$SHW: The century old compounder

Bringing color to the world for more than 150 years

Company: The Sherwin Williams

Ticker: SHW , listed in US

Industry: Paint

Breaking news

Before i continue with today post, i am pretty sure that most of my readers are highly aware of the Silicon Valley financial group (16th largest banks in US) is having a bank run. If you are not, below is a good article that basically gave a good summary about it. The company basically collapsed within a few days and it just shows that investing is tough.

Why was there a run on Silicon Valley Bank? By Noah Smith

Introduction

Sherwin-Williams is the leading provider of architectural and industrial coatings globally. Internationally, many of its products are distributed through a small selection of company owned stores and through a network of retailers, dealers and distributors.

Business model

The company primarily engages in the manufacture, distribution, and sale of paints and coatings. There are 3 main core groups for Sherwin Williams to generate revenue.

The Americas Group - 56%

The Americas Group consisted of company-operated specialty paint stores. Each store in this segment is engaged in servicing the needs of architectural and industrial paint contractors and do-it-yourself homeowners. These stores market and sell architectural paint and coatings, protective and marine products, OEM product finishes and related products.

Consumer Brands Group - 14%

The Consumer Brands Group supplies a broad portfolio of branded and private-label architectural paint, stains, varnishes, industrial products, wood finishes products, wood preservatives, applicators, corrosion inhibitors, aerosols, caulks and adhesives to retailers and distributors (Lowe, Ace Hardware,etc) throughout North America, as well as in China and Europe. Approximately 62% of the total sales of the Consumer Brands Group in 2021 were intersegment transfers of products primarily sold through The Americas Group.

Performance Coatings Group -30%

The Performance Coatings Group develops and sells industrial coatings for wood finishing and general industrial (metal and plastic) applications, automotive refinish, protective and marine coatings, coil coatings, packaging coatings and performance based resins and colorants worldwide.

Bull

Accessibility

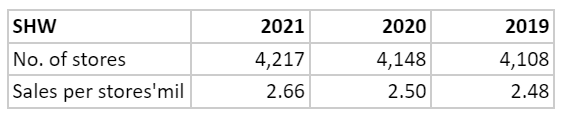

I believe that the rationale for opening a specialty store to sell their products make sense in this context. SHW owned around 4,217 specialty stores in the US in 2021. According to Scraphero, it is serving around 80,000 people to 150,000 per store. The company is targeting to open 80-100 stores annually to reach their potential stores limit - 6,000 stores in the long term. The benefit accrue to them will be on a few levels.

First of all, the investment will help to create a barrier of entries and strengthen their competitive advantage. For example, network density could help them to drive out competition as they have some of the best locations within the region (increasing sales per stores). Besides, it also could help to optimise distribution cost due to more locations (shorter distance).

To put it into perspective, there are around 6,100 Domino's Pizza in the US and it is usually 10-15mins drive away for their customers. This implies that the professional contractors can purchase their products within 20mins drive.

Next, it is also more appealing to professional contractors (their core customers. This is because close proximity and one stop shop as well as inventory availability will reduce their time and cost to travel which will increase their customers productivity.

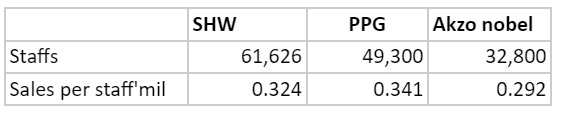

In addition, by having specialty stores, they could raise their prices overnight and use it as a funnel to push their new products efficiently. Well trained staff also give them an opportunity to upsell their products better as they have more knowledge on their products than typical retailer stores. Thereby increasing sales per staff. (Note PPG has higher sales per staff due to their reliance on 3rd distributors)

As compared to their other competitors, they are relying on big box retailers like Home Depot, Walmart, Ace hardware, etc to distribute their products. Although it is less capital and cost intensive, they are lacking the flexibility. This is because there is limited shelf space and a lot more choices available in the big box retailers.

For example, Home Depot has 5 distinct suppliers with PPG and Behr (Masco) being the two largest. To negotiate for more shelf space and raising prices for their products will be a pain in the ass. Besides, retailers will have better bargaining power than the suppliers due to their scale advantage. As a result, their margin will be lower as compared to SHW.

That being said, SHW does have an exclusive distribution with Lowe’s but it is benefiting SHW as SHW has a better bargaining power due to exclusivity. Lowe’s has to dedicate an area as a paint deck to give the same experience that their customers would be getting from SHW specialty stores.

Branding

Consistency of the paint quality plays a more important role relative to price. Their customers want paint that has a thick texture, dries fast, odorless, better finish, less touch up, etc. This is because the cost of paint is relatively low as compared to the total cost of painting (10%-20%). According to fixr.com, painting the exterior of a 1,500 square feet house can cost an average of $5,000, of which $500 - $1,000 are spent on paint.

Imagine if the contractors are using poor quality paint for their projects, there might be delays in their progress which they couldn't afford. For example, cheaper paint tends to be thin and there is a need to coat a few times which will be time consuming. The extra costs in labor as well as reputation damage makes them less price sensitive.

Over time, Sherwin Williams has built its reputation for their great products and consistent quality. Most of the brands they own are #1 or #2 in the respective categories. For example, Sherwin-Williams, Valspar, Dutch Boy, Krylon, Minwax,etc. This gives their customers the confidence to use their products.

The quality and reputation of this brand also led to improved consumer loyalty and recognition as the brand of choice by professional contractors and designers according to the latest report from MarketVision Research and J.D. Power 2020 Paint Satisfaction Study. As a result of reinforcing a brand for more than 150 years, 23 of the 25 top homebuilders in the country use Sherwin-Williams products almost exclusively.

All in, the company has great pricing power and higher pass through ability to its customers. This is great for them as this can minimize the impact from inflation and maximize return.

Relationship

Relationship is harder to quantify for this matter but it is definitely important in winning the heart of their customers. 86% of the company's sales are relying on professionals and it is important to maintain a good relationship with them.

In order to be customer centric, Sherwin Willaims has 3500+ Sales Reps at Job Sites to observe and obtain direct feedback from its customers. As a result, they will be able to obtain unique insights from them and solve their problems quickly. For example, Sheffield metal, one of their customers who has been using SHW products exclusively for more than 20 years.

Supply chain and scale

Paints and Coatings manufacturers generally have a low fixed-cost base, but experience higher variable costs. Coatings production is not capital-intensive. Most of the costs to produce coatings are raw materials. For an average US coatings producer, raw materials costs generally encompass 40-55 % of total sales with total cost of goods sold encompassing 55-70 % of sales.

Thus, it makes sense for Sherwin Williams to be vertically integrated as it isn't costly to build a manufacturing facility. By controlling the production and logistics processes, the company will have the flexibility to control the product quality, scaling or downscale according to market cycle, maximize facility utilization rates and reduce unit costs of distribution.

Besides, the company also can minimize the risk of poor quality during distribution as coatings have a highly complex composition. Unlike PPG, which outsources distribution, Sherwin-Williams controls this process not only to seek economies of scale, but also to mitigate any external risk that ensure the product from reaching the end customer intact in terms of quality.

Competition

Market share

As per KNG research in 2020, the global paint industry is divided into 3 market segments: architectural paints (40%), industrial OEM coatings (40%) and industrial coatings with special purpose (20%). There are around 10.1bil gallons of paint being sold annually with an estimated TAM of $137bil.

The global coatings industry has become increasingly consolidated over the past two decades with the top 10 suppliers representing just over 50% of the global market. Sherwin Williams is currently the leader (13%), followed by PPG (10%), Akzo Nobel (8%), and Nippon (6%).

M & A landscape

Merger and acquisition activity (‘M&A’) has been an essential part of the coatings industry strategy, complementing the strong organic growth witnessed during the past decade. As the market is still fairly fragmented, thus there is room for further consolidation that benefits bigger companies due to their financial strength.

Some interesting acquisitions within the industry include Akzo Nobel and PPG. Akzo Nobel (owning the Dulux brand) was being offered ($30bil) by PPG to acquire its business (the largest deal in the industry) but failed in 2017. However, they managed to acquire its North America architectural business for $1bil.

All in, the competitions were fairly stiff as there aren’t many differences between the competitors. Thus, scale and efficiency will eventually decide who will likely to continuously be the leader in the industry. So far, SHW is leading the pack due to their disciplined capital allocations.

Bear

Cyclicality

The paint and coating industry is also fairly cyclical as both of its sales and purchase depends on the market condition. For example, their sales are dependent on the number of houses built as well as industrial activities. If there is any recession, discretionary expenses would most likely be delayed.

As for its cost of sales, 70% are raw materials. The raw materials are made up of 4 elements: resins / latex, pigments, additives and solvents. Around 60 - 70% are titanium dioxide (China being the world's largest supplier) and oil derivatives. As a result, the input cost is volatile and it will be affecting the company’s margin.

Environmental and health care risk

When dealing with chemical or energy companies, litigation is always a risk. This is because the chemicals involved in producing paints are usually hazardous and there is a need to comply with multiple regulatory guidelines (high compliance cost).

SHW and others were charged for its lead paint that contains toxins in 2000. In 2019, Sherwin-Williams finally settled the lawsuit as one of three defendants in California related to advertising in lead-based paints.

This legal battle lasted almost 20 years. The result is for Sherwin-Williams to pay a fine of $101.7M spread over 7 years. This was a reduced judgment from the court's original $1.15B and $409M (divided by 3) following an appeal. Sherwin-Williams will pay the fines until September of 2025.

E-commerce

Another concern for them would be the rise of e-commerce. Professionals could be buying the necessary products from online retailers. However, I would argue that it is harder to sell online due to the weight and technicality involved before the paint is delivered.

There is a need to mix and stir the paint to ensure it is fully mixed. Hand mixed is usually troublesome and time consuming. It is much easier to visit specialty stores to get the desired well mixed products. This is why most of the SHW stores have a blending facility to assist their customers for this purpose.

Management

Rise to the Top

John G. Morikis joined Sherwin-Williams Co. in 1984 as a management trainee and, in 2016, became the company’s first employee to rise from that position to CEO. He was at the helm last summer when Valspar was acquired - an $11.3 billion move that positioned the company as the global leader in paints and coatings. Under his leadership, the company has grown 2x within 5 years.

The CEO was humble and low profile. These are the three tenets that guide him: good people, hard work and teamwork. “We’re not looking for shortcuts. It’s heavy lifting that we have to do.” The honesty of the management is highly appreciated.

Retention

The company has a culture where people stay. This is because of their policy of investing into their staff. Usually, their new recruit goes through a management trainee program which aims to train them as the future leaders of the company.

This culture is deeply embedded within the organization. For example, 80% of its staff work more than 5 years with the company. More than 7,000 staff worked more than 20+ years with the company.

Besides, most of its top management has worked with the company for more than 20 years. For example, there are only 9 CEOs in the 150 years history of Sherwin Williams. This implies that most of its CEOs worked for at least 16 years in the company before its successor took over.

Low turnover (5-7%) is a great indicator of a good company culture. This is because it not only helps the company to save costs in retraining employees, but also resulting in higher recurrence of sales, higher inventory turnover and higher ROIC per store due to more experienced employees.

Ownership

It is encouraging to note that the insider ownership is relatively high at around 9%. Although it is not founder-led, the culture of the company was highly embraced by its management team and they are long term oriented.

How they can grow

Tailwind - TAM

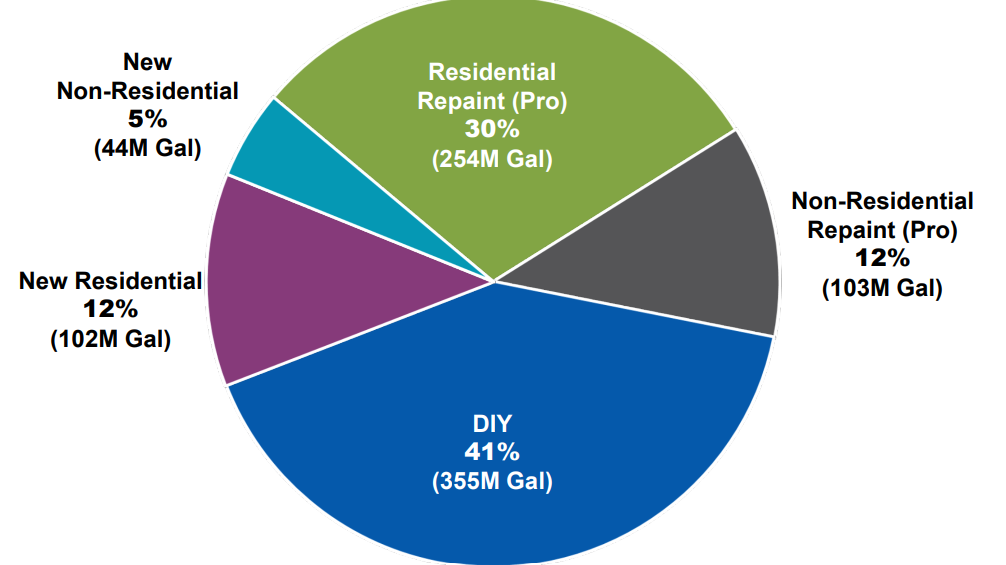

The growth in the paint industry has been relatively stable by growing around 2-4%. As of 2020, there are 858mil gallons of paint being used and it is growing at around 3.2% yoy.

For older houses, about 42% or 357mil is used for repainting and it should continue to expand over the years due to the age of the houses in the US. As per statista, the number of houses in the US aged between 11-40 years are around 40mil. This implies more houses will be up for remodeling and refurbishment.

As for new houses, about 17% or 146mil is used for new housing projects. As per the Department of Commerce, Non-Residential & Residential Square Footage has increased by 19% as compared to the prior peak. This should continue to help SHW to drive their future growth.

Another rising trend being the shift from DIY to contractor. According to the U.S Commerce Department, DIY/Remolder market share has shrinked to 41% and transferred to professional contractors-59%.

This trend actually benefited the company as they are more exposed to professional contractors. It makes sense as the wealth of the household rises, more households are willing to pay up for the professionals to do the jobs insteads of DIY.

International expansions and diversification

The company has a strong foothold in North America with 80% of its revenue derived from it. Thus, it is crucial for them to expand internationally as most of the future growth will come from the Asia Market especially China and India.

The acquisition of Valspar would be SHW's first step to expand its presence in the Asia market. Nippon Paint and AkzoNobel are leading in Asia market. Besides, this acquisition also helped them to diversify into industrial coatings which should further strengthen their lead in the coatings market. They are taking the advantage of the growing demands from bigger infrastructure projects. Ie. China one belt one road initiatives and US infrastructure bills.

Financial comments

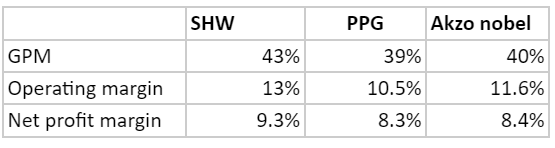

SHW has one of the highest profitability within the industry (GPM-43%). It has been growing its revenue at a CAGR of 7%, operating profit at a CAGR of 11% and operating cash flow at a CAGR of 4.4% for the past 5 years. Its return on invested capital has also increased from 12%-22% implying strengthening of competitive advantage.

As for capital allocation, the company only spent about 8% of their cash flow for capex. It is capital light and requires minimal capital to sustain its business. That being said, the company will need to continue to grow by acquiring great brands.

Acquisitions will be the key playbook for them. SHW has completed close to 30 acquisitions since 2000 with Valspar being the biggest acquisition in 2017. This marks their biggest move into the industrial coating industry.

The rest of their cash flow was returned to its shareholders. The company has increased their dividend consistently and reduced their share count by 2% annually for the past 10 years.

As for their balance sheet, The company is considered highly geared but it is manageable due to be 70% of its debt mature after 2025. The company has been leveraging due to its predictable cash flow ($2bil of operating cash flow vs $10bil of debt).

Besides, they also keep minimal cash on hand ($200mil) and deploy the rest for either reinvestment or returning to shareholders. It is their principal of not holding excessive cash as it minimizes return.

In conclusion

It is fascinating to see how a company could last for more than 150 years and continue to thrive within the industry. Sherwin Williams being the market leader in the field is not by luck but great execution from management.

Besides, Sherwin Williams have strategically acquired and expanded their footprints globally. They have built a portfolio of highly recognised brands globally, especially in North America. I believe the key to their success is due to their discipline in allocating resources by building up a barrier to defend their moats.

The major difference between SHW and their competitors is their investment in specialty stores. Due to the industry being fairly commoditised, SHW has to differentiate by optimizing their distribution network and gaining the distribution advantage. .

By opening specialty stores, they can increase their reach per location and reduce the unit cost of distribution. Besides, they also can differentiate themselves from all the big box retailers which have less knowledgeable staff, their products and more choices for their customers.

Disclaimer: I have no position in the stock and receive no fees for writing the post. This post is just for educational purpose and it is not an advice to buy or sell the stocks. Invest at your own discretion. If you like my post, please also consider to follow me on twitter as well.

Resources

The Global Paint and coating industry by European Coating Journals

Death, Taxes and Repaint by Young Hamilton

Sherwin-Williams (SHW) and the global paint industry by Finding Moats

Products evolution from SHW Investor presentation 2021

Breakdown by addressable market from SHW investor presentation 2021