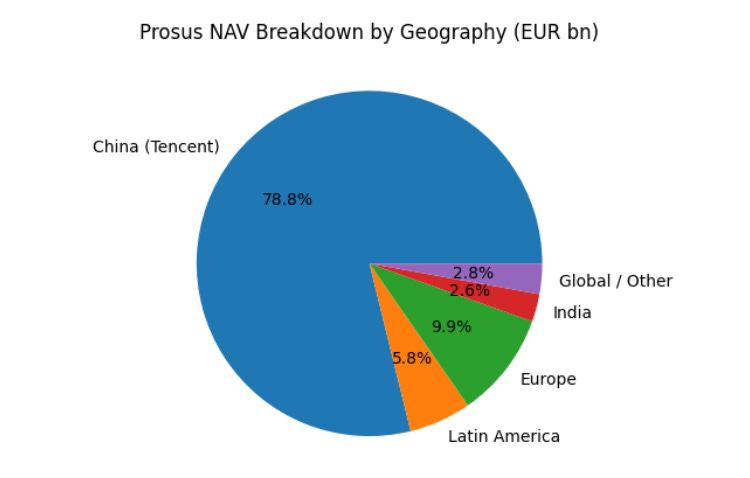

Tencent accounts for roughly 80% of Prosus’ net asset value. The durability of this single asset therefore determines whether the entire thesis stands or falls.

So before discussing structure, incentives, or discount mechanics, we need to answer a simpler question:

How Good Is Tencent Today?

Its gaming division alone would justify serious attention. Tencent is not dependent on a single franchise; it owns or controls major global studios such as Riot Games, Supercell, and Epic Games, among others. At scale, gaming becomes social infrastructure.

Successful franchises evolve into persistent digital communities where network effects are powerful and switching costs are social rather than functional. Engagement deepens over time. Monetisation compounds. Tencent has effectively industrialised gaming into a recurring free cash flow engine rather than a purely hit-driven entertainment business.

Beyond gaming lies WeChat, arguably one of the most powerful digital ecosystems ever built. With over a billion active users, WeChat functions as the digital operating system of daily life in China. Messaging, payments, commerce, content, services, and mini-program ecosystems coexist within a single interface.

Users can complete nearly every aspect of their daily routine without leaving the application. The network effects are layered and mutually reinforcing. Social identity links to payments. Payments link to merchants. Merchants link to mini-programs. Tencent has historically monetised this ecosystem with restraint, prioritising durability and user experience over aggressive short-term extraction.

Tencent has also acted as an ecosystem incubator and long-term investor. Companies such as JD.com, Pinduoduo, and Meituan leveraged Tencent’s traffic, payment infrastructure, and strategic backing during their scaling phases. Tencent does not need to own everything outright; it amplifies ecosystem participants and benefits from their growth through minority stakes and strategic investments.

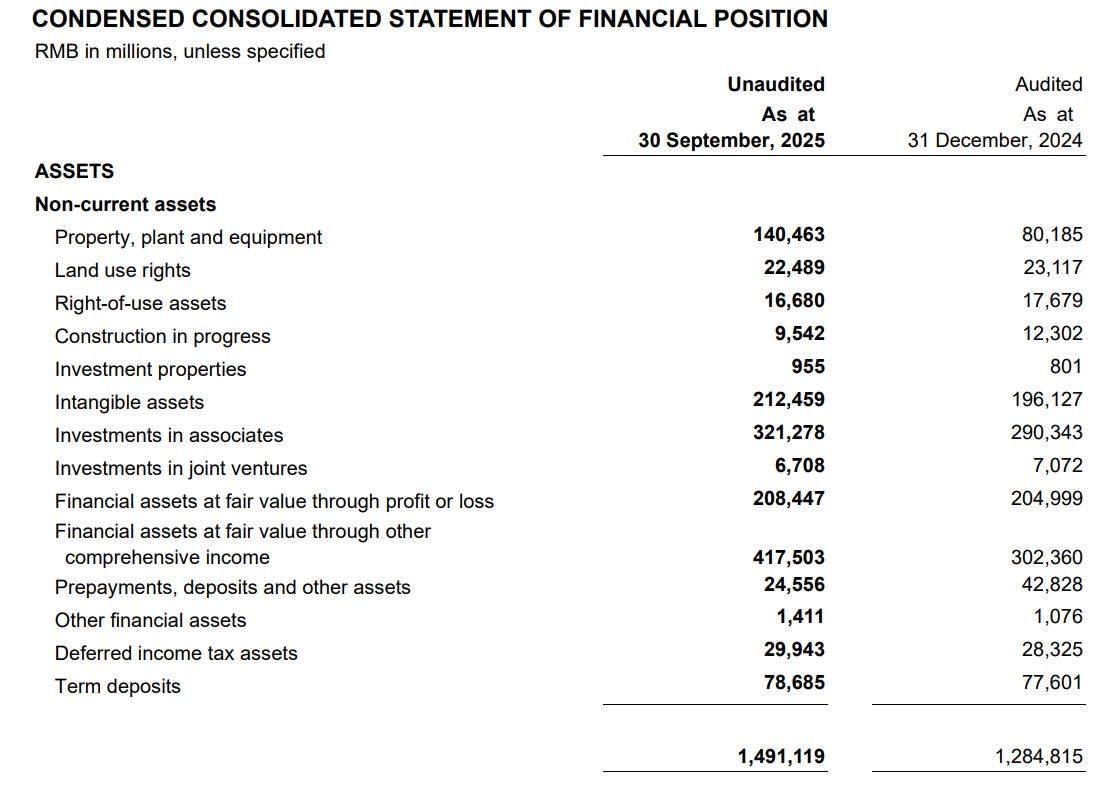

Sources: 30/09/2025 press release

Importantly, this is not a small side activity. As of 30 September 2025, Tencent’s balance sheet includes approximately RMB 626 billion (US$85–90 billion) in financial assets measured at fair value, alongside roughly RMB 321 billion (US$45 billion) in investments in associates. Combined, this represents well over US$120 billion of strategic equity exposure outside its core operating businesses.

This portfolio provides both optionality and financial flexibility. It allows Tencent to participate in the growth of adjacent platforms while maintaining capital-light exposure. At the same time, these investments can be monetised if needed, reinforcing Tencent’s balance sheet strength.

Tencent is therefore not merely a gaming and social media company. It is also a substantial technology investor with one of the largest strategic equity portfolios in Asia.

From a financial perspective, the business remains remarkably resilient. Tencent is currently growing revenue/earnings in the range of roughly 10–15% annually, despite its enormous scale. It operates with high margins (NPM of 20-25%), strong free cash flow generation, and an asset-light structure relative to its revenue base. Capital intensity is modest compared to heavy infrastructure tech peers.

At less than 20x earnings, Tencent is not priced like a speculative growth stock. For a business with dominant network effects, diversified revenue streams, strong cash generation, and double-digit earnings growth, that multiple is hardly excessive by global standards.

In many ways, Tencent fits the criteria I look for in a high-quality business: durable moat, asset-light model, high returns on capital, recurring revenue streams, and disciplined capital allocation.

Tencent is not without risk. Regulatory and geopolitical uncertainty remain real, and growth has moderated from its hyper-scale years. AI also introduces a new competitive dynamic. User attention is fragmenting, and some smaller LLM players appear more aggressive in foundation model development.

There is a concern that Tencent may not be leading the AI race. But Tencent’s strength has never been about winning hype cycles. It has been about embedding technology into a billion-user ecosystem and monetising it at scale whether in gaming, advertising, or payments.

The real question is not whether AI matters, but whether it weakens or strengthens Tencent’s ecosystem. Moats built over decades rarely disappear overnight, but they must evolve.

How about the rest of the pie, the 20%?

If Tencent anchors roughly 80% of Prosus’ net asset value, the remaining 20% is where the strategic evolution is quietly unfolding. For years, the non-Tencent portfolio was viewed as a loose collection of venture-style bets, interesting, but structurally loss-making and capital intensive. That description no longer fits.

In FY25, the Ecommerce portfolio generated US$6.2 billion in revenue and US$443 million in EBIT, a more than tenfold improvement versus two years ago, with group EBIT turning positive. This is no longer experimental capital; it is an operating ecosystem moving toward sustainable profitability.

Food Delivery: From Growth Story to Cash Engine

Food delivery is the clearest example of this transition. iFood, Prosus’ Brazilian platform, now delivers over 120 million monthly orders and generated US$226 million in aEBIT. At scale, delivery becomes infrastructure rather than a promotional battlefield. AI-driven route optimisation, fraud prevention, and automation are improving margins while strengthening user experience.

The proposed acquisition of Just Eat Takeaway.com signals that Prosus intends to replicate this playbook in Europe, aiming to build a multi-region AI-enabled delivery platform rather than remain a regional champion.

Ecosystem Depth: Classifieds, Fintech and Etail

Beyond food delivery, the ecosystem logic becomes clearer. OLX operates asset-light marketplace businesses with embedded monetisation through transaction services. PayU processes significant payment volumes and continues to improve margins, acting as the connective tissue between commerce and consumers.

eMAG in Central and Eastern Europe has turned positive at the aEBIT level, reinforcing the shift toward self-sustaining platforms. These businesses are increasingly interlinked: marketplaces drive engagement, fintech enables transactions, and shared data enhances monetisation. The whole becomes more valuable than the sum of its parts.

Capital Discipline Emerging

Equally important is the change in capital allocation behaviour. Prosus has exited non-core stakes and narrowed losses in segments such as EdTech, demonstrating greater financial discipline. The objective is no longer growth at any cost, but ecosystem-level profitability. This marks a maturation phase, one where management is focused on compounding returns rather than simply expanding footprint.

Why This Matters for the Thesis

Tencent remains the anchor: a high-margin, asset-light platform growing at roughly 10–15% annually and trading at under 20x earnings. I like Tencent as a business on its own merits. But Prosus adds a second dimension. You gain exposure to Tencent at a discount, while owning a portfolio of improving, AI-enabled ecommerce platforms that are beginning to stand on their own.

In that sense, Prosus is not merely a vessel. It is a capital allocator layered on top of a world-class asset, with an increasingly credible second engine of value creation. That optionality if executed well is where the asymmetry may lie.

Paid Section Preview

In the next section, I will quantify the magnitude of that discount and discuss why own Prosus rather than Tencent. Because the question is not whether Tencent was a great investment in 2001. The question is whether Prosus is mispriced today.

If you find this kind of long-form, independent thinking valuable, your support genuinely matters. It enables writers like us to keep doing the slow, uncomfortable work of thinking clearly when narratives are loud and prices are volatile.

Thank you very much for reading and for supporting independent research.

Disclaimer: The information in this newsletter is for educational and informational purposes only. I might hold positions in the securities mentioned. This is not investment advice and should not be taken as a recommendation to buy or sell any security. Always conduct your own research before making investment decisions.