$Wise: Transfer without border

Can it truly disrupt the borderless payment?

Company: Wise

Ticker: Wise.L, listed in UK

Industry: Fintech

I am back after 2 weeks of rest. Today post will be slightly different than my usual one. I will be letting my readers to decide if this is a great company or just another overvalued overpromised company. This is an interesting company that I came across when I listened to my favorite podcast : Business breakdown.

Do share your comments with me and i would like to learn more about the company or industry.

Investment thesis

While we are talking about sending humans to mars, the way we are moving our money internationally has not changed in decades. International payment remains an inefficient and cumbersome system. Customers are paying exorbitant fees for each transaction.

Source: Migration and development brief 37 by World bank

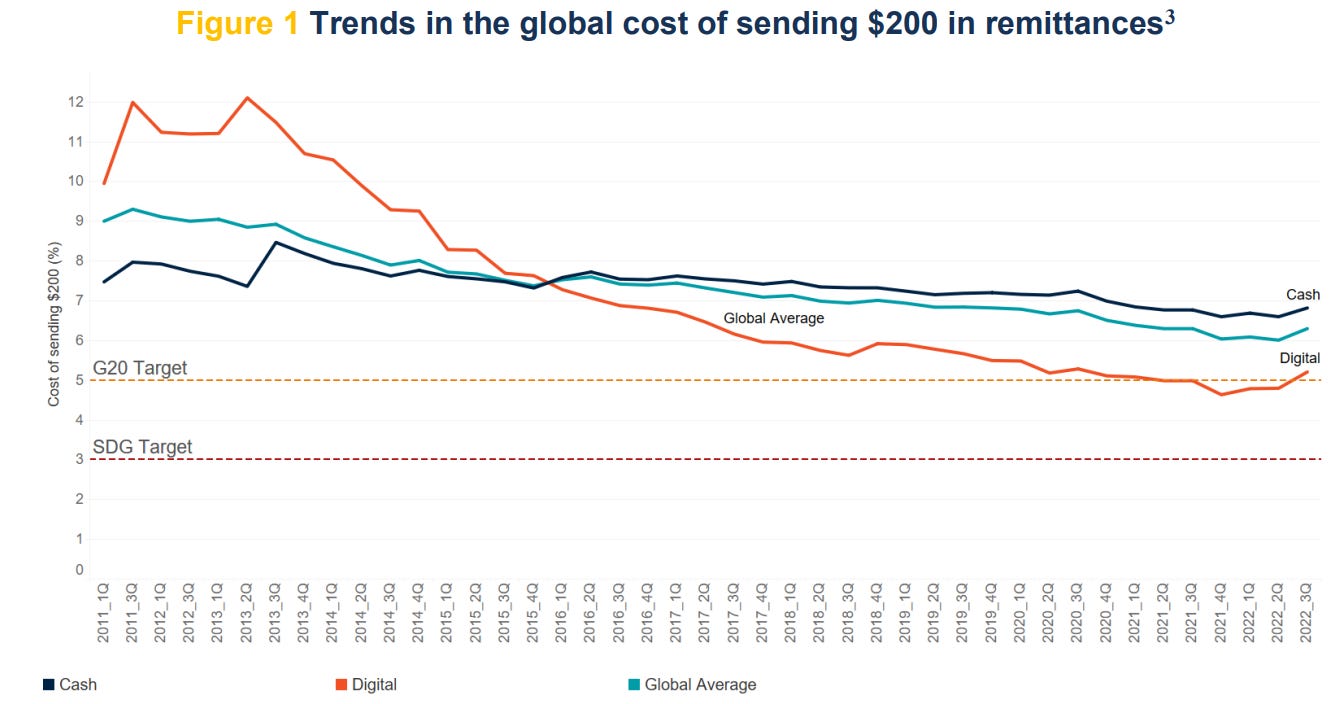

According to the World bank, global remittance costs remained high at around 6% for $200 transfer. It is still at twice the Sustainable Development Goal (SDG) target of 3 percent. Although there are improvements over the years due to technology, regulation and competition, the fees remained stubbornly high. Therefore, this industry is ripe for disruption.

Wise, a newly listed company in the UK vows to disrupt the legacy system by providing an innovative solution for international payment and transfer. Essentially, the company is trying to create a better way to transfer money internationally quicker and cheaper. The CEO of Wise has vowed to eventually remove the fees for transferring internationally. It is certainly a very bold call for a relatively new company as compared to banks.

Well, I am not an expert in fintech but whenever I perform research, these are the questions that pop up in my mind. How does cross-border payment work? How Wise is solving the problem? How big is the market? What is the competitive advantage for Wise to compete with the new players as well as the incumbents? What are some of the risks or challenges that the company faces,etc?

It is going to be an exhilarating learning experience as I go through articles, blogs, podcasts, 10k, etc to get my best view on the industry and company to determine whether or not it is a good business to be included in the investable universe and eventually in the portfolio at the right price.

Here is an outline of the deep dive:

1. An overview of the industry and how Wise solves the problem?

2. Business model

3. Total addressable market

4. Competitive landscape

5. Bull vs Bear

6, Management and culture

7. Conclusion

Industry overview

Source: EY report

How does cross-border payments work?

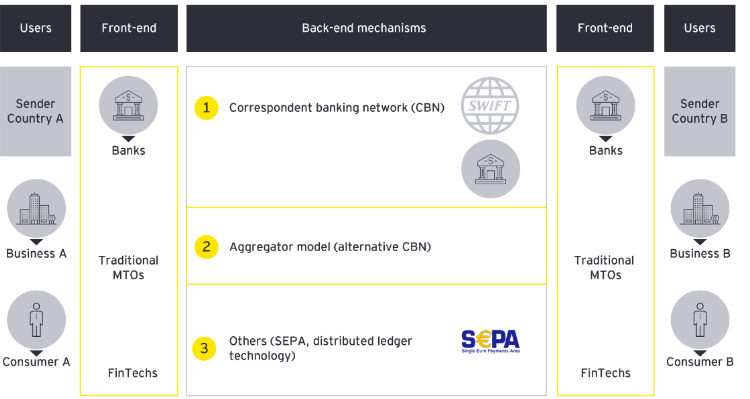

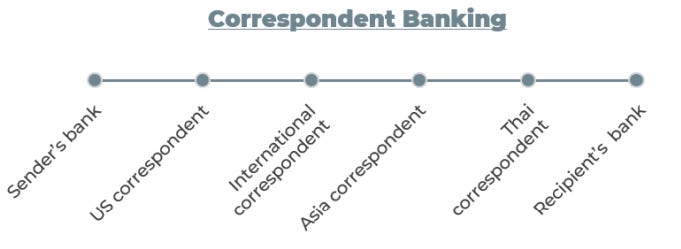

Traditionally, users typically choose a front end provider such as banks or traditional Money Transfer Operators (MTOs) (Eg: Western union) for transfer or payment. These payments flow via the correspondent banking network (CBN) to settle payments.

Source: Wise prospectus

The problem with corresponding banking networks is that money has to flow through multiple layers before reaching its end customers. Besides, there is little competition and it is dominated by a few dominant global correspondents.

As a result, there is lack of transparency, long settlement periods, high transaction costs, and limited accessibility especially for cross-border transactions of exotic currencies. (However: Not much concern on liquid currencies such as USD/EURO)

“For example, a transaction from a local bank account in Germany to a bank account in Senegal can incur costs of more than 100€, depending on the transaction value, and can take up to seven days to settle. And even then, the sender would often not receive a confirmation of the transaction’s success” as mentioned by EY research.

For a more detailed explanation on correspondent banking, Andreessen Horowitz team, a famous private equity fund has a clear explanation on the legacy issues. Click here to learn more. (Note: they have invested in the company as well)

How Wise is solving the problem?

Source: Wise prospectus

Essentially, Wise is trying to disrupt the industry by using a peer to peer model to resolve these issues. Instead of going through the traditional route that involved many parties (means higher fees, lower transparency and slow), they are recreating an alternative network to CBN by being a middleman to match both the origination and receiving. There is no money crossing the border but merely a local transfer from Wise local banks to their respective customers.

For example, if X wants to send US100 to Singapore and Y wants to send SGD136 to US, all Wise has to do is to match the request with their own banks (both in Singapore and US) and the transaction will be completed within a day or sometime instantly depending on the currency pair.

Thus, with this new payment infrastructure, based on Wise's latest H1 investor presentation, 90% of its transactions are completed within 24 hours as compared to banks which will take 3-5 days. Besides, Wise is also 5-10x cheaper than conventional routes due to their peer to peer transfer model. The average take rate for Wise is around 0.64% (excluding other fees) vs 3-7% of banks average fees. However, there are major flaws in their peer to peer model and how Wise can overcome it under the bull vs bear section.

Business model

Let me briefly explain how Wise makes money. Wise reports its revenue in two segments: Personal and Business segment.

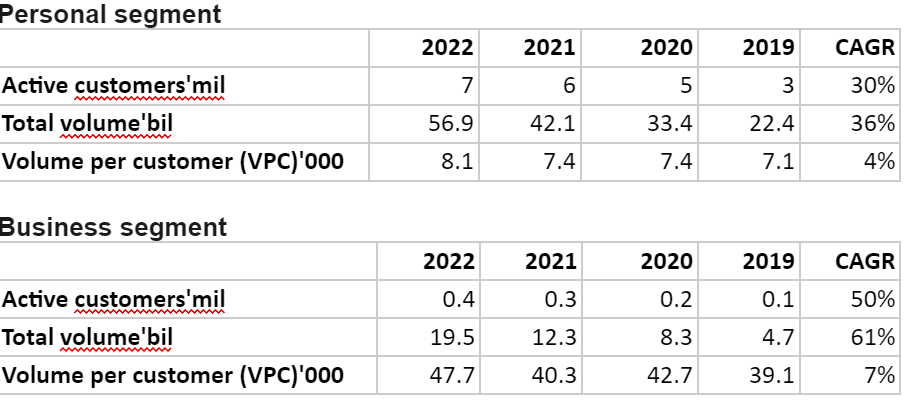

The personal segment consists of C2C (consumer-to-consumer) and C2B (consumer-to business) payments capturing a broad set of cross-border use cases including personal remittances, eCommerce transactions, real estate investments and other bills, like tuition and healthcare payments. However, there is no disclosure on the %revenue of each use case. Thus, I would assume that the majority of the use cases will be for remittance purposes.

Majority of the revenue is derived from this segment. It charges an average take rate of 0.76% for its personal customers. This is the segment that Wise has an edge over their incumbents as these markets are traditionally being underserved and charged the most by the incumbents.

It is supported by a research from EDC that, although Personal and micro/SMB customers make up approximately 50% of the overall market volume, they make up the majority (approximately 95%) of the fees paid.

However, at the same time, it will also attract the most interest from new fintech startups as the barriers of entries are low and the services are highly commoditized. It is going to be very competitive but there are rooms to accommodate few players due to the massive TAM as claimed by the bulls.

The SMB and enterprise segments are composed of B2C (business-to-consumer) and B2B (business-to-business) payments capturing the cross-border payments of wages and salaries, freelancing and subcontracting payments, and accounts payable by businesses for merchandise and services imported from abroad. It charges a take rate of an average of 0.65% for its business customers.

It is a much harder segment to disrupt and it is largely dominated by the banks with market share of around 95% of the market in 2019 as per Wise prospectus. Let me discuss why this segment is harder to disrupt. As per EY report, B2B usually has an average transaction value that is often higher than US50,000. The current unit economics for B2B transactions are better due to the fixed nature of fees. (ie: KYC/AML and compliance processes)

Besides, it requires senders to significantly increase working capital requirements by prefunding high value transactions. For example, if Bank A was to exchange a $10mil deal, Bank A has to fork out $10mil to exchange the money before the clients will pay them due to the T+3 settlement rule. This is where most fintech companies lack unless they are able to secure the funding like banks. For these reasons, almost all high-value B2B cross-border payments are still processed through CBN's.

The volume per customer for either personal or business of Wise is still relatively small and far below $50,000 per transaction. Wise will likely remain active for low value transactions as there is more inefficiency in the system. As Jeff Bezos once said” you margin is my opportunity”. Wise will likely stick with this strategy going forward.

As you can see from the Wise revenue mix, the business segment has been growing at a rapid rate and eventually, the mix will be more equal in my opinion. The business segment total addressable market is simply too big. A small increase in business market share will make an impact towards both their topline and bottom growth.

Supercharging growth? - Wise platform

In order to accelerate their growth, the company is looking to leverage the power of other platforms and access previously untapped customer pools. Wise Chief Product Officer emphasized that:

“In the future, within like 10-plus years, the majority of our volume will come through via the API URL. Not everyone in the world is going to download our app. We’re going to need to be in the banks and the platforms that people use daily for managing their money. And that’s where lead scoring is the fastest growing part of ways.

By introducing Wise platform, it is one of the most important moves by the company to accelerate their penetration. Basically, Wise are partnering with various solution providers or neobank/fintech that need the foreign currencies platform but lack of them.

The rationale is simple as Wise is cheaper and more transparent as compared to legacy players. However, this might not be their north star as their close competitors are also integrating with these players. For example, Xe.comm, another close competitor, has integration with Google Pay or Xero as well.

As for legacies bank, Western Union (legacy competitor) basically is their default platform since they have been working with these players for years. Legacy banks are known for their bureaucracy and old infrastructure. Unless the Wise API is compatible with them, it will be hard to penetrate the wall.

As per Wise prospectus, the annualised volume run-rate of Wise Platform was over £1 billion in 2021. It accounted for a small portion (1.8%) of the total cross border volume of Wise. However, there is no further disclosure afterwards. It could be a good channel for them to grow as the volume should grow with neobanks or fintechs gaining more traction but not easy.

Total addressable market

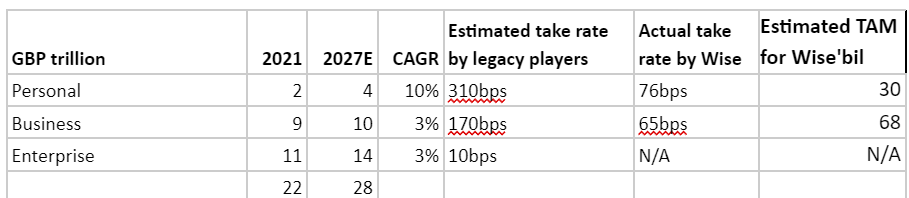

According to Wise's annual report, they cited a report from payments consultant Edgar, Dunn & Company (EDC), the Global cross-border payments market volume is increasing steadily and it is estimated at £22 trillion in 2021 and is expected to reach £28 trillion by 2027. Below is the breakdown of the cross border payment market volume and respective take rate:

Note: The enterprise segment is highly competitive and Wise is unlikely to compete in the segment

To put into context, Wise made up only 4% of the personal market and <1% for the business market in 2021. It does suggest that Wise has a long run way ahead.

Personal segment

The TAM might appear to be huge but it is pretty abstract. My best assumption is that their actual TAM for the personal segment would be the global remittance instead of e-commerce, which is crowded with large payment processors taking up most shares.

To be conservative, if we were to take the global remittance volume, as per world bank, it would be around $800bil. Assuming unchange take rate and 10% growth as suggested by EDC for the next 5 years, their TAM will be around $12bil or £10bil.

Source: Credit suisse on fintech

Besides, it would be misleading to include both digital and non digital cross border volume as Wise dont have the infrastructure to compete for the non digital portion. For example, as per Credit Suisse estimates, 35% of all remittance transactions are cash-based. If excluding cash remittance, their possible TAM will be around £6.5bil.

It is apparent that Wise will not be winning market share on cash based transactions unless Wise partners with players like Western Union (WU) but there will be charges for them to access the infrastructure. The likelihood will be low as WU don't want their business model to be jeopardised by Wise as they will have lower bargaining power as compared to Wise once their volume increases tremendously over WU.

The brightside being that the cash portion is shrinking due to rapid adoption of digital payment by poorer countries. It is still a long way to disrupt the cash remittance as most poorer countries are still using cash for their day to day transactions by statista due to the high unbanked population.

Business segment

It is much harder to estimate as Wise has minimal disclosure on business use cases. To simplify the thinking, let's just take Uk, Europe and US SMEs businesses that employ less than 10 staff as these are the markets that are usually underserved by banks.

Assuming unchange take rate and 3% growth as suggested by EDC for the next 5 years, their TAM will be around $21 bil or £17 bil. It is a huge TAM and Wise will be gearing up to compete in this segment.

Although it is more competitive as compared to the personal segment, (take rate is much lower for traditional channels ~310 bps for personal vs 170 bps for business), Wise is looking to penetrate this market as it will help them to lower the unit economics for each transfer as well as gather local liquidity pools. It is necessary for them to gain competitive advantage over their competitors in the long term.

Bull vs Bear

Flaws in peer to peer model

Let's discuss the flaws of the P2P model first. Bear argues that there is a major challenge with the peer to peer business model as it is inherently assumed that there are an equal number of buyers and sellers in any given currency. That is simply not true as clearly pointed out by OFX CEO, another competitor for Wise. For example, as per an interview with OFX CEO:

“During Brexit, you had lots and lots of sellers and very few buyers. That can lead to an inability to transact because you simply have all these sellers lined up and no buyers. That’s one of the reasons why the peer-to-peer players opted out of their model during this period of volatility because it wouldn’t have been sustainable."

Sources: World bank

Apart from periods of volatility, the remittance market is also inherently imbalanced as per world bank. For example, migrants who work in developed countries will remit their currencies back to their home countries and not the other way around. This will likely cause more problems for the peer to peer model. (currencies mismatch)

However, Bull argues that as Wise grows bigger, Wise will be able to collect more data for their customers and manage the flows better since remittance is somewhat recurring and tends to happen during month end. Then, they could keep higher “inventory” for the period to cope with the demand for certain currencies. For example, Wise has been using ML to predict 50% of the demand for any currencies.

It is still far from perfect as mentioned by their competitors especially during periods of volatility or stress. For example, during Covid-19 period, Wise suffered a huge loss on currency due to highly fluctuating rates and customers are holding their transfers for good rates and the amount transfer also tends to be more lumpy. This will likely distort their algorithms and affect their ability to forecast.

Risk management on forex would be very crucial but there is limited information on how they can minimize the forex risk. (Any readers could share their thoughts with me will be great)

Mid market rate

As a result, Bear argues that Wise will have to act as the principal when there is no supply for the currencies demanded due to their business model of guaranteeing mid market rate for a certain number of hours. Wise has to buy the required currencies from the interbank market and is exposed to currency risk. For example, Wise lose about £20-40 mil a year (5-10% of revenue) on forex and the amount of losses could be huge if they are at the wrong side of the transaction.

Besides, according to the FT article, Wise is not transparent on their disclosure of their matching rate as it is crucial to determine if they have sufficient liquidity pool to match most of the currencies required to limit their forex risk. However, as per FT report, Wise only mentioned that they are able to match 60% of the transactions for liquid currencies pairs like USD/EUR, while the rest are being supported by third party liquidity.

It is definitely one of the shortcomings for their business model. As Wise continues to grow bigger, the management is fully aware of these issues and they are moving away from a pure peer-to-peer play towards a more traditional model. Cofounder Kristo Käärmann told BI last year:

"We always work with a local liquidity provider, someone who has the opposite flows or is able to aggregate the opposite flows. We work quite hard to find a partner who has these flows and is willing to exchange them at a reasonable margin so that it doesn’t become a cost for our customers.”

Bear continued to challenge the business model:

"Whilst you are breaking even or near that, their credit limit would be very small. You have to post collateral which is a proportion of the risk of their exposure. That’s the challenge they’ve got, you do need significant reserves to be able to operate in global financial exchange. It’s not something you can just do with a technology solution, you really need the strength to be able to play in the markets we’re in."

Bull argues that this is not a major issue for Wise as it is profitable and is able to generate high free cash flow due to capital light and operating leverage. Besides, Wise is able to escape the punitive regulation on banks as they are non-banks and subject to lower collateral requirements which allow them to post lower collateral for higher risk exposure. This type of regulation arbitrage is most likely unsustainable as banks will lobby for harsher regulation for these alternatives players.

Shared scale of economy

All these issues argued by bears are valid. However, Bull argued that a shared scale of economy could be the key to compete with incumbents and strengthen their moat. The theory is simple: with more volume through their infrastructure, they could reduce the unit costs and pass down the savings to its customers to create their own flywheel.

At the same time, they could gather sufficient local liquidity pools especially for low liquidity currencies pairs due to their low fees policy. Paypal used to have the local liquidity pool advantage when they partnered with ebay but after the spin off, they are losing the moat and resulted in newer players like Wise to overtake their lead.

With scale and ever growing local liquidity pool, this will effectively solve the currencies mismatch, limit their forex exposure and gather a huge amount of reserve to post as collateral for expanding risks.

The evidence for their strategies are starting to surface as the volume of international transfers are increasing to reach the record high of £76bil and is estimated to reach £100bil by FY2023. It is surpassing most of the MTOs, even Western Union.

Besides, Wise is also gaining more trust from their customers and they are putting more money within the account balances. For example, the deposits have grown significantly over the years to £9bil based on their latest disclosure with personal accounts consisting an average of £486 and business of £8,500.

As a result, the company has been earning a huge chunk of net interest income from the float. Since Wise is not a bank, the company is unable to return the excess to their customers. However, the company is finding a way to return the excess earnings such as introducing investment accounts or rebates for their customers.

Below is an excerpt of CFO take on net interest income on Q3FY23 trading update presentation:

“And the fundamental of this is building up a relationship with our customers that they believe we are charging a fair price. We are not charging what we can, we are charging what we need to. And we think this over time has built this relationship with our customers that means we are charging what we need rather than what we can get away with.”

Wise understands that these are all the positive impacts from the shared scale economy and they are not going to stop their flywheel as this is crucial to defend their competitive advantage.

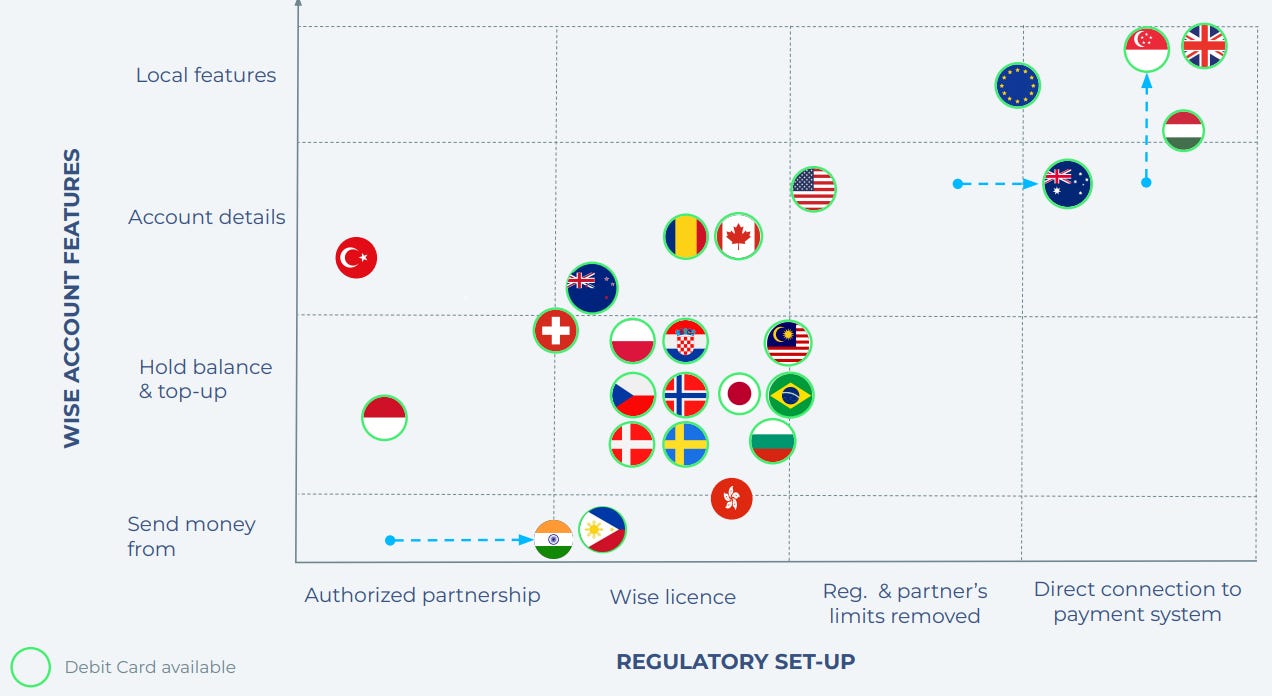

Secondly, Wise is also finding other ways to lower cost and improve transfer speeds as it is crucial for commoditised services like them. Wise is working hard to build an internal payment infrastructure such as accessing directly into national payments infrastructure to provide faster and cheaper money transfers. They want to be an “interbank” themselves.

For example, joining the faster payment service(FPS) in the UK or Singapore FAST system. Bear in mind that countries like Japan, US and India continue to restrict access to banks only. Below is the progress for their regulatory set up:

Source: Wise Q3FY23 investor presentation

Although it does expedite the payment process and lower cost, it is not much of a high barrier for new entrants as central banks are opening up their infrastructure for non banks participants. A good example is that there are more than 10 non-bank participants such as square (known as Block now), revolut,etc participate in the FPS. It is not going to help Wise in winning the stiff competition as this should be the trend going forward for any new entrants.

Currently, Wise only has access to less than 60 countries for either account details, hold and convert or just send money. They are still working to expand their offering to more countries but it will be harder as these countries usually have a lot of red tape and poor regulations. It will be tough to penetrate these markets but not impossible.

Competitive landscape

The large TAM and low barrier to entries certainly attract a lot of attention from new fintech players. This is going to be competitive and it might result in a winner take all scenario. Thus, private funding for global fintechs are reaching record high at over $100bil in 2021 but slowed down to $75.2bil in 2022 according to Techcrunch. It is still a large sum of money injected into the fintech industry.

Some good examples are revolut, currencyfair, Xoom for personal transfer or Airwallex, Currency cloud for business transfer. These companies are competing aggressively by offering zero to low cost for international transfer. Even traditional MTOs are introducing their own digital transfer platform to compete.

However, my focus will be on revolut and western union as currently, these companies might pose the most threat for Wise. As for banks, I believe that they are suffering from counter positioning (wanted to protect high profitability) and their legacy infrastructure will also prevent them from cutting their prices to reach fintech level. The early stage of the disruption will be fintech taking share from legacy players and subsequently competing among themselves.

Personal segment

Since Wise has 2 segments, I will be discussing them by segment. As per Wise prospectus, banks still hold the largest share of the personal segment (66%), with traditional money transfer operators (13%) and other non-banks (21%) comprising the rest of the market.

Money transfer operators

Source: World bank

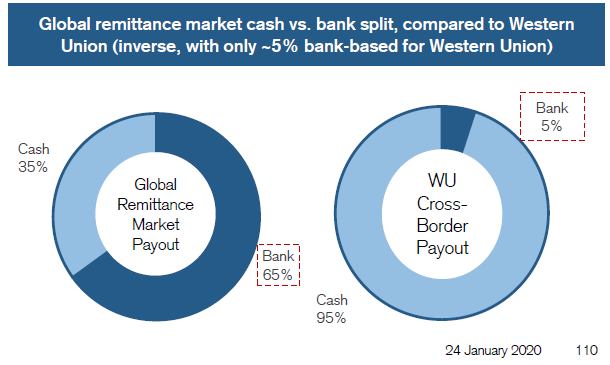

From the table above, developing countries remain the largest inflow on remittance. Top 10 countries made up 51% of the total volume. Majority of these countries share the common characteristics like poor banking system, high unbanked/underbanked population,etc.

Thus, the remittance for these countries will be highly cash based. MTOs like western union or money gram have an advantage in this regard. They have a network of agents situated around the countries to facilitate cash based remittance.

It is harder to compete within the cash segment as the receiving parties usually don't have bank accounts or have a low literacy rate. Even the mobile penetration is relatively low within these areas.

Besides, WU/moneygram is able to offer competitive rates for these currencies as the volume following through them is relatively high as compared to their competitors. As a result, it could be as competitive or better than Wise even though Wise offers it at mid market rate for these types of corridors (iE: USD/INR). Click here to see the rate.

Revolut

As for more comparable competitors, there is no shortage of argument on which business model is better between Wise and revolut. Revolut started off with international transfer but slowly evolved into everything apps. Aika has a good overview on the company.

Essentially, Revolut is able to charge low to no fees for international transfer because they are leveraging their other business to cover the losses for each transfer. (They do charge a fixed monthly subscription fee for different accounts, but it barely covers the cost of active users. However, less active users could subsidise more active users)

Their strategy is simple. By offering more products and bundling them together, customers will be more sticky. At the same time, with balances built up in their account, revolut could build up a local liquidity pool that has more reserves than their competitors. WIthout the legacy infrastructure and high cost of operation, revolut could build a formidable moat around itself. Thus, they are valued at around $33bil during the last round of funding.

It is definitely a formidable competitor but currently, they are using loss leader strategy to gain market share. Scale could eventually propel them to earn exceptional profit but it is tough to forecast. A lot of so-called scale companies are not even making any money with the exception of Amazon. Some good examples are grab, uber and doordash. Even a pandemic couldn't even help them to become profitable.

Business segment

As for the business segment, it has a lot more use cases and general solutions aren’t the best for their problem. Wise has been good at solving problems horizontally (underserved customer) but it often can’t help everyone as certain international banking has unique banking and maybe better served by more vertical specific tools. A16z teams have made a compelling argument as extracted below:

“Take a very high-volume sender, such as an exporter who needs to both manage their business as well as move large amounts of money. This type of company can create unique compliance headaches for traditional banks, so building compliance workflow tools and KYC processes designed specifically for this can help serve more businesses that might traditionally be turned away by banks. Companies like Silverbird and Kapapa are building in this exporter centric market, while others like Levro are working on similar solutions, but for startups.”

As a result, Wise is unlikely to win a big market share from this segment but small/micro businesses will be their main target.

Other key risks

As for other key risks, James Revell - Wise: Moving Money Around the World by Business Breakdown covers it well. Let me just summarise it as follow:

1. Countries modernizing their payments infrastructure. Essentially, it is to their interest to reduce fiction for foreign currencies and create an interlink between countries. Singapore is a good example where they've interlinked their domestic payments infrastructure with countries like India or Thailand.

2. Regulatory risk. While Wise is expanding aggressively internationally, they have to own and maintain multiple licences. Managing the regulatory risk for multiple jurisdictions with different rules and regulations could expose them to monetary and reputation risks. Eg: there is a long list of compliance such as Anti Money Laundry and counterterrorism financing. It will only add more cost for operation and there are instances where Wise is being fined in Abu Dhabi for weak control.

3. Paradigm shift towards digital currencies. The rise of blockchain technology or central bank digital currencies where digital cash is distributed around the world. This will essentially disrupt their business model and it is a terminal risk for their business but the possibility of it happening is fairly low at the moment.

Given the slow pace and bureaucracy of governments around the world, the first and third risks might take longer to materialize. it could be a longer term issue at least for now, there are other more thorny problems to resolve such as competition.

Management and culture

Investors are usually drawn to founder-led companies as they have deep skin in the game and thus their goals are aligned with shareholders. Basically, the founders own close to 28% of the company but have a voting right that is > 40%. They are effectively controlling the company and making decisions for the minority shareholders. The founding story is well known and I am not going to repeat it here. Click here and here to learn more about it.

It is common for some of the founders to step away from the company and pursue their own interests. For example, Taavet Hinrikus, ex chairman has left the company for his own venture as an angel investor (Plural platform). He was replaced by former CFO of Netflix, David Wells. However, he still owns a substantial portion of the company at 9% but I believe he will reduce his stake to focus on his private venture as he has his own ambition for helping entrepreneurs in Europe.

As for the current CEO/founder for Wise, Kristo Käärmann, he is still the largest shareholder (18%) with high absolute say (40% voting right) (will lapsed in 5 years-2026). Note: He sold none of his stock since IPO. Most founders have a mission in mind like Mark Zuckerberg, connecting the world,etc. Same goes to Kristo, he famously outline his mission below:

"We obsess about our mission in a way other companies don't. And we stay on track by following 3 unorthodox principles:

Be radically transparent

Most companies aren't always 100% honest about their fees and profits. We believe in having nothing to hide.

Charge as little as possible

Most companies charge as much as they can get away with. We believe in pricing for you, not us.

Make premium the new normal

Most companies have select products for select people. We believe in the best for everyone."

Other interviews by FT on his staff also mentioned that he is also humble and obsessive with customers. It reminds me of Jeff Bezos, another successful businessman. Below is an excerpt on the conversation:

“He’s extremely humble. If you didn’t know he was the CEO, you wouldn’t know,” said a former employee. “He hot desked with the rest of us.”

The walls of its London office are decked with mottos including “consumers > team > ego”; another is “no drama, good karma”.

However, nobody is perfect. He was penalised $500,000 for not paying his tax in 2021. It is rather embarrassing for a CEO to not pay taxes intentionally as charged by Her Majesty’s Revenue and Customs while he is a billionaire.

Incentive

Since 2019, Wise has accumulated up to £120mil of SBC while it only generated about £338 mil operating cash flow. There is no surprise that it made up 35% of the operating cash flow of the business since it is fairly common for tech companies to attract or retain their staff. It is rare to find companies like CSU/Adyen that have low/no SBC.

The CEO has a pay of £200k and chooses to abstain from bonus and LTIP since he will be the major beneficiary if the company outperforms. As for the team, they are incentivise by 2 key measures as per below:

It is rather a straightforward metric which suggests that they are incentivized to grow at all costs. It could be a sound strategy since they need scale to win over customers but in my opinion, this will encourage short termism for its management team.

Although the company has been profitable since it first started (which is rare), poor incentive could easily destroy the company. Note: the profitability of the company should be much lower due to the capitalization of staff costs as it is allowed under IFRS but not GAAP. If they normalize it, their profitability will be reduced by half. (50 mil capitalised staff cost vs 90 mil net profit for the past 4 years)

Conclusion

Wise certainly has the potential to be a large market capitalization company given the large addressable market. The company has built up trustable brands with their commitment to bring down the fees to exceptionally low levels.

However, the issues for this type of disruptive company is that there is large variability and there are alot of unknown unknown. A lot of things can change for the next few years as companies are getting better at solving issues. Besides, there is a lot of competition fighting for the ever shrinking market due to fees competition. My bet is that even if the fees go to zero, there will not be any significant increase for international transfer.

The harsh lesson I learned is that it is easy to be fooled by the shared scale of economy works for every industry. The truth is that it is never that simple and alot of companies are trying to convince their shareholders otherwise. Only companies that truly practice it will be able to win. Costco is a good example that ensures their margin is maintained at a very low level to benefit their customers.

The best for now in my opinion is giving this company time to build up a good track record as charlie munger once said: “a truly exceptional company should last for at least 20 years before we could conclude that it is”. It is never too late to invest in a good company just because it has grown to a large company. The best example would be Warren Buffett's investment into Apple in 2016 when it is already a huge company.

Appendix

Metrics

The management has emphasized that these metrics are highly important in measuring the success of the business. It is growing at an impressive rate and the management is highly optimistic about it.

Resources

How new entrants are redefining cross-border payments by EY

It’s All About the Money (Movement): Simplifying Cross-Border Payments by a16z

How Is the International Money Transfer Market Evolving? by Finance

Wise Plc by VIC

James Revell - Wise: Moving Money Around the World by Business Breakdown

How TransferWise beat Banks at their own game by Unit Economics

(Transfer) Wise - Company Deep Dive by Chirag Modi's Tech Notes

Revolut's Puzzle by Aika’s Newsletter